Australian housing affordability, which improved over the year to September, will continue to improve slightly over the next 12 months, because of low mortgage interest rates and lower housing prices.

» Affordability will continue to improve on low mortgage rates and lower housing prices. Australian households with two income earners needed 23.0% of monthly income to meet mortgage repayments on new loans in September 2020, down from 25.1% a year earlier. We expect low interest rates for the foreseeable future and lower housing prices over the next 12 months, further improving housing affordability. Conversely, household incomes will come under pressure in coming months as coronavirus-related government income support measures end, but in respect of housing affordability, we do not expect this to outweigh low mortgage interest rates and lower housing prices.

» Housing affordability improved in all major capital cities in 2020. Housing affordability improved in Sydney, Melbourne, Brisbane, Perth and Adelaide over the year to September 2020. For all capital cities, housing was the most affordable or near the most affordable in a decade in September. The affordability of apartments and houses improved in all capital cities over the year to September.

Affordability will continue to improve on low mortgage rates and lower housing prices

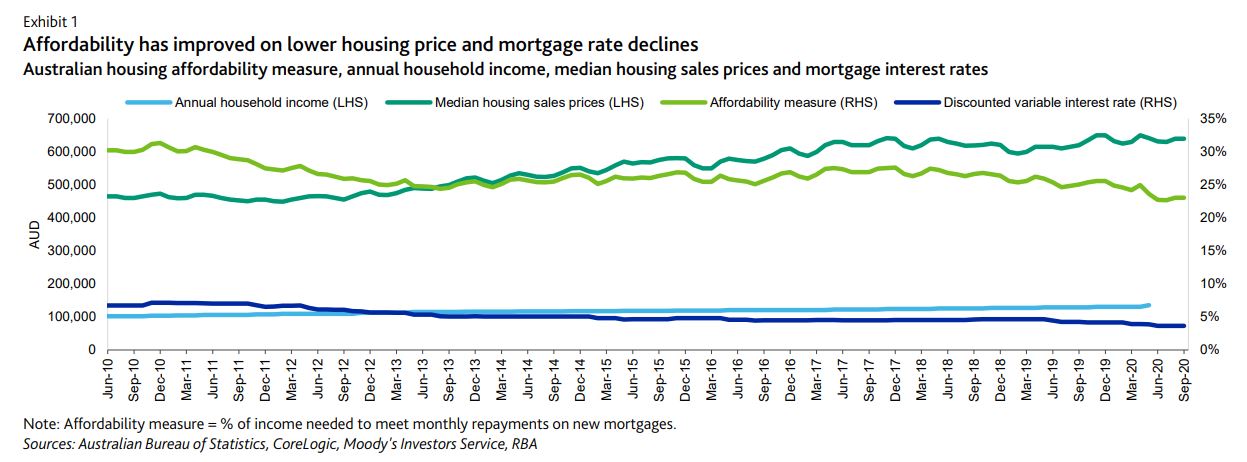

Housing affordability for new mortgage borrowers – which we measure as the proportion of household income borrowers need to meet repayments on new mortgages – improved on average in Australia over the year to September 2020, because of mortgage interest rate cuts and lower housing price in the wake of the coronavirus pandemic.1

More affordable housing reduces credit risks for new mortgages, which is positive for new residential mortgage-backed securities backed by such loans.

