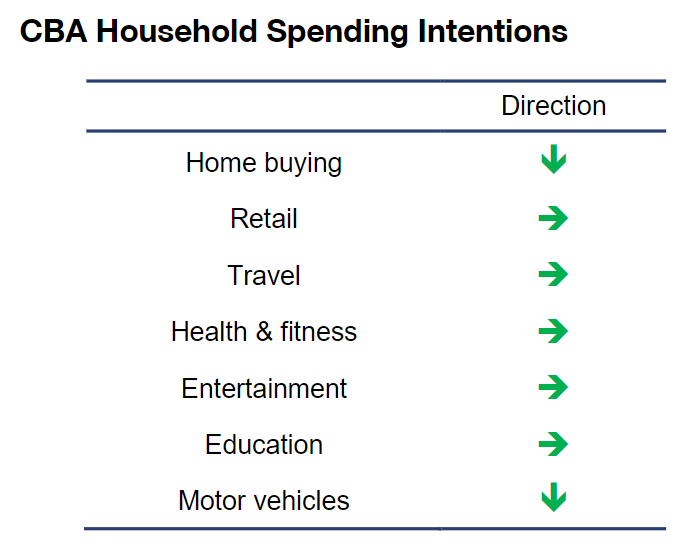

Spending patterns across key sectors of the economy tracked sideways in September, according to the latest Commonwealth Bank Household Spending Intentions survey:

Key Points:

The Commonwealth Bank Household Spending Intentions series showed that spending largely tracked sideways in September –as the impacts of the Victoria stage 4 shutdowns remain evident.

Both Home Buying and Motor Vehicle spending intentions softened a little during September. Spending intentions for Retail, Travel, Health & Fitness, Entertainment and Education tracked sideways.

The Household Spending Intentions series for September showed that spending patterns across key sectors of the economy largely tracked sideways on the month –reflecting the ongoing stage 4 shutdowns in Victoria and the bumpy recovery now underway in the economy.

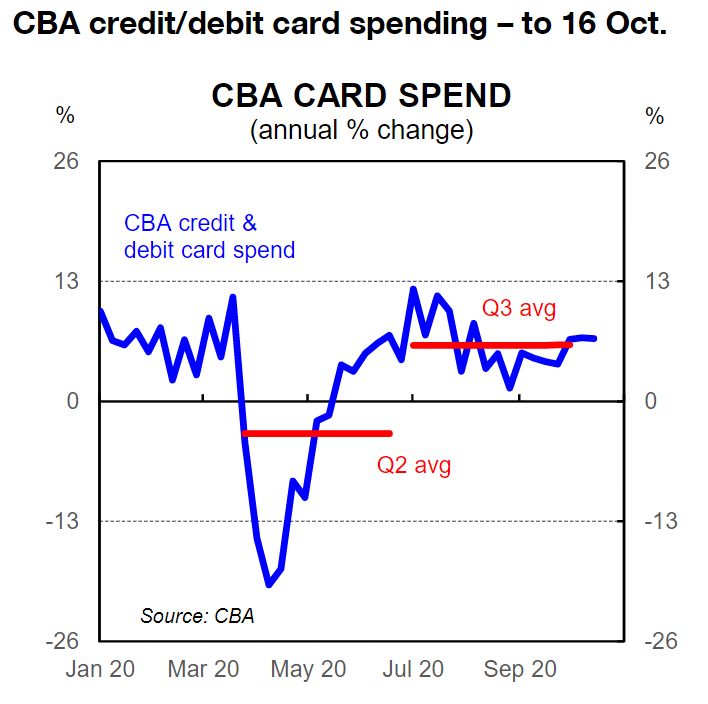

Notwithstanding the sideways trend in September, weekly CBA credit & debit card data shows that overall spending in Australia was higher in Q3 20 than it was in Q2 20. Some further improvement could be expected throughout Q4 20 and into 2021 given the extent of the fiscal and monetary policy support being applied to the economy and the level of savings.

