DXY took off last night:

The Australian dollar was hammered:

With EMs:

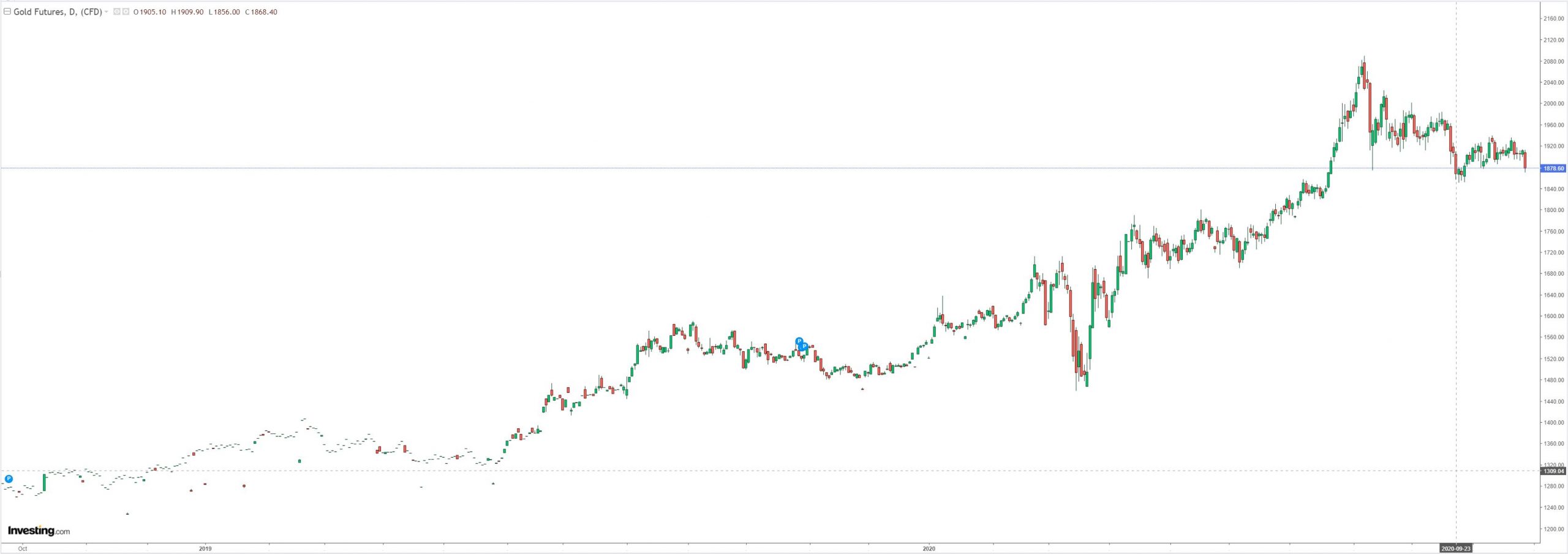

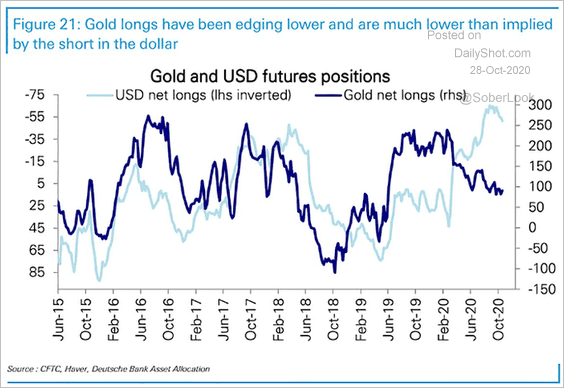

Gold puked:

Oil may halve here:

Metals fell:

Miners were flushed:

EM stocks gapped:

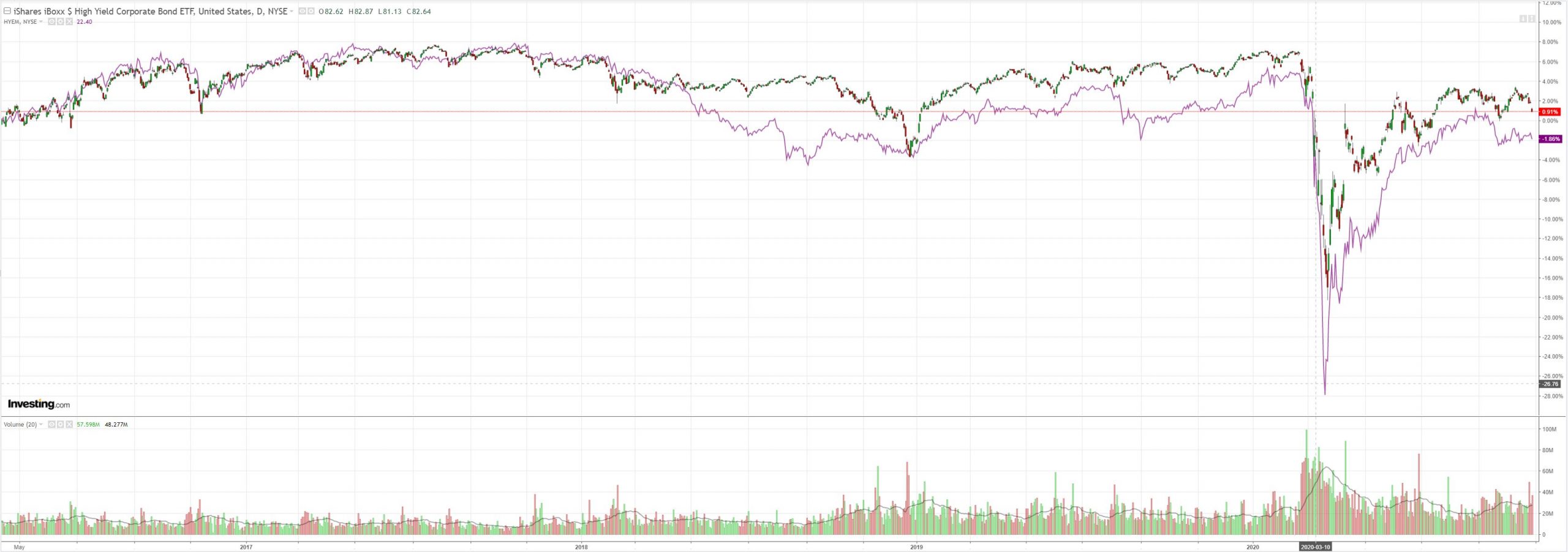

With junk. Watch EM for an early warning on more carnage:

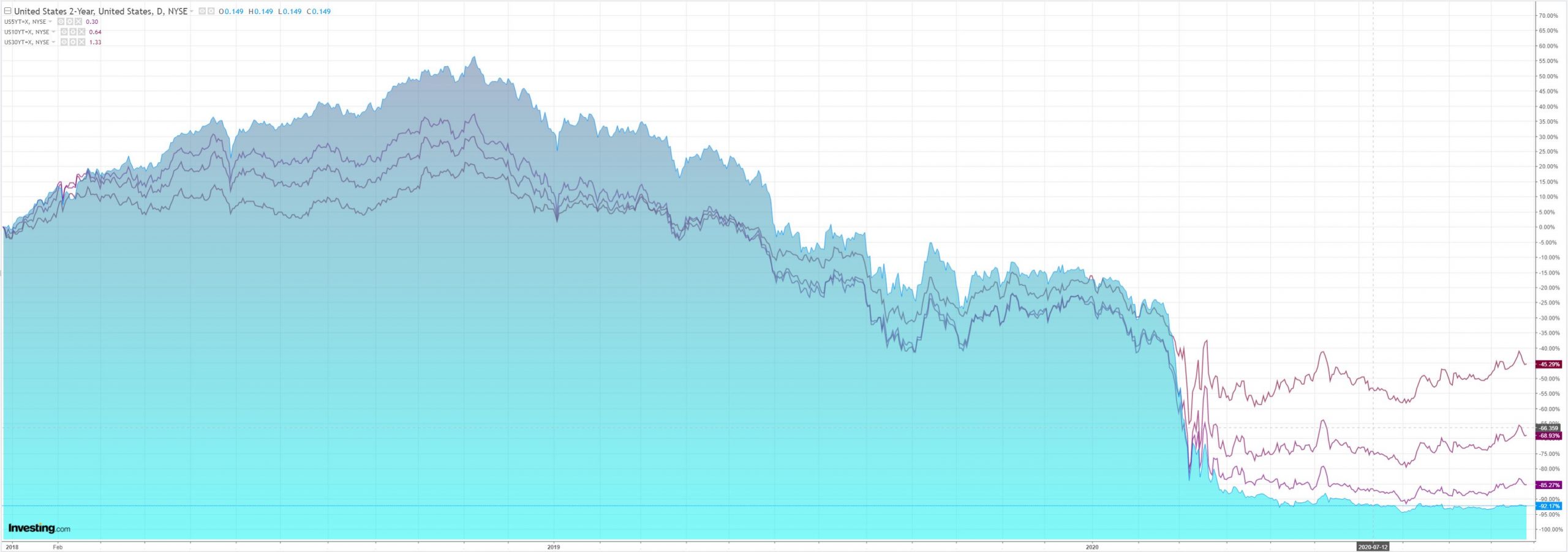

Treasuries steepened, bizarrely:

Stocks are one bad day from delivering the greatest bearish double-top you’d ever care to see:

Westpac has the data wrap:

Event Wrap

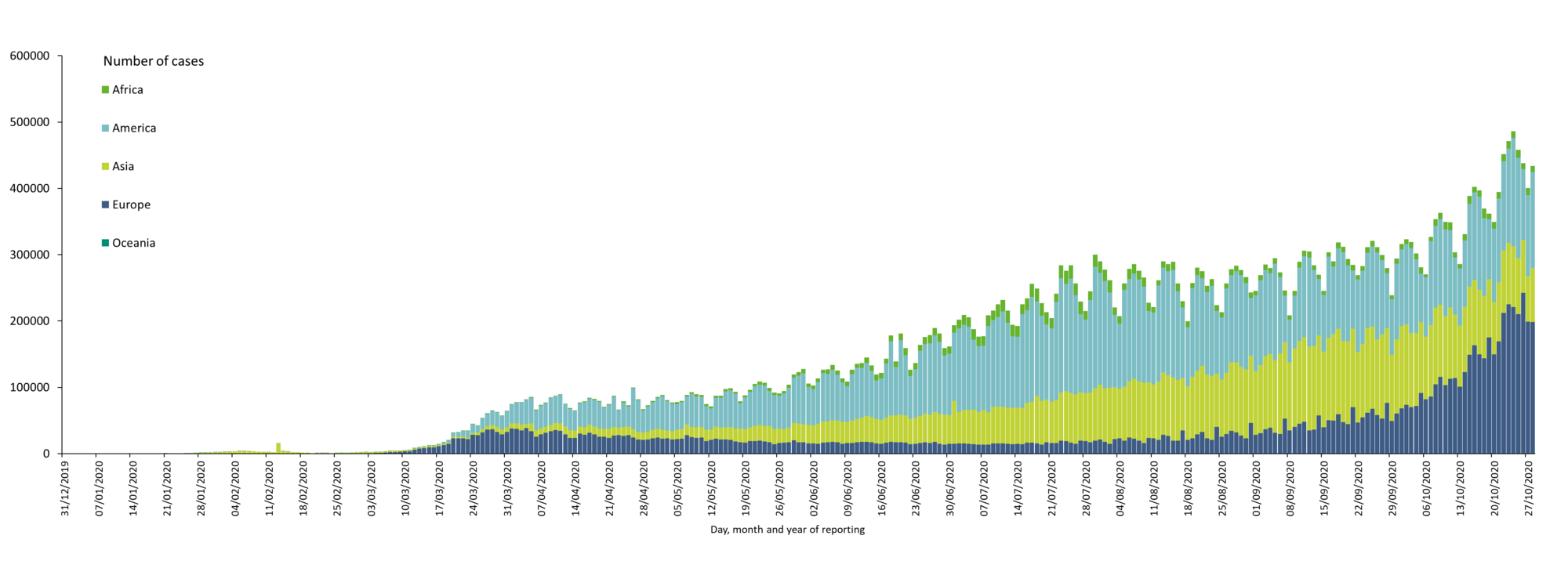

German Chancellor Merkel announced fresh Covid-related restrictions, closing bars, restaurants and leisure venues for one month from Monday, but leaving most businesses operating, Officials will gather again in two weeks to assess the impact of the measures. The French government is poised to impose tighter restrictions after a night-time curfew failed to halt a surge infections. Switzerland closed nightclubs and imposed other new limits. New York cases topped 500,000, while hospitalisations in neighbouring New Jersey exceeded 1,000 for the first time since July. The two states, the early focus of the U.S. outbreak, have seen a resurgence in recent weeks.

US Sep. advance goods trade balance deficit narrowed to -USD79.4bn (est. -USD84.5bn, prior -USD83.1bn) due to the first pullback in imports in four months. Sep. wholesale inventories fell 0.1%m/m (est. +0.4%m/m) but retail inventories rose +1.6%m/m (est. +0.5%m/m), the latter related to pre-festive season stocking.

Band of Canada left is policy rate unchanged as expected, but the tone of its statement and subsequent press conference indicated potential to increase QE, despite an interim pullback in weekly bond purchases to CAD4bn from CAD5bn. Extended forward guidance and concerns over a slower future growth path due to prolonged COVID-19 impacts were noted.

Event Outlook

Australia: The Q3 import price index is expected to print at -2.0% as the AUD rebounds, offsetting higher fuel prices (prior: -1.9%). The higher AUD has also seen AUD denominated commodity prices fall, leading Westpac to forecast a 3.5% decline in the export price index.

NZ: ANZ business confidence will be finalised for October, the flash result earlier showing a rebound almost to pre-Covid levels.

