From Gareth Aird, Head of Australian Economics at CBA:

Key Points:

We expect the RBA to ease monetary policy at the November Board meeting and we expect a suite of measures to be announced.

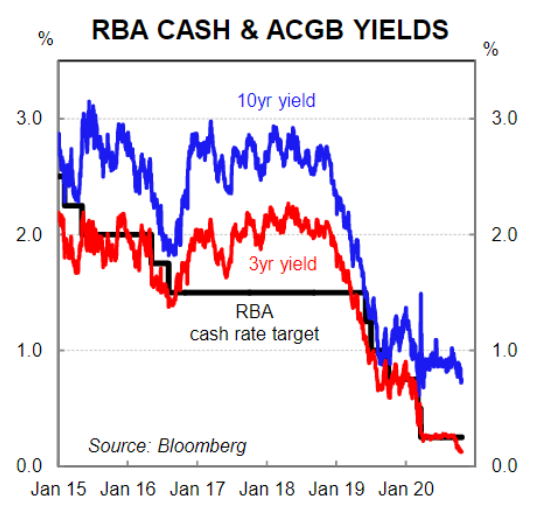

We expect the RBA will lower the cash rate target, lower the target on the 3-yearAustralian Government bond yield and lower the term funding facility rate all to 10 basis points(from the current 25 basis points).

We expect the RBA will announce a quantity based asset purchase program that will involve buying Australian Commonwealth Government Bonds (ACGBs) and Semi-government bonds with a focus on the 5-10 year part of the curve.

Overview

The RBA’s November Board meeting is shaping up as a memorable one. Both RBA Governor Lowe and Deputy Governor Debelle have indicated that more monetary policy easing is forthcoming. And with the Federal Budget now behind us, it looks clear to market participants that monetary policy easing is now imminent. In many ways the question is around what the RBA will do at the November Board meeting, rather than will they do something.

Our central scenario for the November Board meeting is that the RBA will deliver a comprehensive package –building on the policy announcements on 19 March 2020. Specifically, we expect the RBA to announce:

A reduction in the cash rate target to 10basis points (from 25 basis points).

A reduction in the target for the yield on 3-year ACGBs to “around “10basis points (from“around”25 basis points).

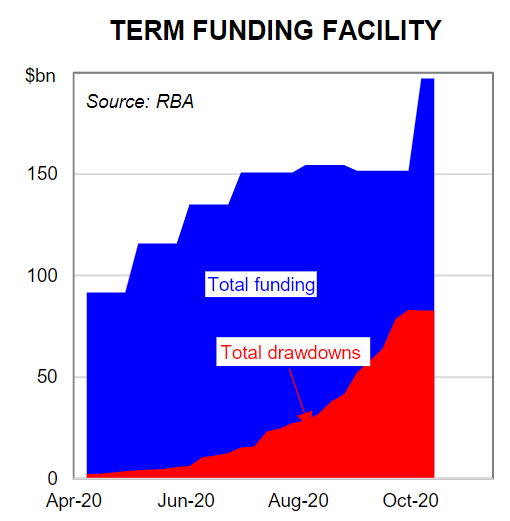

A reduction in the in the interest rate charged on the Term Funding Facility (TFF) to 10 basis points (from 25 basis points).

A reduction in the interest rate paid on exchange settlement balances at the RBA to 5 basis points (from 10 basis points).