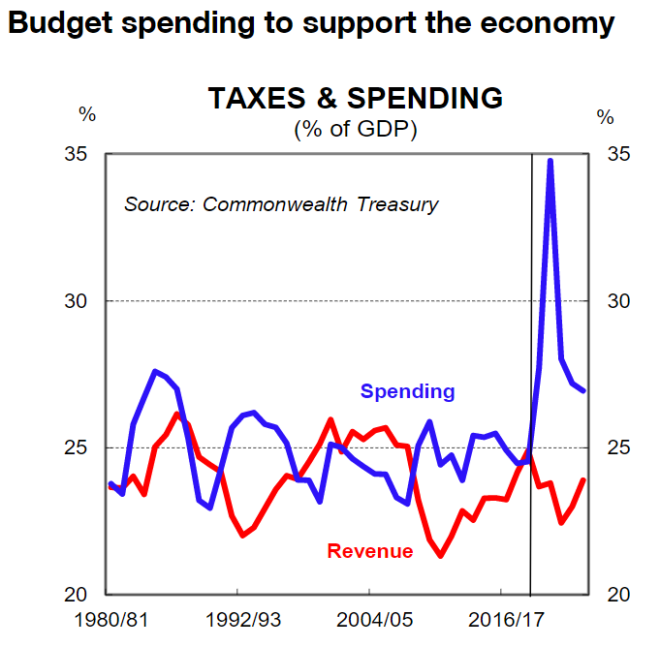

Indeed, as we detailed here the 2020/21 Commonwealth Budget detailed a large fiscal support package, with the fiscal impulse in 2020/21 (ie. the increase in the budget deficit from the previous year) a very large 6.7% of GDP. As shown in the chart facing, this fiscal stimulus is being provided largely by a surge in government spending across a number of support programs designed to improve income flow for consumers and businesses and to encourage businesses to increase both employment and investment.

For September, highlights in household spending intentions include:

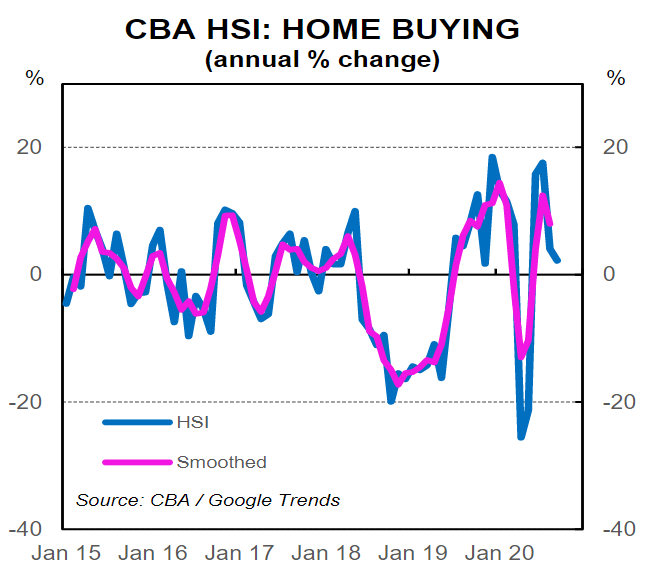

Home Buying spending intentions declined moderately in September. While the number of home loan applications seen in September were higher than September last year, there was a decrease on the month.

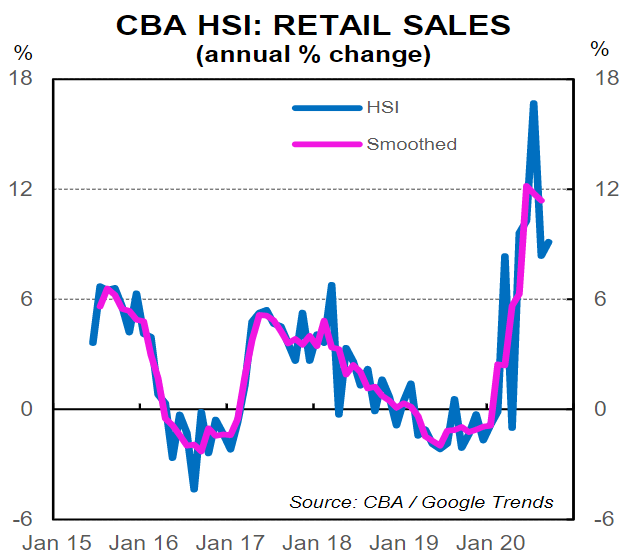

Retail spending intentions largely tracked sideways in September, coming off the highs seen pre-Victoria shut-down in July.

