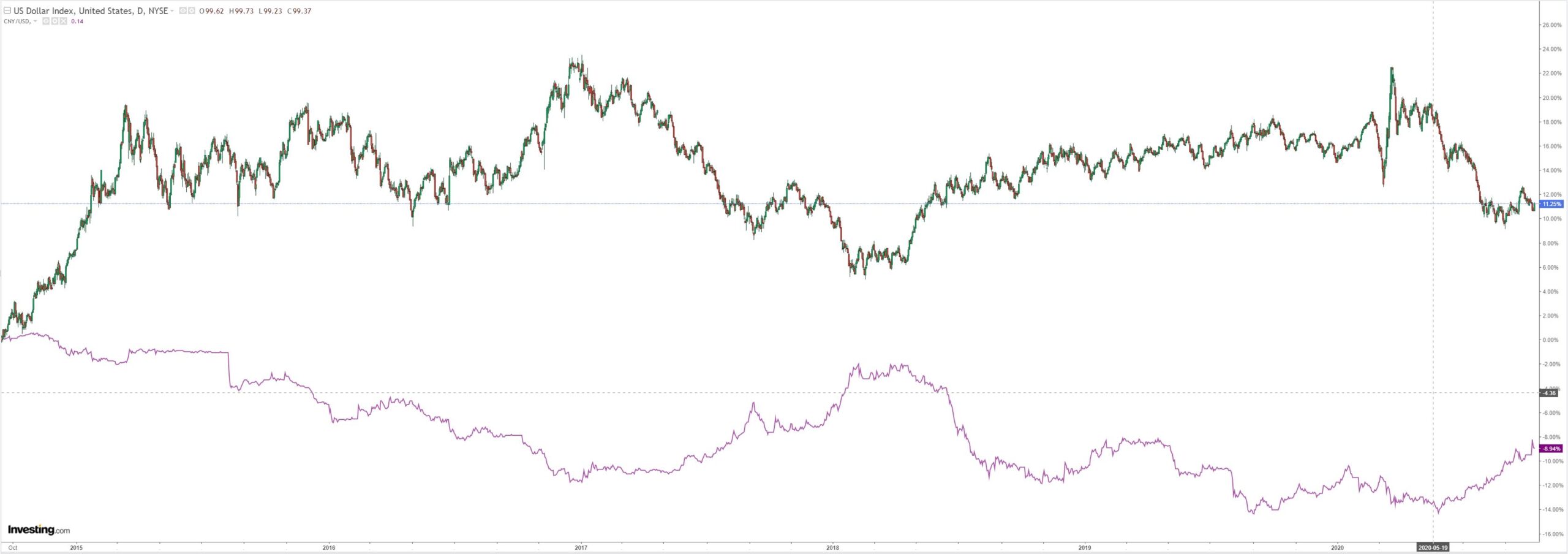

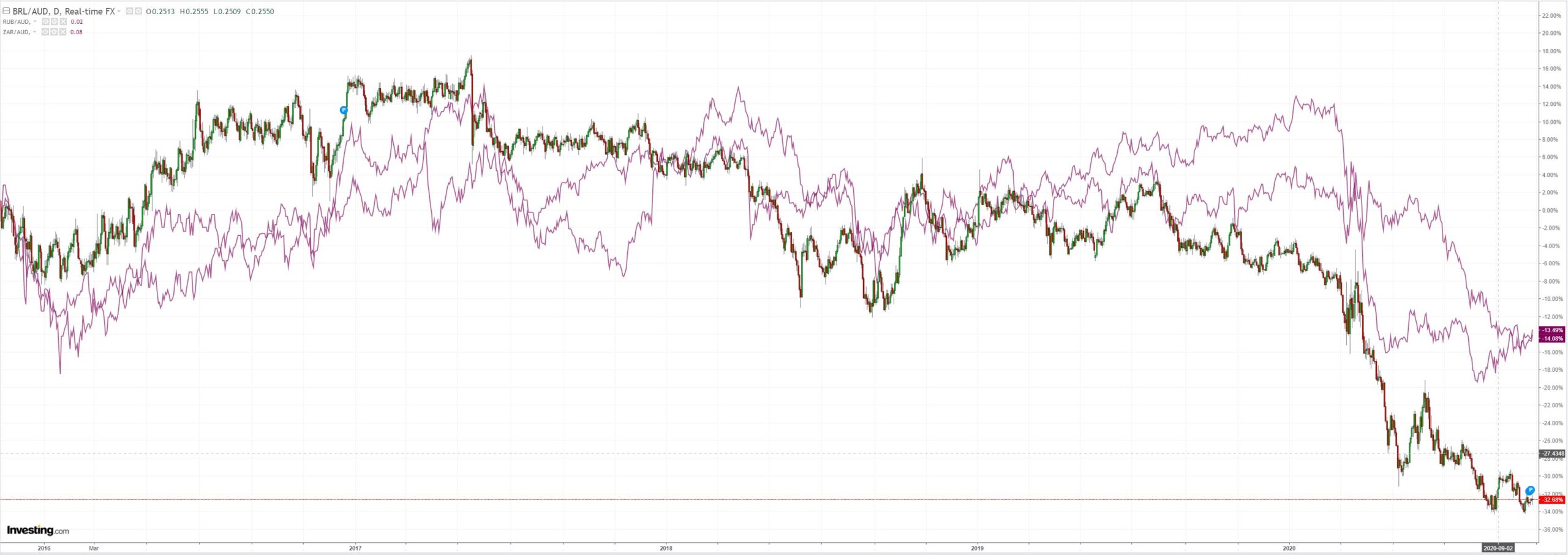

In fact, the entire EM and commosities complex sagged:

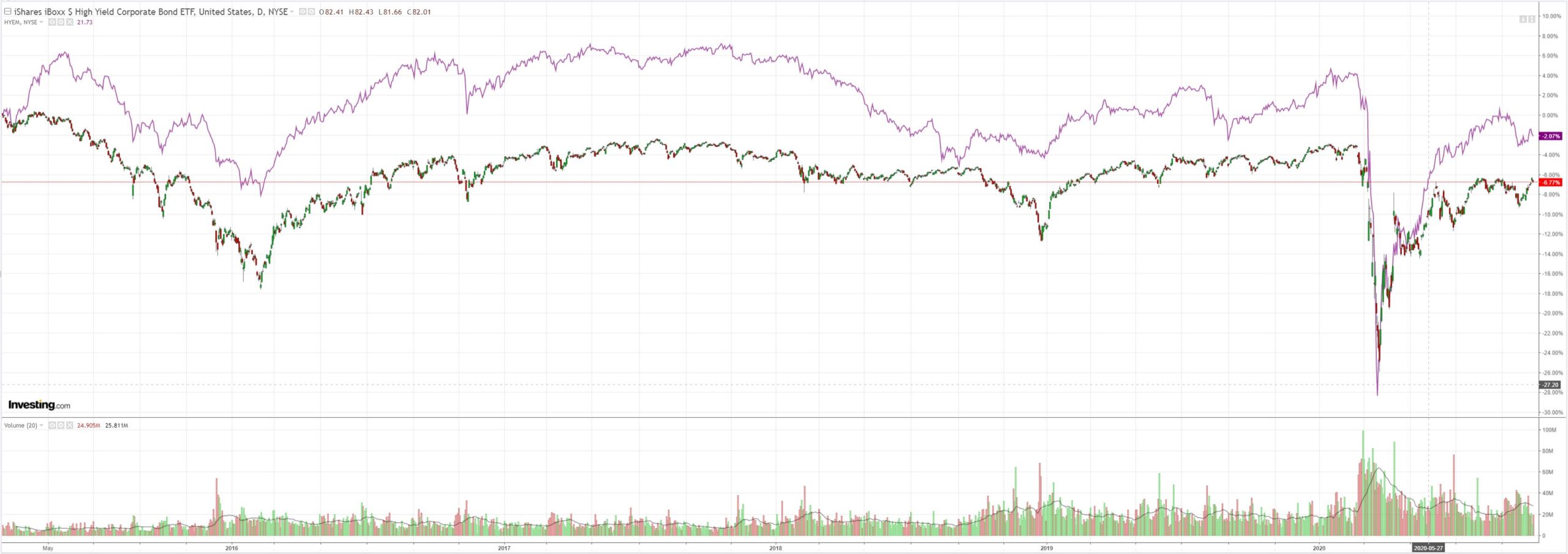

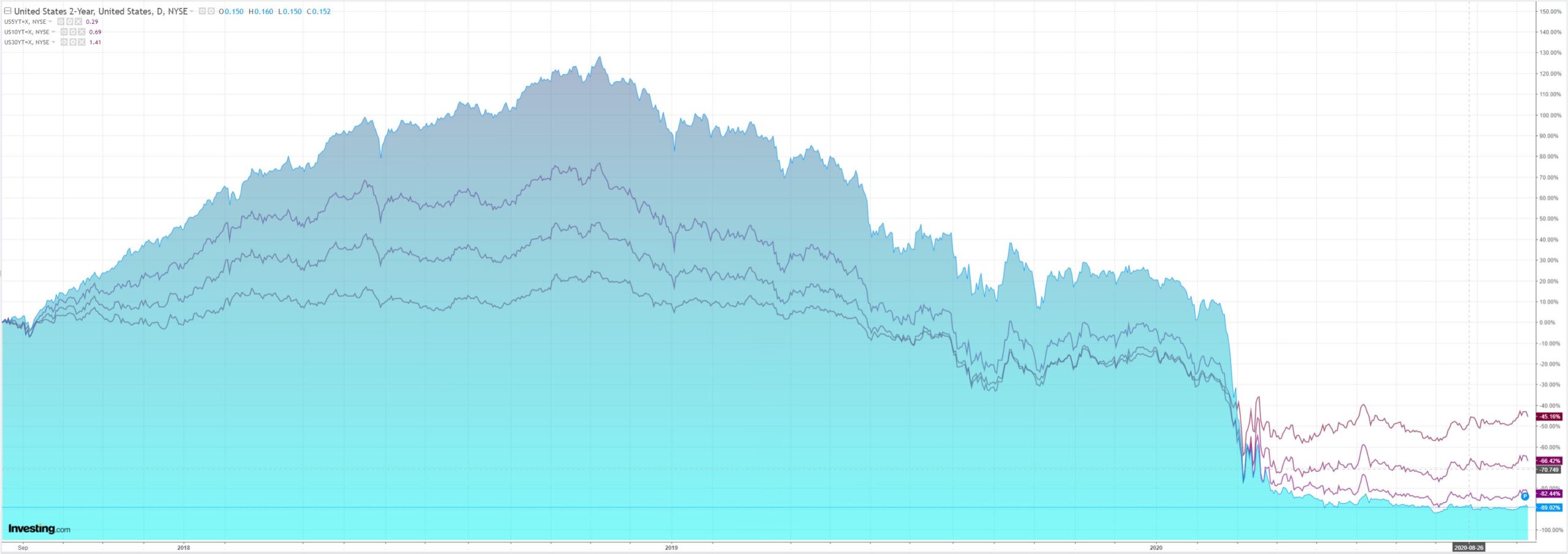

Treasuries rallied hard:

Advertisement

Stocks only go up:

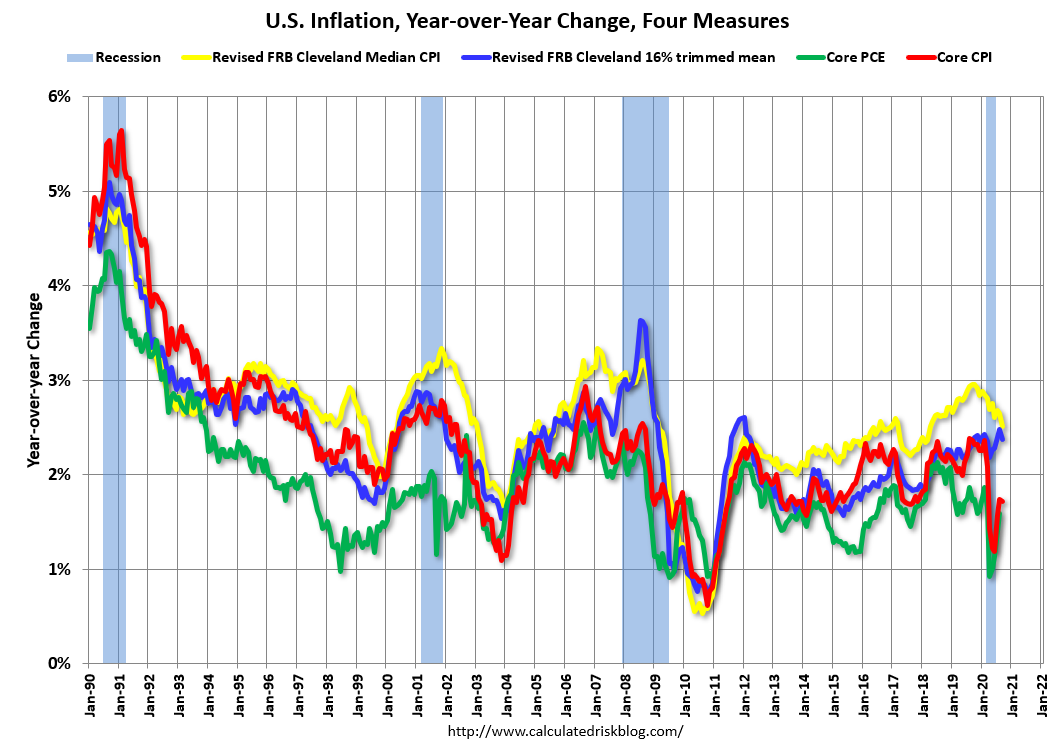

Not much in data but US core inflation remains very weak:

Advertisement

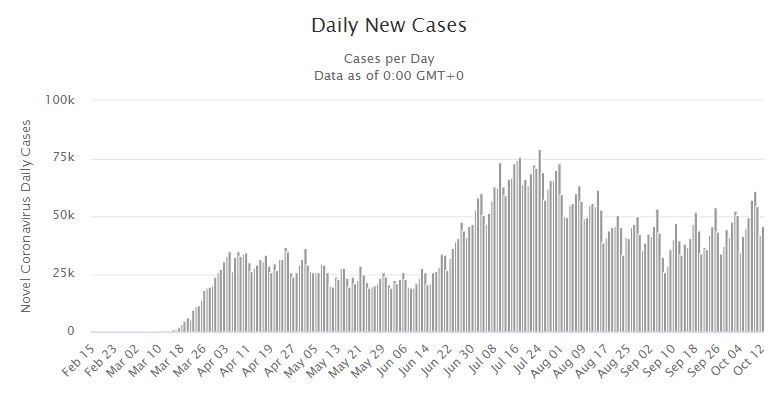

And the virus very strong:

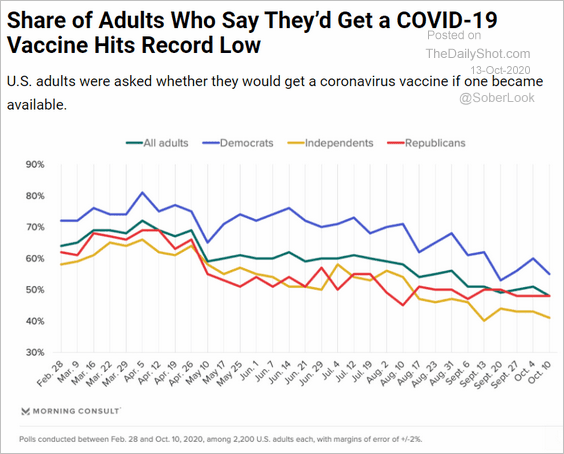

Two vaccines are now offline with Johnson&Johnson and Ely Lily in pauses as mysterious illness strike patients. Vaccine efficacy is waning anyway:

Advertisement

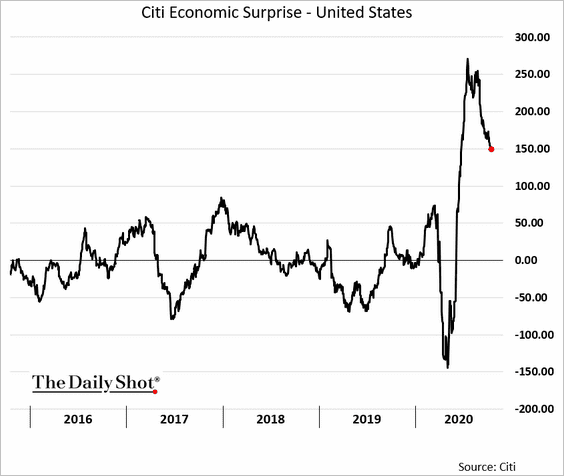

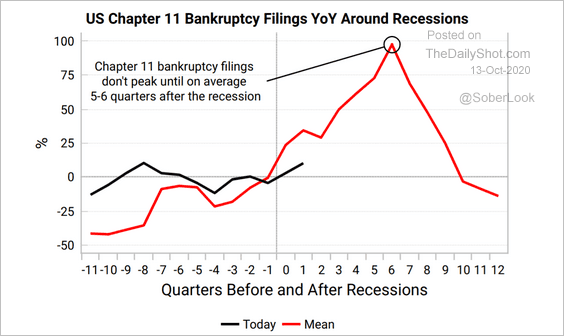

The economic recovery is fading:

And the election is approaching:

Followed by:

Advertisement

So, still plenty of risk in the chamber for forex to calculate and weigh on the Australian dollar.

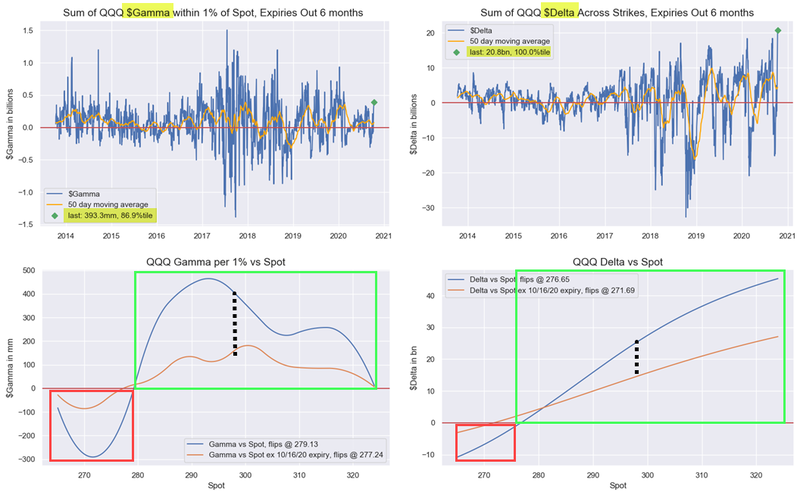

The major offset is stocks where robots keep buying robots but even that has its limits, from Nomura’s Charlie McElligott:

…the market “gets” the Dealer “short Gamma” dynamic in mega-cap single-names with very large open interest outstanding (remember, the large Oct expiries from the Aug Calls / Call Spreads were in AMZN, ADBE, GOOG and NFLX) and are in the process of self-fulfilling near or even through the strikes which the Dealer(s) is short and thus forced to aggressively Delta hedge…

…just like the Aug / Sep “pivot” from extreme grab to extreme vomit, if we were to continue rallying into Friday’s expiration, there will continue being a ton of stock to buy for the Dealers to remain delta hedged and extend the melt-up (i.e. late Aug)—but if we roll over and the individual stocks trade well below the strikes and the options again look “worthless” (back to last week’s levels, LOLOL), there then would be a massive puking of all that Dealer delta hedge, just like the Aug turn into Sep expiry (Note: the same thing would occur if the client were to unwind the position).

In my eyes, we are not quite at that same “vol up, spot up” red-flag level just yet as said Aug / Sep swing, particularly bc the delta hedging is still far too “real” here as judging by NQA +103bps early today vs ESA -6bps and RTYA -92bps – there is just too much convexity out there and it is forcing the standard “short Gamma” into a rally perversion of “buying more to stay hedged the higher it goes”

As I said yesterday however, next week – post Op-Ex – could see spot markets get very “binary,” with the latest index-level options analysis showing that 32% of the Gamma in SPX / SPY is set to come off, and an incredible 60% of the Gamma in QQQ set to roll-off after this expiry – and all with $Delta back at historical super-extremes (SPX at $452.2B – 97.5%ile, QQQ at $20.8B – 100%ile).

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.