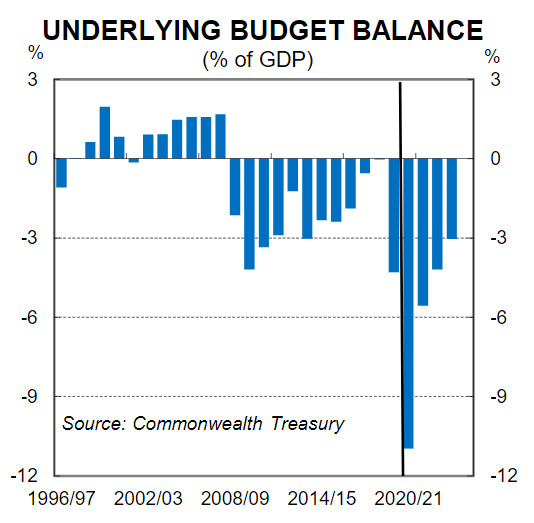

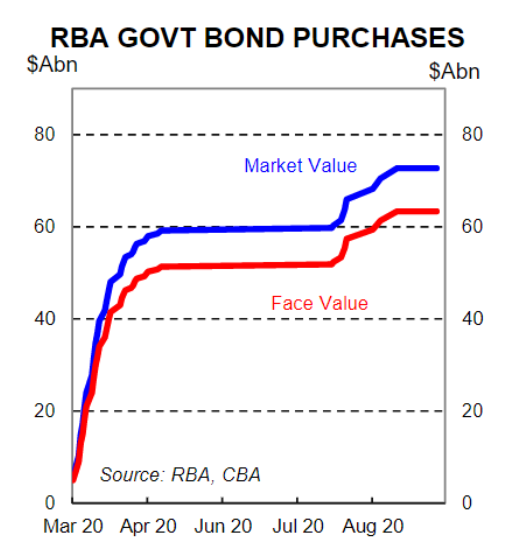

A commitment to purchase a fixed quantity ($A100bn, which is approx. 5% of GDP) of ACGBs and Semi-government securities with an explicit intention to focus purchases on the 5-10 year part of the curve. Our working assumption is that the RBA will not announce a timeframe in which they intend to purchase the announced quantum of bonds as they will seek to retain some flexibility. We do, however, expect the purchases to start immediately.

We do not expect the RBA to put a target for the yield on any other maturity bond other than the 3-year ACGB–as is currently the case.

The rationale for our call

On 22 September 2020 RBA Deputy Governor Guy Debelle delivered a speech on the Australian Economy and Monetary Policy. Most importantly for financial markets there was a discussion on ‘other’ options for monetary policy (i.e. what more the RBA could do to ease monetary policy). What the Deputy Governor spoke about in that speech remains highly relevant for the November Board meeting. Deputy Governor Debelle listed four ‘other’ options for monetary policy easing.

(i) Buy bonds further out along the yield curve, supplementing the three-year yield target. This is essentially additional bond purchases further out the yield curve on a regular basis. This would have the impact of lowering bond yields at longer maturities and would put downward pressure on the exchange rate.

(ii) Intervention in the foreign exchange market to lower the AUD. Debelle said a “lower exchange rate would definitely be beneficial for the Australian economy”. However, he also pointed out that because the Australian dollar is broadly aligned with its fundamentals, he doubts intervention would be effective. We agree on both counts.

(iii) Lower the current structure of interest rates in the economy a little more without going into negative territory. Debelle listed the remuneration on exchange settlement balances (currently 10 basis points), the three-year yield target (currently 25 basis points)and the borrowing rate of the TFF (currently 25 basis points). He noted, “it is possible to reduce these interest rates”.

(iv) Negative interest rates. Debelle noted that, “the empirical evidence on negative rates is mixed”. This is somewhat different to what Governor Lowe has stated in the past, where he has said that he believes the cost of negative rates exceeds the benefits. Nonetheless we remain of the view that the RBA has no intention of taking key policy rates into negative territory.

At the time of Deputy Governor Debelle’s speech we didn’t think that more monetary policy easing was imminent, particularly given that earlier in the month at the September Board meeting the RBA had expanded and extended the size of the TFF. In addition, whilst Debelle’s discussion around what other policy options were available was prudent, with the Federal Budget just around the corner it seemed logical to leave policy on hold at the October Board meeting. That turned out to be the case.

The focus then shifted to RBA Governor Lowe’s speech delivered on 15 October. We expected the Governor’s speech to provide clarity on the near term direction for policy one way or the other and that’s exactly what we got. Governor Lowe made it very clear that more monetary policy easing is forthcoming and the November Board meeting is now the obvious time to deliver –why wait once you’ve decided and signalled that you intend to do something?

In his speech the Governor did not reiterate the four ‘other’ options that the deputy Governor had spoken about a month earlier. But he did make reference to Debelle’s speech and stated, “the options (for more easing) have been laid out in previous speeches by the Deputy Governor and myself and I don’t plan to elaborate on these again today.” That statement rubber stamps the views expressed previously on the four options. And importantly it signals that the decisions that will be taken by the Board at the November meeting will be consistent with the views on each of the four options previously canvassed.

It is therefore clear to us that at this juncture the RBA has no intention of (i) intervening in the foreign exchange market to lower the AUD; or(ii) taking key policy rates negative. That leaves the other two options in play: (i) lowering the current structure of interest rates in the economy a little more without going into negative territory; and (ii) buying bonds further out along the yield curve, supplementing the 3-year yield target.