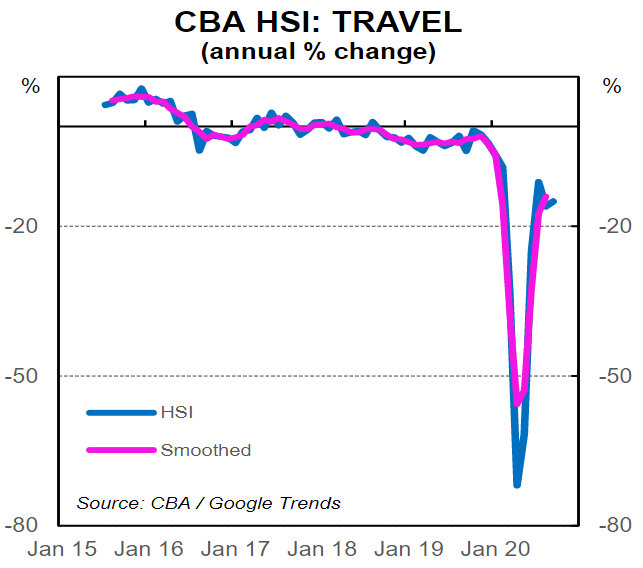

After bouncing sharply off their lows of April in recent months, Travel spending intentions tracked sideways in September.

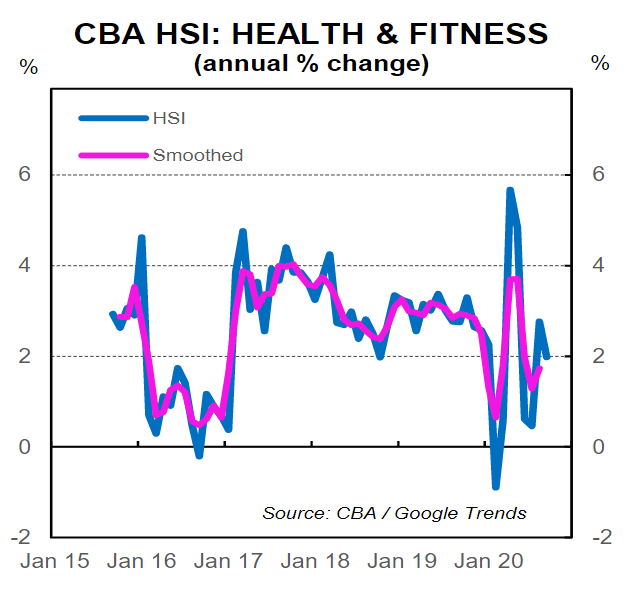

Health & fitness spending intentions also tracked largely sideways in September and are well off their highs seen early in the Covid-19 period.

Whilst well up from their lows of April, Entertainment spending intentions were also little changed in September.

Education spending intentions moderated a little in September, with both the value of transactions and Google searches down.

Motor vehicle spending intentions lost momentum again in September, coming back down off their Covid-19 highs seen in June.

Home buying intentions

Home buying spending intentions were marginally lower in September, continuing the small decline evident in August.

Although the number of home loan applications seen in September 2020 were higher than September last year, there has been a decrease on the month. In addition, Google searches declined marginally in September, as they had the previous month.

But the RBA’s substantial easing of monetary policy has seen mortgage rates fall to multi-generational lows and we expect these low interest rates to continue to provide support to home buying. We expect house prices to show a peak-to-trough decline of -6%,but with substantial deviation expected across the capital cities.

Retail spending intentions

Retail spending intentions largely tracked sideways in September, coming off the highs seen pre-Victoria shut-down in July.

Retail spending intentions were, however, mixed across different categories during September. Gains were seen in spending in department stores, grocery stores, furniture & household equipment and appliances, paint & hardware stores, school and office supplies,

Weakness in September was most evident in spending intentions in duty free stores, men’s clothing, shoe stores, beauty & barber shops.

Whilst accounting for a small share of overall spending, outsized gains continue to be seen in spending intentions on arts & crafts supplies, Apps, electronic stores, hobby, toy & games stores and record stores.

Travel spending intentions

After bouncing sharply off their lows of April in recent months, Travel spending intentions tracked sideways in September.

In the month, ongoing recovery was seen in visits to aquariums, camper & recreational vehicle dealers and trailer parks/camp grounds.

Weakness remains evident in key areas such as airlines, hotels, motels & resorts, motor home & recreational vehicle hire, sport & rec camps, cruise lines, timeshare, tourist attractions, travel agents, car rentals and bus lines. We would expect further gradual improvement as more state borders are reopened.

Health & Fitness spending intentions

Health & fitness spending intentions also tracked largely sideways in September and are now well off their highs seen early in the Covid-19 period.

Within the health & fitness sector, spending intentions are mixed across the different categories. Improvement can be seen in spending intentions on chiropractors, dentists, optometrists and podiatrists.

Large increases in spending intentions can also continue to be seen in bicycle shops –sales and service, golf courses and sporting goods stores.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.