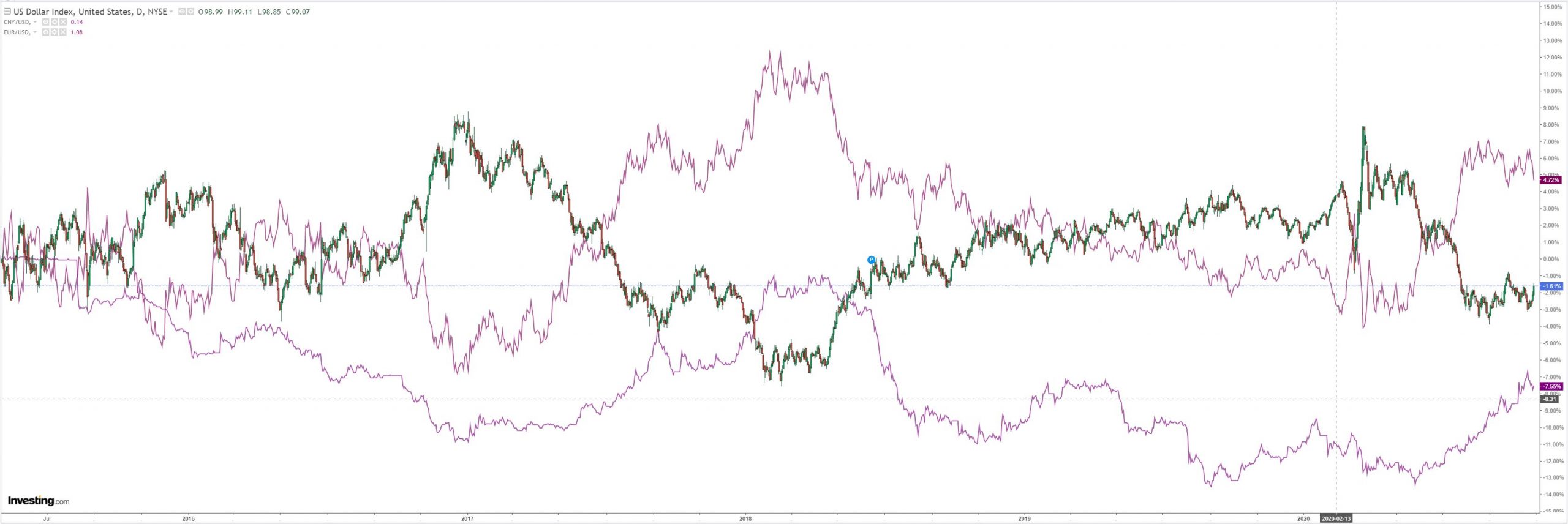

DXY is up and away as EUR sinks:

The Australians dollar was hammered:

Gold is close to a major technical break:

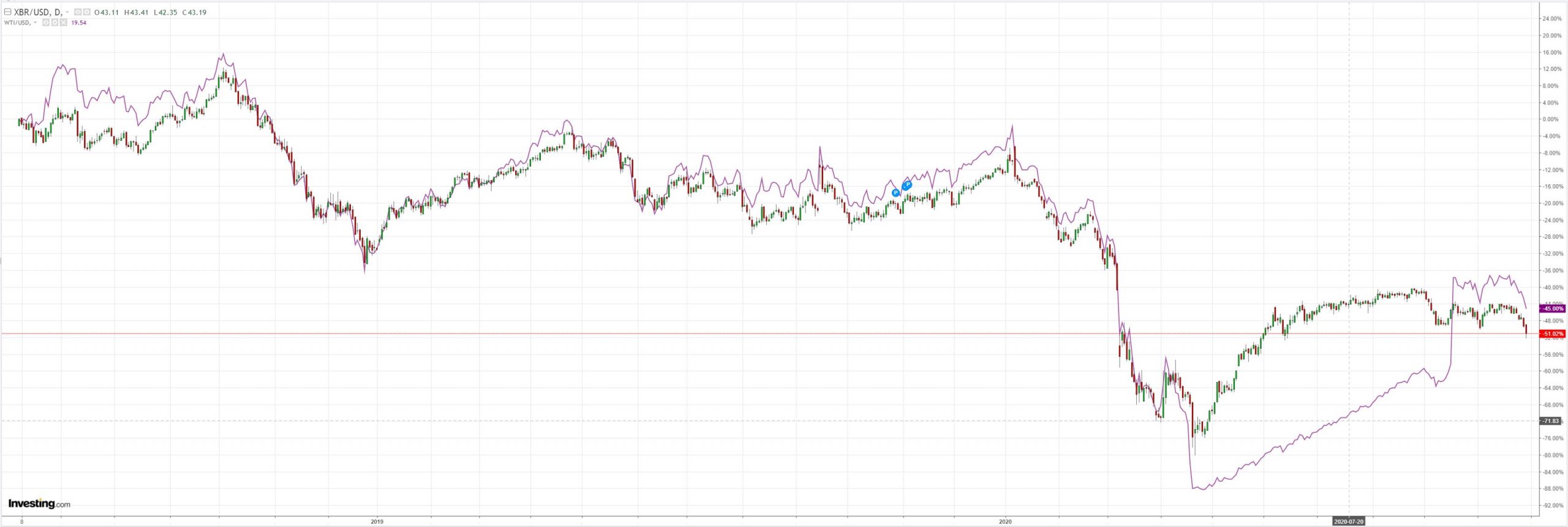

Oil is already through the same:

Metals fell:

Miners bounced:

EM stocks too:

Junk was OK:

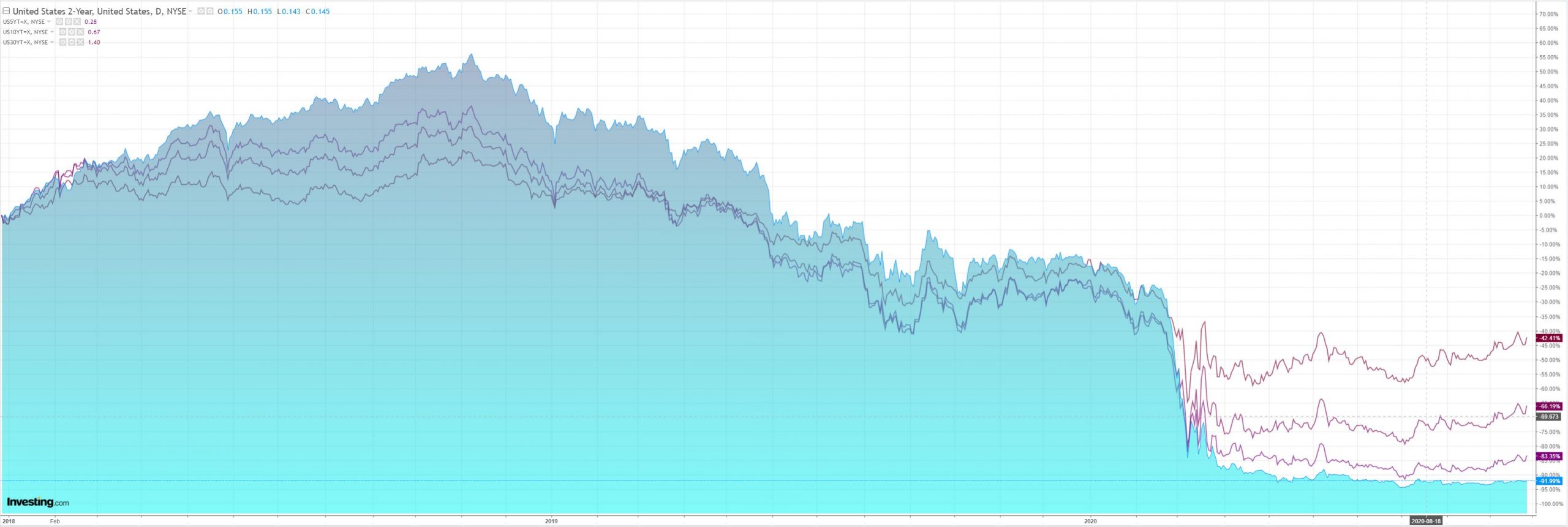

Treasuries were flogged:

Stock pain is forgotten:

Westpac has the wrap:

Event Wrap

US 3Q GDP rose +33.1% (qtly, annualised) – a record rise and slightly above the +32.0% median expectation (prior -31.4%). Personal consumption was notably strong at +40.8% (est. +38.9%, prior -33.2%). Although growth is expected to continue in 4Q, the rise of Covid infections in US and globally, and the current profile from 3Q, still leaves activity 3.5% below its peak. Initial jobless claims grew 751k (est. 770k, prior revised to 791k from 787k), with continuing claims pulling back to 7,756k (est. 7,775k, prior revised to 8.465k from 8.373mn). Sep. pending home sales faltered for the first time in five months, falling 2/2%m/m (est. +3.0%m/m), though still rising +21.9%y/y (est. +23.0%y/y, prior 20.6%y/y).

The ECB left policy on hold while clearly indicating that they would respond to increasing downside risks with further accommodation in December. Asset purchases programmes (including their EUR1.35tr PEPP) were left unchanged, as were LTLRO III targeted funding facilities. It said it would “recalibrate its instruments” once it received December staff macroeconomic projections. While the ECB was widely expected to open the door for a December easing, this was a more explicit preparatory statement. The press conference added emphasis, with Lagarde saying the economy was already losing momentum after its summer activity rebound and is now facing deeper downside risks.

Event Outlook

Australia: Private sector credit is contracting and there is prospect for further falls as Covid’s economic shock reduces the appetite for debt. Westpac expects the weakness in business and personal credit to continue, whilst housing credit grows modestly (total private credit: market f/c: 0.1%; Westpac f/c: -0.1%). The Q3 PPI will follow; higher fuel costs are expected to be offset by a stronger AUD and soft demand (prior: -1.2%). Also, the result of the 2019-20 annual re-benchmarking of the national accounts will be released.