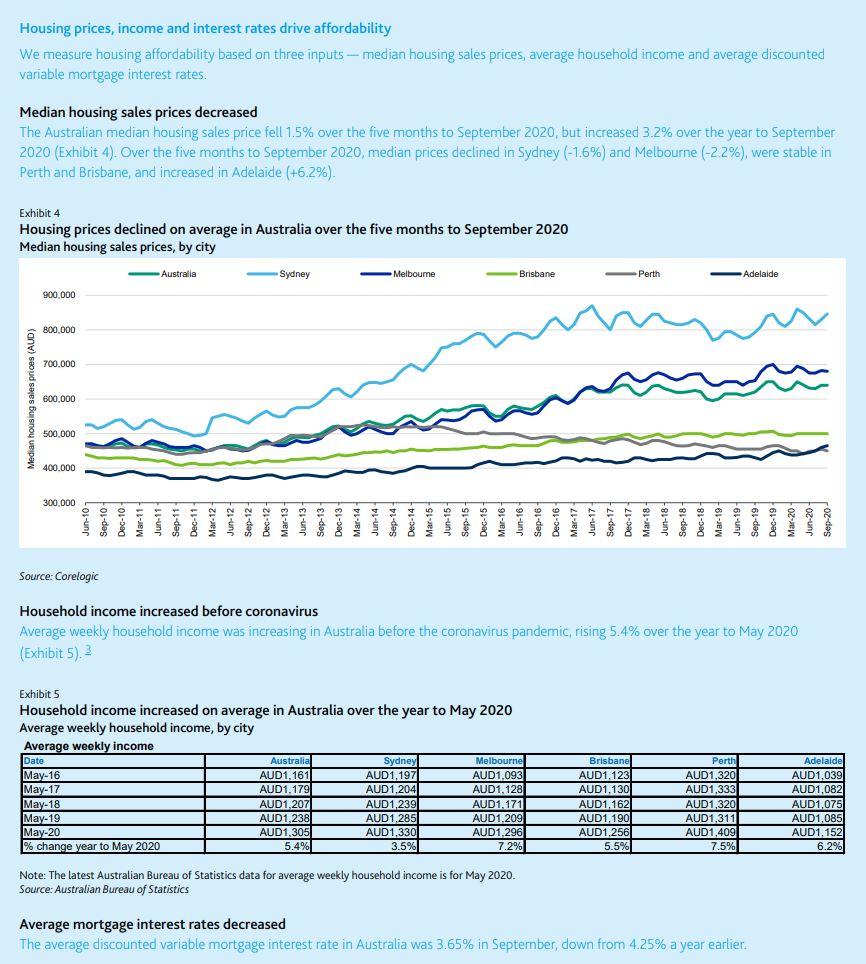

On average, Australian households with two income earners needed 23.0% of their monthly income to meet monthly mortgage repayments on new loans in September 2020, compared with 25.1% in September 2019 and 26.4% on average over the last 10 years. Australian housing prices declined an average 1.5% over the five months to September 2020 because of the economic fallout from the coronavirus, though prices still rose 3.2% over the year to September.

The Reserve Bank of Australia (RBA) lowered the official cash rate to a record low 0.25% in March to combat the economic downturn triggered by the pandemic, driving mortgage interest rates down. Government assistance payments have supported household incomes since the coronavirus pandemic. Before the pandemic, average household incomes were increasing, rising 5.4% over the year to May.

We expect housing affordability will continue to improve moderately over the next 12 months. We expect interest rates to remain low for the foreseeable future. Housing prices will likely see some downward pressure as the result of the macroeconomic weakness, albeit the impact may be muted due to the low interest rates. Conversely, household incomes will come under pressure in coming months as government income support measures such as Jobkeeper and Jobseeker end, but we do not expect this to outweigh the impact of low mortgage interest rates and housing price movements.

Exhibit 1 shows changes in our housing affordability measure, annual household incomes, median housing sales prices and mortgage interest rates.

Housing affordability improved in all major capital cities in 2020

Housing affordability improved in all major Australian capital cities over the year to September 2020. For all capital cities, housing was the most affordable or near the most affordable in a decade in September 2020.

In Sydney, new borrowers needed 29.9% of household income to meet mortgages repayments in September, compared with 30.9% a year earlier and 32.7% on average over the last 10 years. However, Sydney remained the least affordable city for housing in Australia.

The Sydney median housing price fell 1.6% over the five months to September 2020 because of the coronavirus outbreak, but still rose 6.7% over the year to September 2020.

In Melbourne, new borrowers needed 24.6% of household income to meet mortgage repayments in September 2020, compared with 27.0% a year earlier and 27.8% on average over the last 10 years. The Melbourne median housing price fell 2.2% in the five months to September, but increased 4.1% over the year to September 2020.

In Brisbane, new borrowers needed 18.7% of household income to meet mortgage repayments in September 2020, the lowest in a decade and down from 21.0% a year earlier. Brisbane housing prices were stable over the 12 months to September 2020.

In Perth, new borrowers needed 15.0% of household income to meet mortgages repayments in September 2020, the lowest in a decade and down from 17.4% a year earlier. Perth is the most affordable capital city for housing in Australia. The Perth median housing price declined 1.1% over the year to September 2020, the most of any major Australian city.

In Adelaide, new borrowers needed 19.0% of household income to meet mortgages repayments in September 2020, compared with 19.8% a year earlier and 21.6% on average over the last 10 years. The city’s median housing price increased 8.1% over the year to September 2020.

Exhibit 2 shows that housing affordability improved in all major capital cities.

The affordability of apartments and houses improved in all capital cities over the year to September 2020, as Exhibit 3 shows.

Owner-occupiers bidding up prices today have only themselves to blame.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.