Advertisement

From CBA’s head of Australian economics, Gareth Aird:

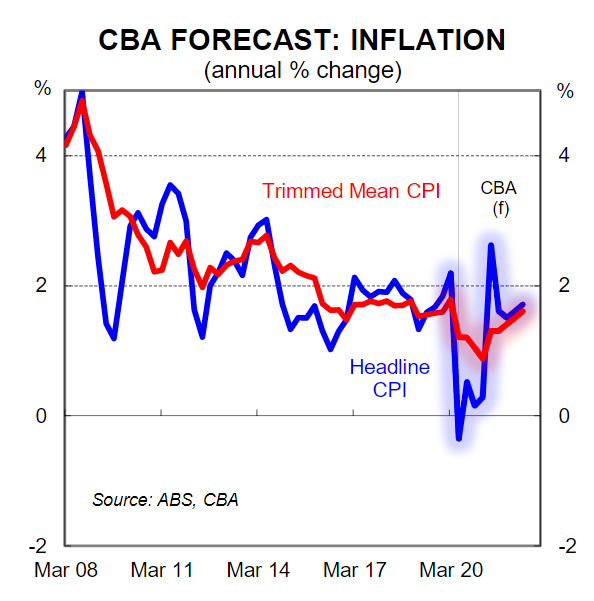

- We expect the headline CPI to increase by 1.4% in Q320 (+0.5%/yr).

- The trimmed mean CPI on our forecasts will print at +0.4% (+1.2%/yr).

- Recent communication from the RBA means that more policy easing is imminent and we expect it to be delivered at the November Board meeting.

Summary

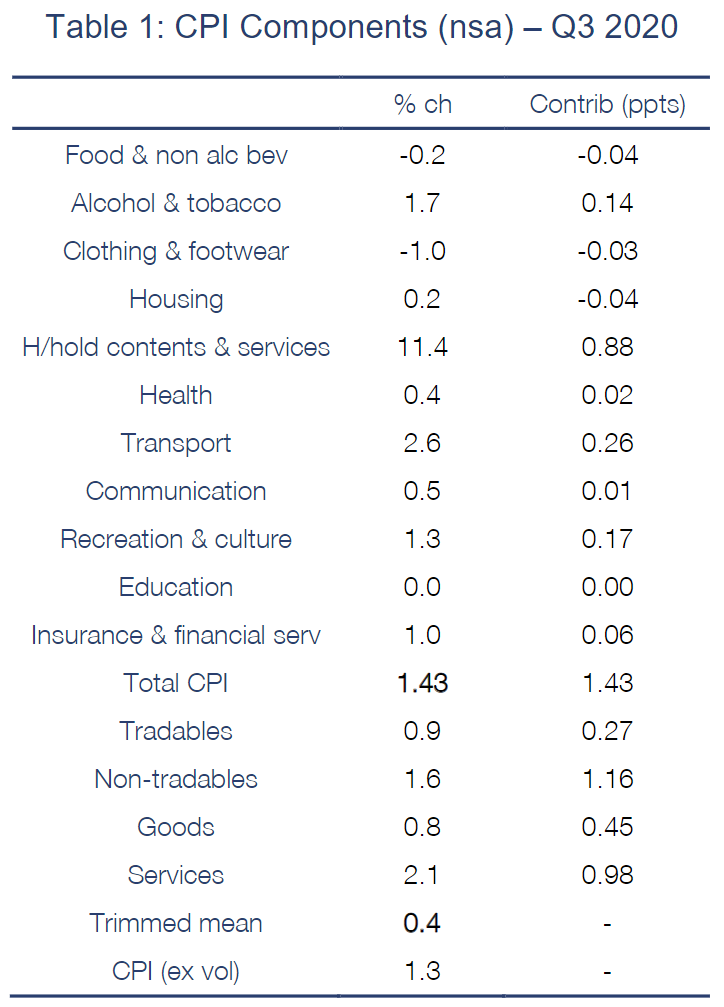

On Wednesday 28 October the ABS will publish the Q3 20 CPI. We expect to see a sharp lift in headline inflation primarily because: (i) child care and pre-school prices have returned to more normal levels; and (ii) petrol prices lifted over the quarter. Those two factors alone are anticipated to add 1.10ppts to the headline CPI.Context of course is key. The Q2 20 CPI fell by 1.9% – the largest quarterly fall in the CPI since 1931. So our forecast for a 1.4% increase in the headline CPI over Q3 20 still leaves the annual rate of inflation low and well shy of the RBA’s inflation target.Underlying inflation is set to remain muted. Our forecast is for the trimmed mean, the RBA’s preferred measure, to rise by 0.4% over Q3 20. Such an outcome would see the annual pace of core inflation sit at just 1.2%. The six month annualised pace of underlying inflation on our figuring drops to just 0.5% given the trimmed mean fell by 0.1% in Q2 20. See Table 1 below for our detailed forecasts for the Q3 20 CPI basket.The RBA currently expects inflation to remain below target over their forecast horizon which is an uncomfortable place to be for an inflation targeting central bank. That discomfort looks set to result in more monetary policy easing at the November Board meeting. Jobs are the focus for the RBA at the moment, but the disinflationary pulse that will be evident in the data next week will certainly feed into the policy debate and will be consistent with more easing. We will publish our full RBA preview early next week.Some unusual dynamics within the CPI basketReaders that follow the inflation data closely will be aware that a number of unusual dynamics played out of the June quarter. More specifically,

