DXY was up last night but not a lot:

Australian dollar rose against most DMs:

And EMs:

Gold was flat:

Oil is in trouble again as Libya disgorges barrels galore:

Metals fell:

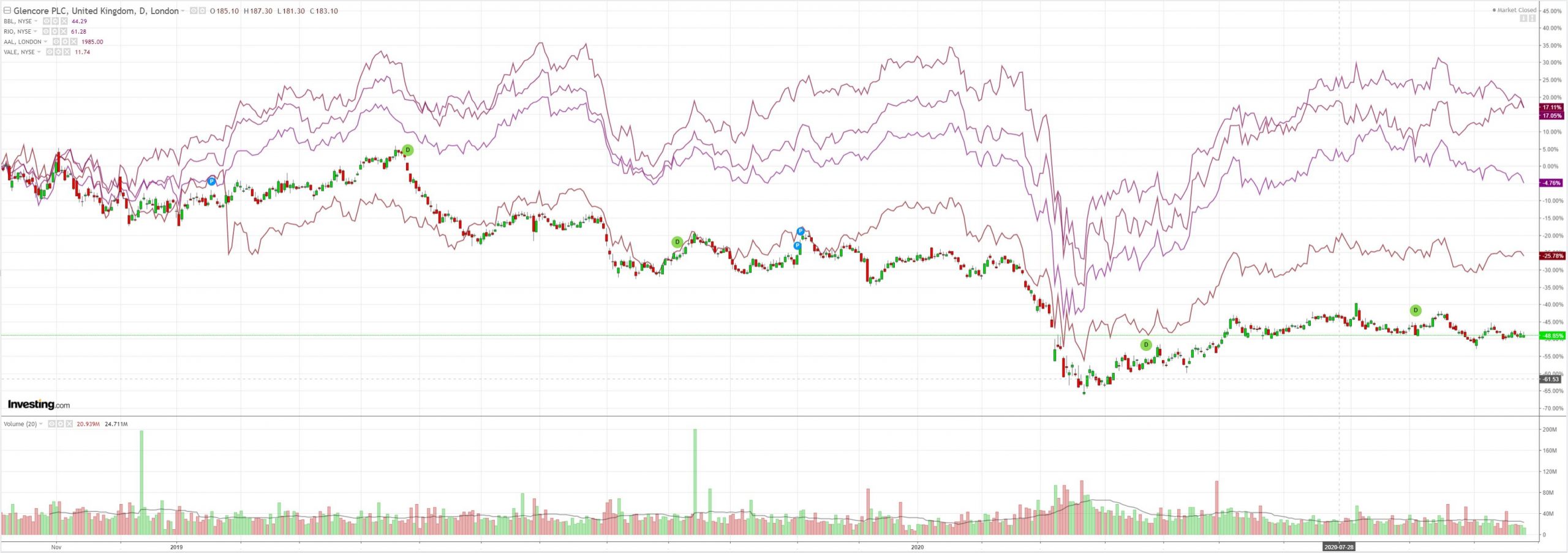

Miners were hit:

EM stocks too:

Junk was mixed:

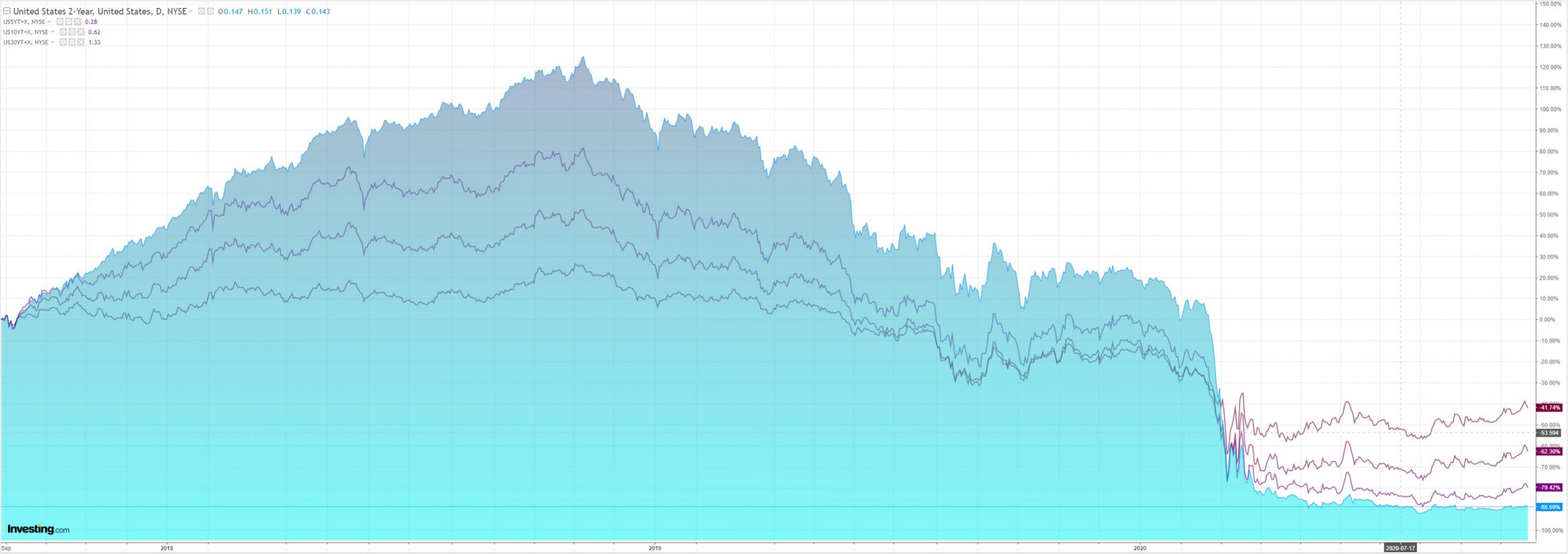

The crazy Treasury back up ran screaming for cover:

Stocks are in danger of printing one of the truly great double tops:

Westpac has the wrap:

Event Wrap

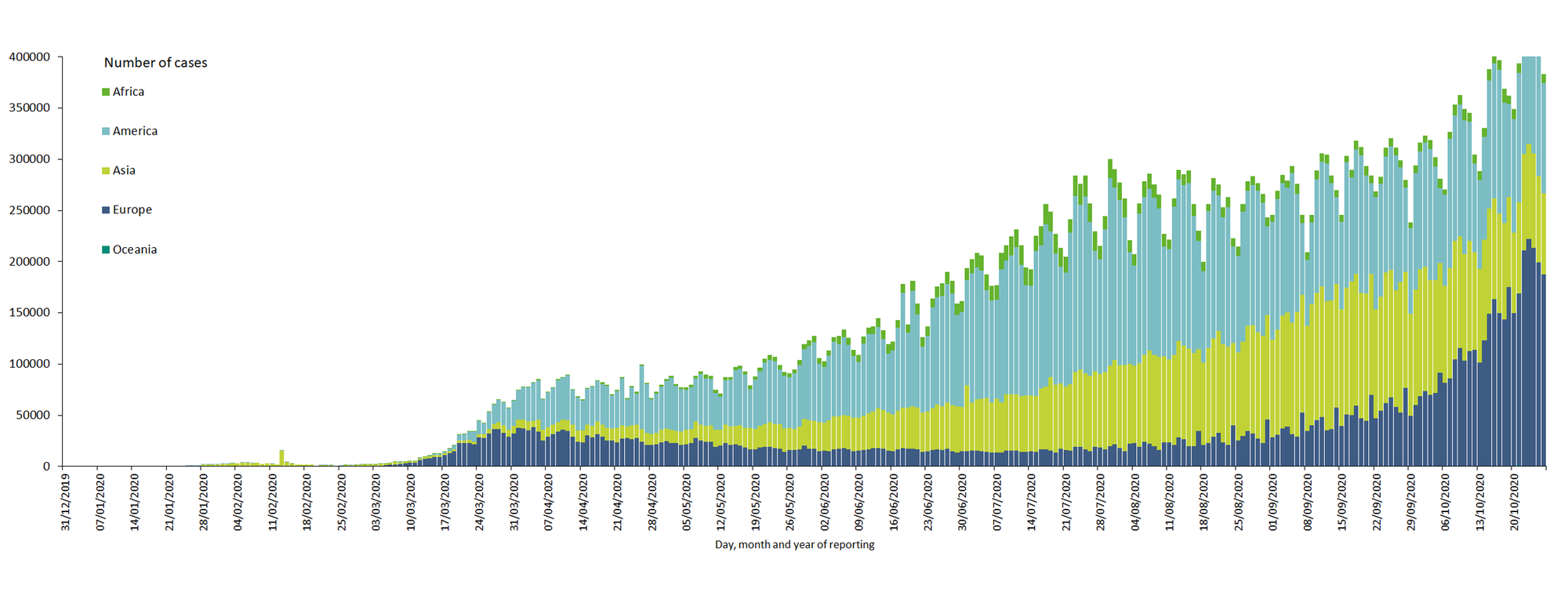

Covid-19 cases in the U.S. made a daily record of 85,000 on Saturday. The World Health Organization’s director general said the northern hemisphere faces a “dangerous moment” as Covid-19 cases have surged.

White House economic adviser Larry Kudlow said that while stimulus talks were ongoing, President Trump cannot accept parts of the plan the Democrats have proposed.

U.S. new home sales fell 3.5% to 959k in September, disappointing expectations (est. 1025k). Sales had surged from May to August by a cumulative 61% following a three-month pandemic-related plunge of 29%.

Dallas Fed manufacturing survey rose 6.2 points to 19.8 in October (vs est. 13.5). This is the third month in positive territory after five negative prints, the region hit by the double whammy of the pandemic and weakness in weakness in the oil industry. Gains were broad-based, although the employment fell to 8.7 from 14.5. Chicago Fed national activity survey slipped -0.84 points to 0.27 in September. The index was at a record high of 5.93 ,in June after a record low of -17.74 in April.

German Ifo business confidence survey fell from 93.2 to 92.7 in October (vs est. 93.0). The current conditions indicator continued to improve, but the future expectations reading fell as virus developments undermined confidence in the recovery. The breakdown showed that services and trade were mainly hit by the jump in new case numbers and associated restrictions in Europe.

Event Outlook

Australia: RBA Deputy Governor Debelle and Assistant Governor (Financial System) Bullock will appear before the Senate Economics Legislation Committee (13:30 AEST). Assistant Governor Bullock will also give a speech at the Ayr Chamber of Commerce at 18:30 AEST.

New Zealand: Exports are expected to soften in Sep, widening the trade deficit (prior: -$353m, market f/c: -$1015m).

China: Industrial profits saw double-digit growth of 19.1%/yr in August, reflecting continued recovery in production and stronger exports.

Euro Area: M3 money supply is anticipated to moderate in September (prior and market f/c: 9.5%), though the second wave of cases is raising the prospect of additional easing.

US: Durable goods orders are set to track sideways in Sep at an expected 0.5% pace as transport and machinery orders slow. The forward-looking Conf. Board’s Consumer Confidence is also likely to be little changed at 101.8. Strong demand and low interest rates have seen FHFA house prices rise 6.5%yr, though depleted inventories are a potential headwind for further gains (prior: 1.0%, market f/c: 0.7%).

It’s all about the virus again now as it runs wild in both Europe and America:

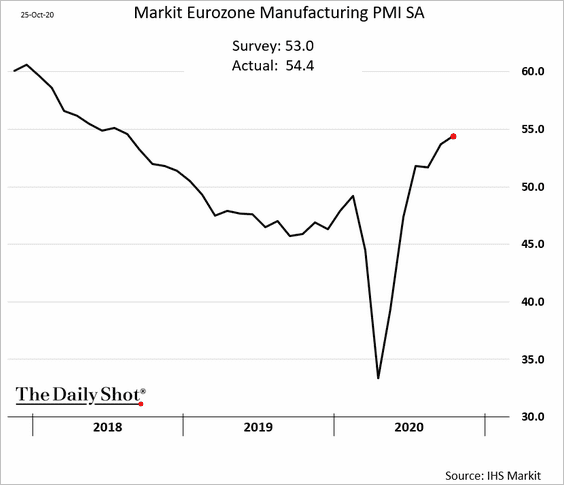

Lockdowns are underway in Europe with Germany joining in last night. So far they are of the “light” variety but good luck with that as winter deepens. So far, manufacturing is OK as the global inventory cycle plays out:

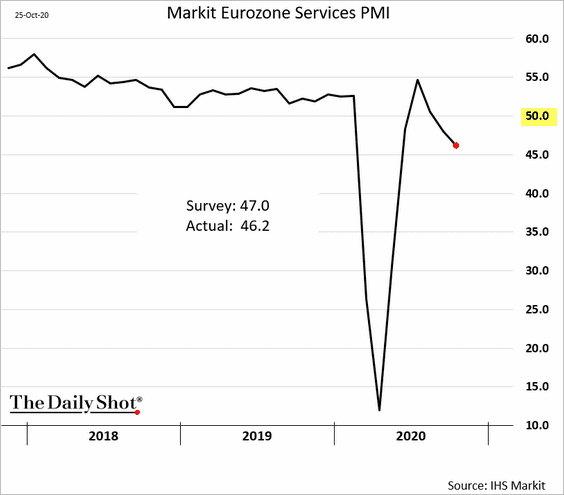

But services are leading the decline:

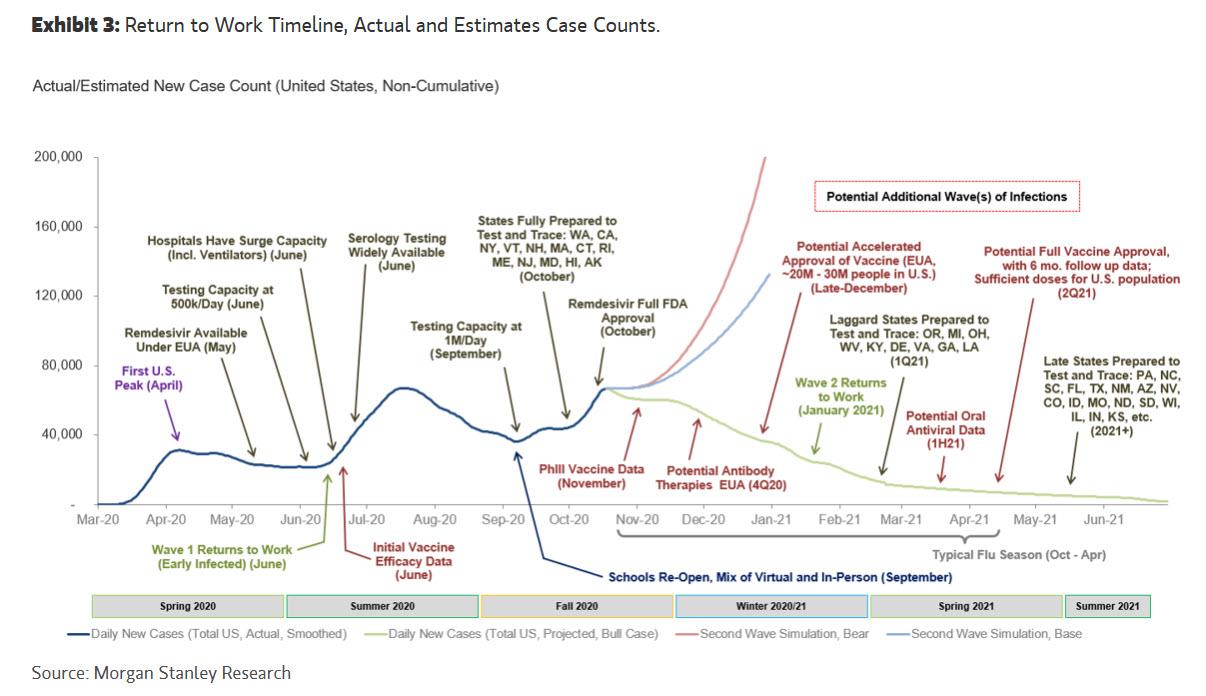

It’s the same in the US though lockdown there will be slower. Morgan Stanley offers the anything could happen chart:

The equation is straightforward. The less the government does, the more the private sector will do. There is no avoiding lockdown. I expect we’ll follow that base to bearish case (blue and red lines) of virus cases until the death count is bad enough that the US private sector closes its doors. Then the virus will peak again and trend lower.

Unfortunately, there is still no fiscal support in sight and the best case is a lame-duck passage if the ‘blue wave’ gets up but there are doubts even about that.

The virus is about the tear the heart out of the North Atlantic economies and the Australian dollar is no safe harbour in that event.