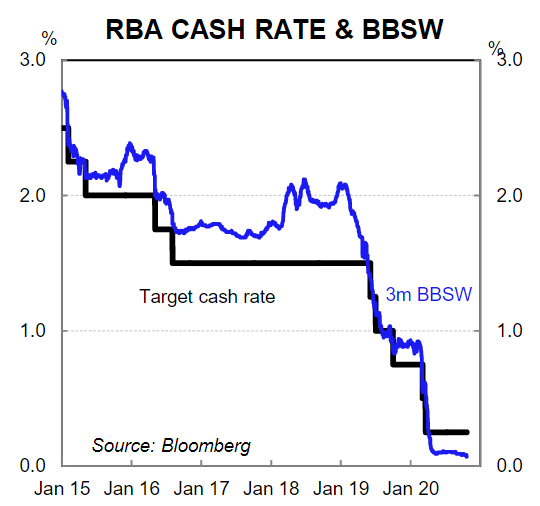

On lowering the current structure of interest rates, regular readers will be aware that we have previously questioned the efficacy of tinkering with the cash rate in a very fine corridor between 10 basis point and 25 basis points because it carries the risk of other important short-term rates falling into negative territory. In addition the traded or actual cash rate sits below the 25 basis points target at 13-14 basis points because of the abundance of liquidity in the system and the fact the RBA pays 10 basis points on retail bank’s cash balances held at the Reserve (known as exchange settlement accounts or ES accounts).

Further, one month and three month Bank Bill Swap Rates (BBSW) sit even lower at around 7 basis points(admittedly that’s in part because financial markets are pricing in cuts to key policy rates, but even before that one month and three month BBSW were sitting around 8-9 basis points).We continue to question the effectiveness of pushing key policy rates lower at this juncture, but clearly what matters more is what the RBA is likely to do rather than what we think they should do.

We think there is enough evidence in the RBA’s recent communication to expect that they will now push key policy rates lower at the November Board meeting. We believe this means a reduction in the cash rate target to 10 basis points, a reduction in the target for the yield on 3-year Australian Government bonds to “around”10 basis points (from “around” 25 basis points) and a reduction in the in the interest rate charged on the TFF to 10 basis points (from 25 basis points).

On the basis that the RBA are going to lower the cash rate target, then it makes sense to also drop both the target for the yield on the 3-year Australian Government bond (particularly given the RBA has regularly statedthe3-year yield target is closely aligned with the Board’s guidance about the future direction of the cash rate target) and also the interest rate on the TFF.

The interest rate paid on exchange settlement accounts will also need to be lowered. Conceivably the RBA could take that down to 1 basis point, but we suspect they will drop it to 5 basis points.

On bond buying specifically we expect the RBA to commit to purchasing a fixed quantity ($A100bn,which is approx.5% of GDP) of ACGBs and semi-government securities with an explicit intention to focus purchases on the 5-10 year part of the curve.

Clearly any bond purchases of shorter duration intended to maintain the target for the yield on the 3-year Australia Government bond will also be part of the announced quantum. Effectively we think that the RBA will end uprunning both price and quantity based quantitative easing (QE). We do not, however, expect the RBA to put a target for the yield on any other maturity Australian Government bond other than the 3-year bond – as is currently the case.

We think that the RBA is more likely to announce that it will purchase a fixed quantity of bonds rather than simply state an intention to buy more bonds, as some analysts have suggested. The reasoning is simple–announcing a fixed quantum of bonds to be purchased sends an explicit signal to the market that the RBA is committed to expanding its balance sheet.

The RBA wants to ease financial conditions through the use of its balance sheet to support the Australian economy and the best way to do that is to be explicit in what they are trying to achieve. Committing to purchase a fixed quantity of bonds is likely to more put more downward pressure on bond yields, and by extension the exchange rate, than simply stating an intention to buy more longer dated bonds.

Our working assumption is that the RBA will not specify a time period in which the intended bond purchases will take place. We believe that they will seek to retain some flexibility in the pace at which they will purchase assets as some other central banks have done. Having said that, we think they will purchase bonds at a pace of around $A15bn a month, which would see purchases total $A100bn by the middle of next year.

We don’t believe that financial market participants should be disappointed if the RBA does not announce a larger quantum as the option to further expand purchases will always remain on the table.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.