Euro Area: The deterioration in Europe’s growth prospects associated with the ‘second wave’ of infections now being seen will start to impact the EC survey of economic confidence in Oct (prior: 91.1, market f/c: 89.6). The ECB’s policy meeting is also expected to highlight these intensifying risks.

US: GDP is expected to bounce back strongly in Q3 following a historic 31.4% decline in Q2. Household demand is expected to lead the recovery, with Westpac and the market seeing a 28% and 32% annualised rebound respectively. Initial jobless claims high level signal labour market churn and uncertainty, but pending home sales continue to show strength, having reached a record high as a result of low mortgage rates and households’ increasing desire for the best home possible (prior: 8.8%).

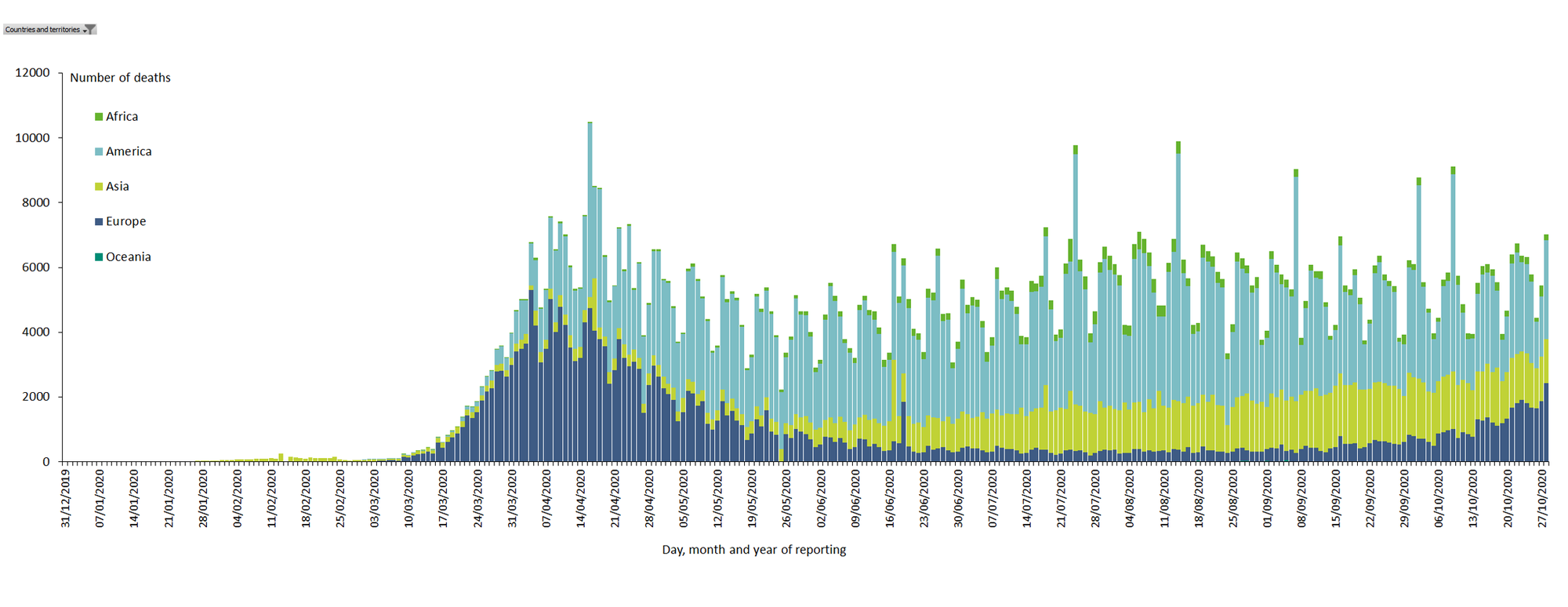

The virus is out of control, to put it mildly, with European and US deaths surging:

The sequence of risks is extreme. Europe is progressively locking down. We are only in October so this has six months to run on and off. It faces Hard Brexit and limited extra fiscal.

The US is entering an election that will likely result in a Biden Administration which will have to follow Europe’s example with at least partial lockdowns nationally and more intense lockdowns locally. Yet the incumbent Trump Administration is openly preparing a coup to steal the election and could use prospective lockdowns as a part of its war on democracy.

Even if we get through that, there is no fiscal support left for this year as partisanship takes over (there is still a chance of a lame duck senate passing a $500bn package by, say, Xmas) and any attempt to remedy the virus post-election by the Biden Administration will likely result in very serious civil conflict as traumatised Trumpians take to the streets.

As well, markets are positioned entirely on the other side of the boat. They are massively short DXY on the vaccine recovery and Biden stimulus trade:

And massively long stocks, especially those that benefit from a falling DXY such as tech, commodities, EM etc.

Markets have fully repeated the mistake of February 2020 and the Australian dollar is square in the gun.