NZ: ANZ consumer confidence should reflect lingering uncertainty for NZ households (prior: 100).

Japan: Lower food and energy prices are expected to weigh on the Oct CPI (prior: 0.2%/yr, market f/c: -0.2%/yr).

Euro Area: GDP had its largest contraction on record of -11.8% in Q2. The unwinding of strict containment measures in May and June point to a rebound in Q3 (market f/c: +9.6%, Westpac f/c: +9.0%). But, with cases surging once again, risks are to the downside for both Oct’s CPI (prior and market f/c: 0.1%) and Sep unemployment (prior: 8.1%, market f/c: 8.3%).

US: Personal income growth should flatten at an expected 0.3% as unemployment aid rolls off, whilst personal spending continues to be supported by food and healthcare spending (prior and market f/c: 0.1%). The Q3 employment cost index is likely to reflect substantial labour market slack, with wage growth expected to moderate to 0.5%. Elevated virus counts and a lack of fiscal relief will challenge the recovery in Uni of Michigan sentiment too(prior and market f/c: 81.2).

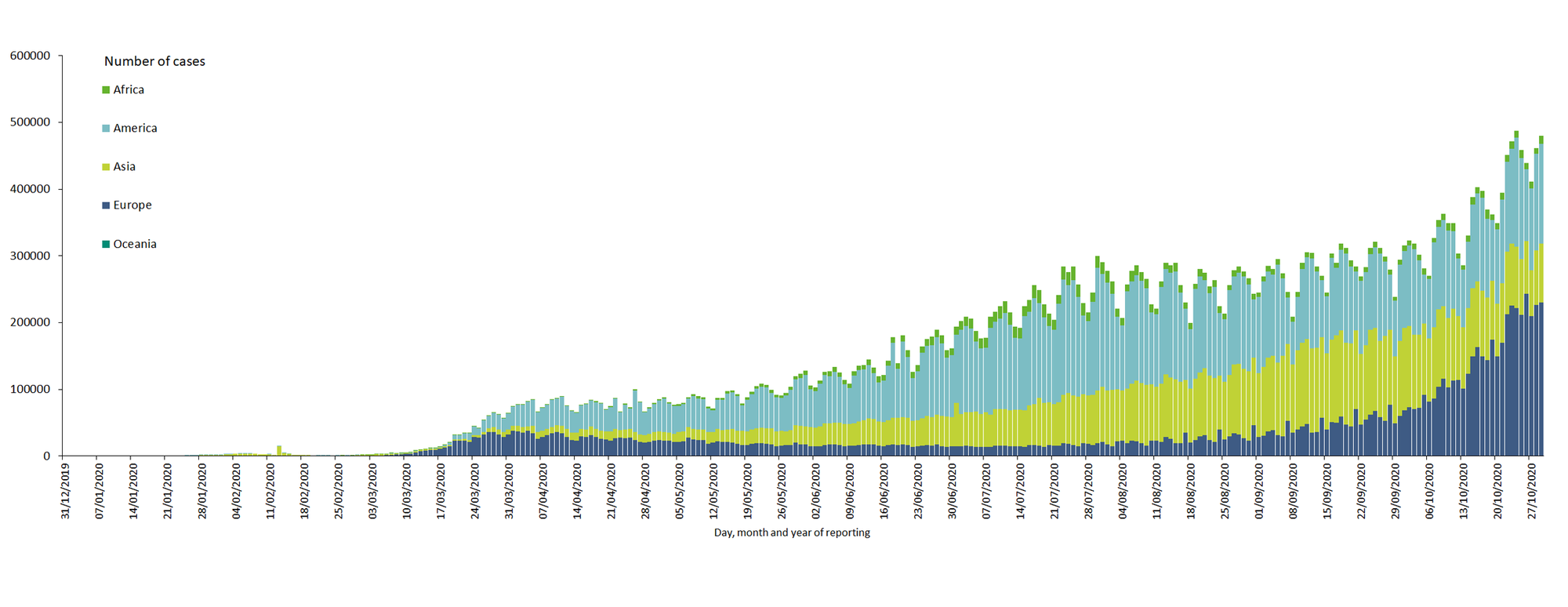

The virus marches higher across the North Atlantic:

It’s an absolute mess of signals. The Treasury curve wants to steepen into a “blue wave” election recovery and inflation even as oil plummets. But DXY is rising strongly, the classic risk-off signal and obviously bearish for inflation everywhere. Equities can’t decide, either way.

Much of the confusion is related to the election. Yesterday’s polling and court action over mail-in ballots were bad for Trump so the market lifted on the hope of an uncontested result. But the risk of Joe Biden is also more lockdowns, doubtless of the “lite” variety, but bad for activity nonetheless. Economic signals are softening but not terrible:

Then there’s the senate and stimulus to worry about, as well as still hugely over-priced stocks.

In short, it’s a mess and Australian dollar falls are reflecting that.