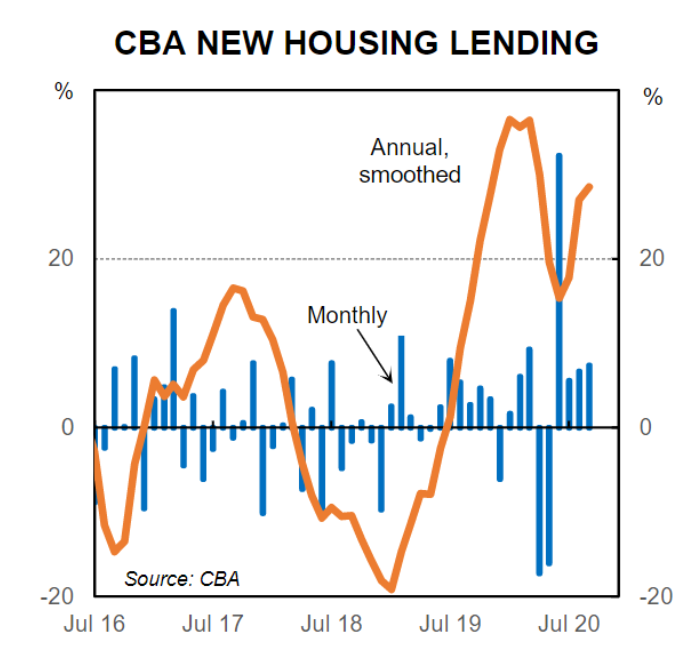

According to CBA’s internal data, Australian mortgage lending strengthened further in September, up 30% year-on-year:

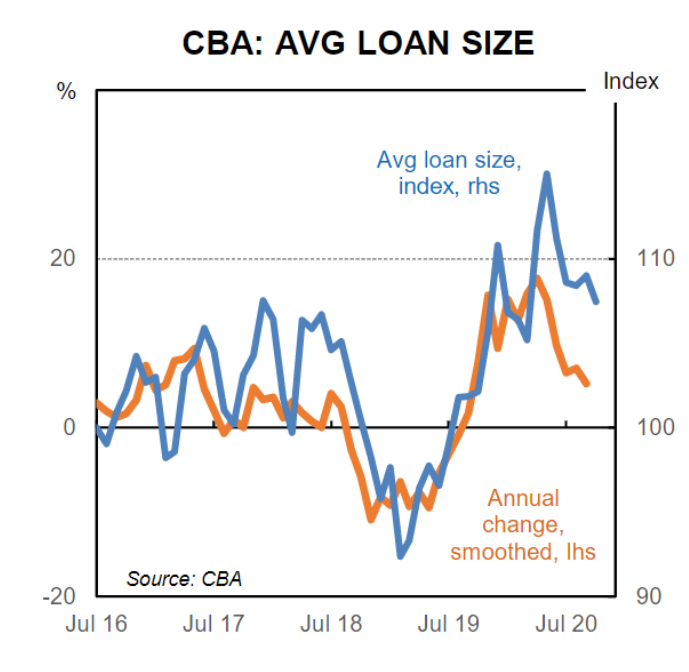

However, average loan sizes are shrinking; albeit are still higher year-over-year:

Advertisement

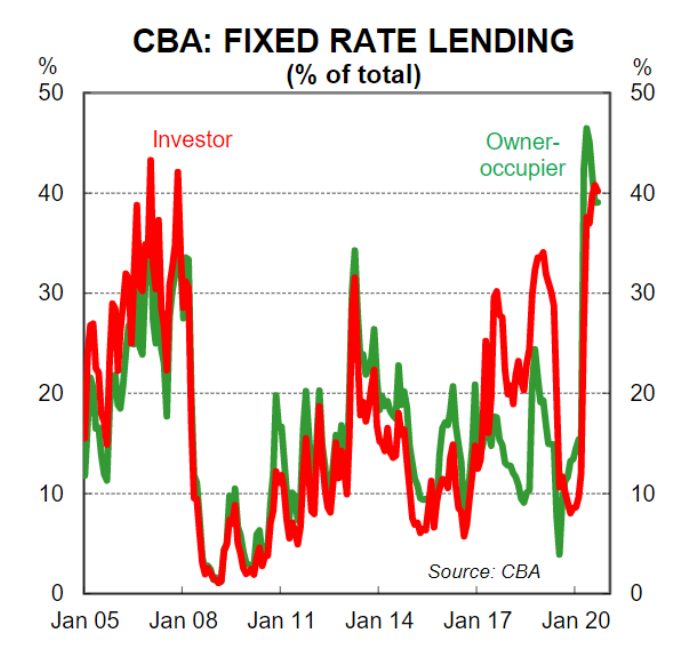

The share of fixed rate lending remained at high levels, driven by fixed rates being lower than variable rates:

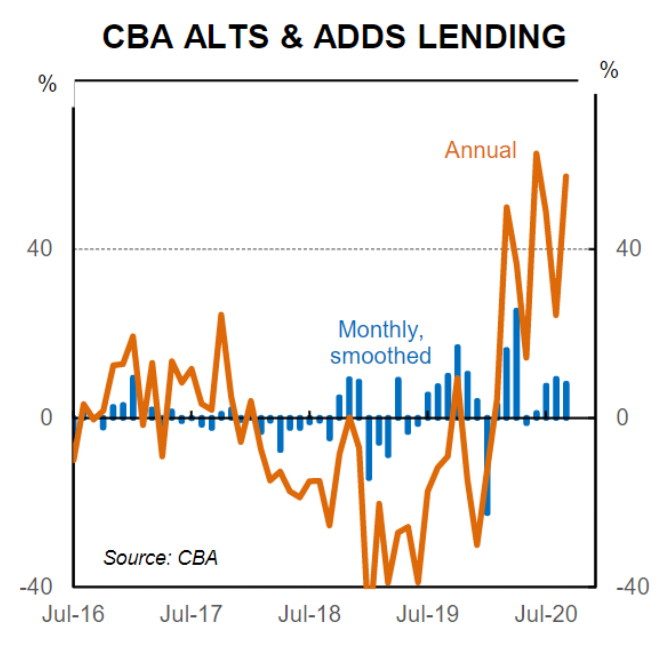

Lending for renovations continued to grow, likely driven by people spending more time at home and lower borrowing rates:

Advertisement

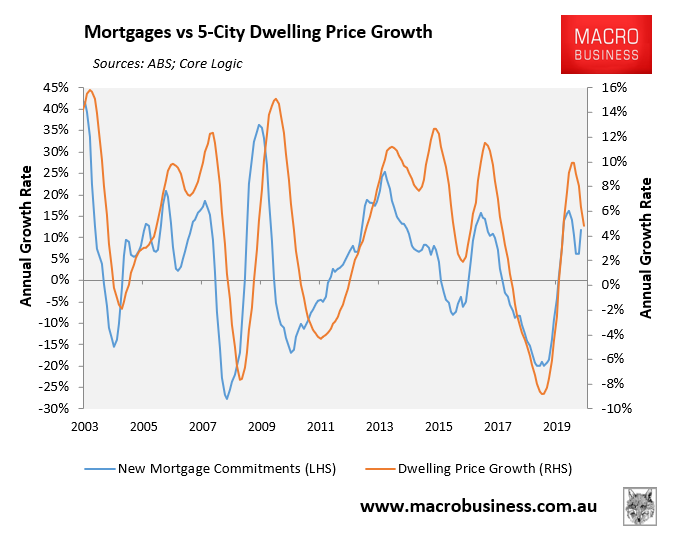

Mortgage growth is one of the best indicators for property price growth having displayed a very strong historical correlation:

Advertisement

Thus, this CBA data is bullish for Australian property values, assuming it is replicated across the mortgage market (as previous CBA releases have been).