- Child care services were free for families from 6April to 28 June(62 out of 65 business days). That resulted in a 95% fall in the CPI child care expenditure class and shaved1.1ppts from the headline CPI.

- Petrol prices plunged 19.3% which took 0.7ppts from the headline CPI.

- Pre-school and primary education fell by 16.2% because of free pre-school being provided in NSW, Victoria and QLD which took off 0.2ppts.

In addition, a decent chunk of the CPI was missing reflecting unavailable goods and services due to COVID-19 restrictions. That meant that 9% of the CPI was imputed at the headline CPI. Given the headline CPI was massively impacted by free child care, free pre-school and the plunge in petrol prices it meant that 9% of the CPI was imputed at an unusually low rate.A number of the factors that pulled the headline CPI down in Q2 20 will be reversed in Q3 20. Child care is no longer free. And petrol prices over Q3 rose by ~9%. The upshot is that we will get back a large proportion of the fall in Q2 20 CPI in the September quarter. Notwithstanding, it is clear that we are in a period of very low inflation that we would characterise as disinflationary rather than deflationary. It’s often easy to get bogged down in the detail with the CPI and we suspect that the Q3 CPI will throw up a few curve balls with regards to the basket itself. The ABS have had to suspend CPI in-store collection and there will be more missing prices than usual due to ongoing COVID-19 restrictions, particularly the Stage 4 restrictions in Melbourne. That complicates the forecasting process and suggests there is a greater margin for error than usual. But in any event what is more important to us at the moment is the story rather than the detail. On that score it is evidently clear to us that market driven wages growth will remain very weak over the next few years. That in turns mean that any upside surprise on consumer inflation is effectively a drop in real wages and at this particular juncture will not be welcome. Policymakers want higher inflation that is generated from higher wages and a reduction in spare capacity in the economy. And that looks to be a long way off which is why the RBA appears committed to ease policy further at the November Board meeting.

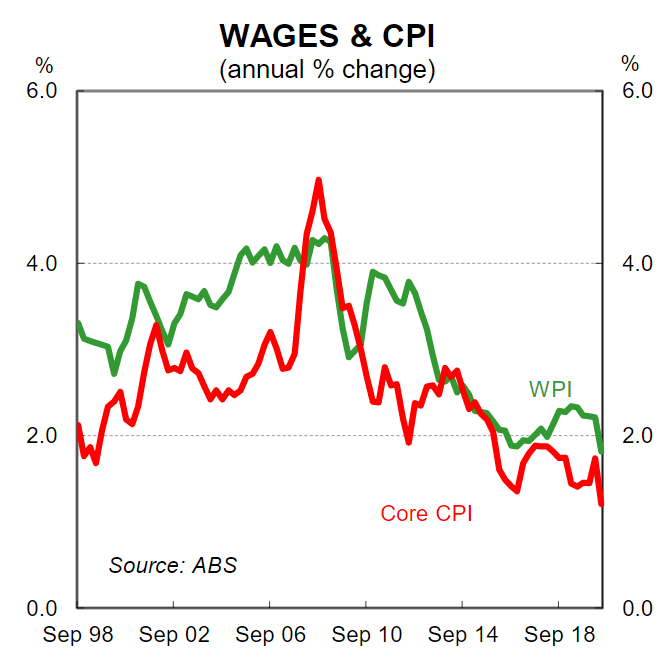

It’s often easy to get bogged down in the detail with the CPI and we suspect that the Q3 CPI will throw up a few curve balls with regards to the basket itself. The ABS have had to suspend CPI in-store collection and there will be more missing prices than usual due to ongoing COVID-19 restrictions, particularly the Stage 4 restrictions in Melbourne. That complicates the forecasting process and suggests there is a greater margin for error than usual. But in any event what is more important to us at the moment is the story rather than the detail. On that score it is evidently clear to us that market driven wages growth will remain very weak over the next few years. That in turns mean that any upside surprise on consumer inflation is effectively a drop in real wages and at this particular juncture will not be welcome. Policymakers want higher inflation that is generated from higher wages and a reduction in spare capacity in the economy. And that looks to be a long way off which is why the RBA appears committed to ease policy further at the November Board meeting.

About the author

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.

Advertisement