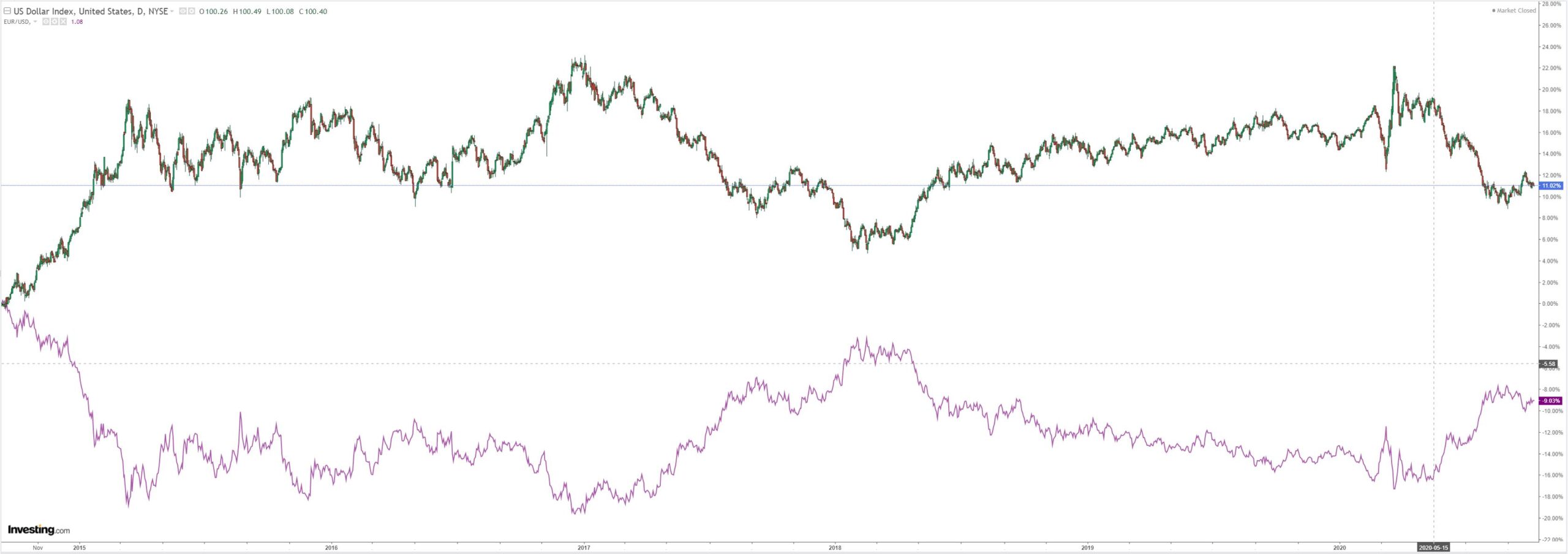

DXY was soft last night:

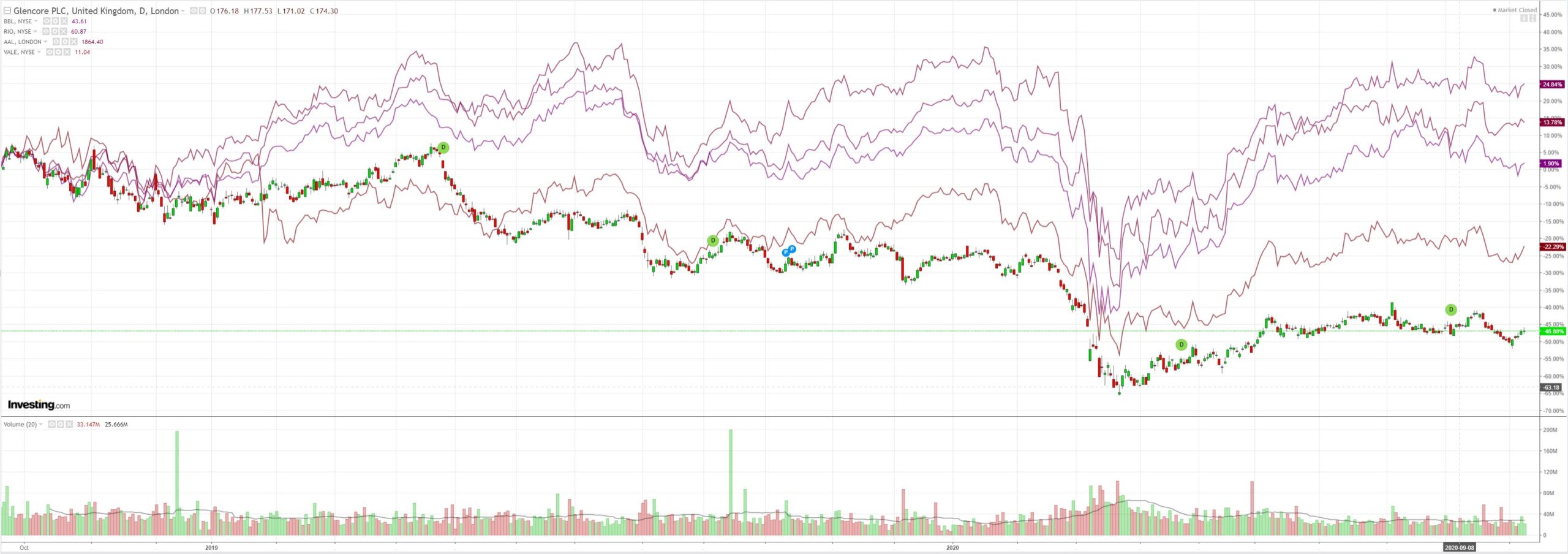

Which had all of the usual effects with AUD, EM and commodities all posting gains:

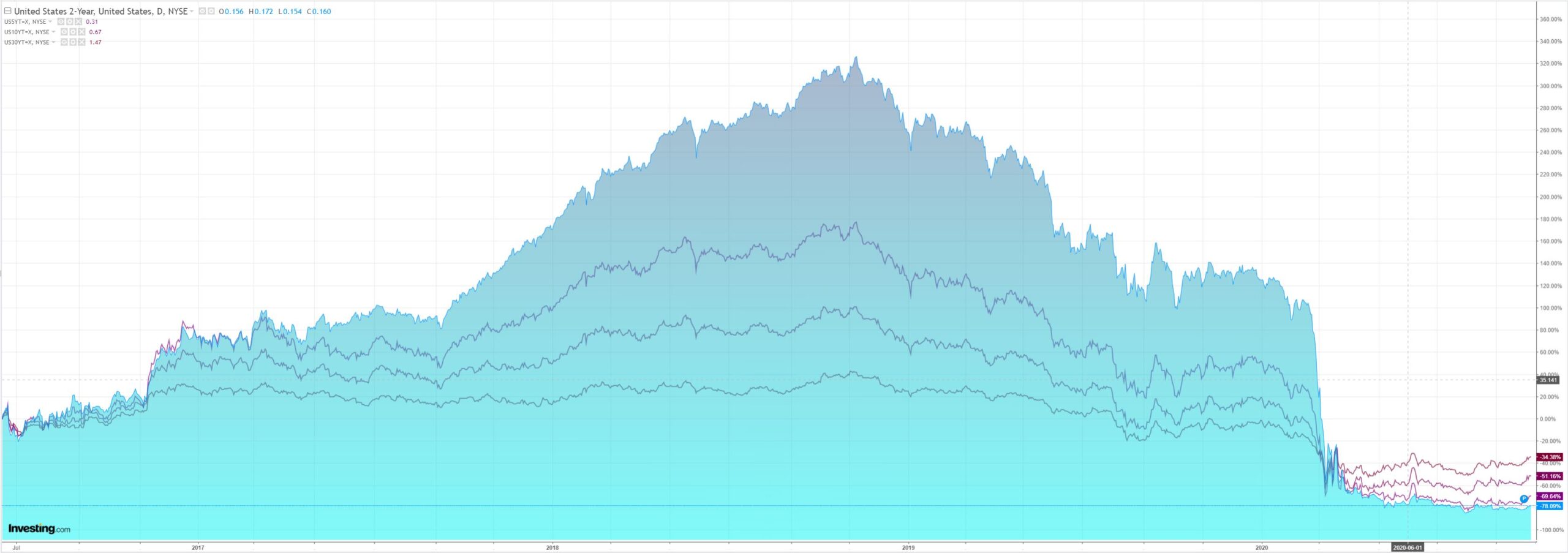

Treasury yields were flat:

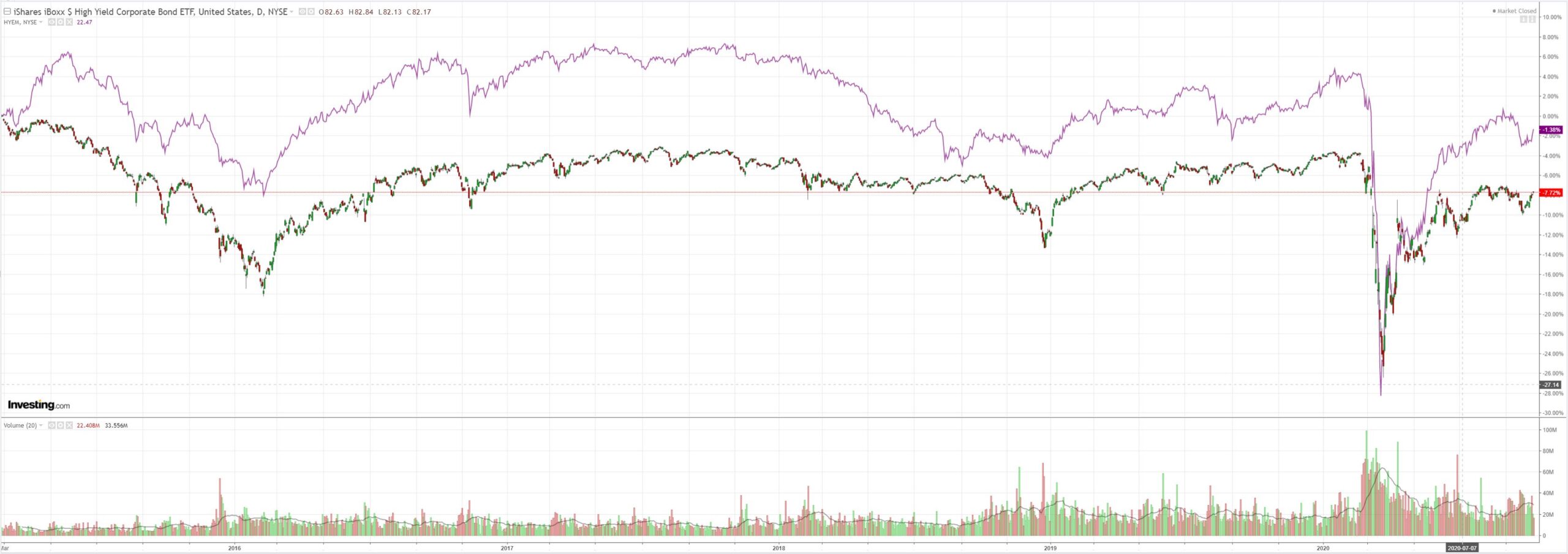

And the stock bubble returned:

Westpac has the wrap:

Event wrap

Once again, the lack of key data in the North Atlantic meant that markets awaited comments from policy makers and politicians. Central Bank speakers stressed their preparedness to use further easing tools if needed whilst comments on EU/UK post-Brexit talks remained cautiously optimistic.

Trump pulled out of the 2nd televised debate, after the decision was taken to make it a virtual event while polls suggested that Biden’s lead has widened further.

US weekly claims data provided little market direction. Initial claims at 840k were marginally above the Bloomberg average estimate but close to the median of continued wide ranges in estimates. The encouraging slip in continuous under 11mn (10.976mn, ave. est. 11.4mn) was more pronounced.

Germany’s August Current Account surplus was close to market estimates at EUR16.5bn (est. EUR 16.2bn) with both exports and imports rising more than anticipated. However, it had little market impact.

French daily COVID case count remained uncomfortably high at 18,129, but below yesterday’s over 19k. UK posted a lift in cases to 17,540 (a trebling in 2 weeks and up from yesterday’s 14k).

UK and France are again looking to increase restrictions.Event Outlook

Australia: Housing finance approvals posted a strong rebound throughout June-July. Westpac expects this to falter in August under the weight of Victoria’s second lockdown (prior: 8.9%, market f/c: 1.0%, Westpac f/c -1.5%). Owner occupier finance (prior: 10.7%, Westpac f/c: -1.0%) and investor finance (prior: 3.5%, Westpac f/c: -3.0%) are both expected to deteriorate.

The half-yearly RBA Financial Stability Review will be released at 11:30 AEST.

US: Wholesale inventories growth has returned to positive territory, supported by durable goods restocking (prior and market f/c: 0.5%).

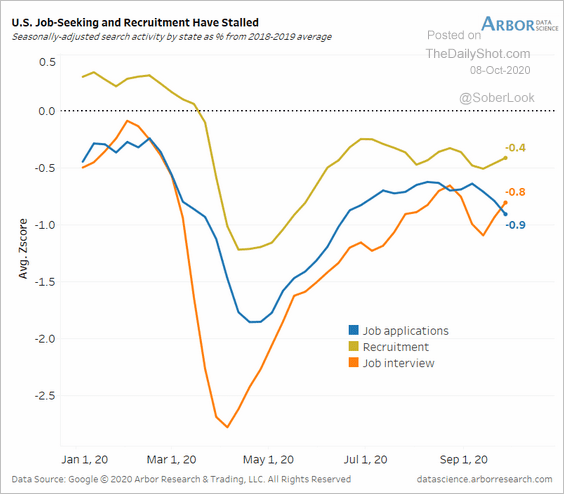

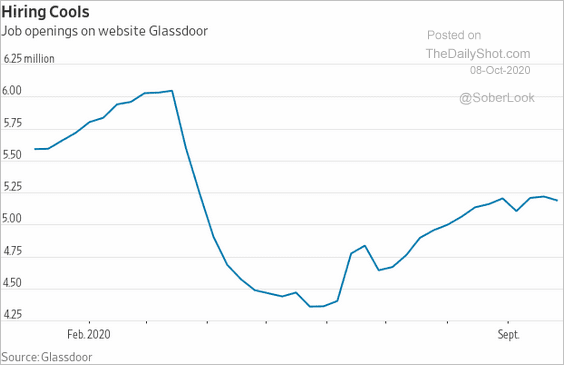

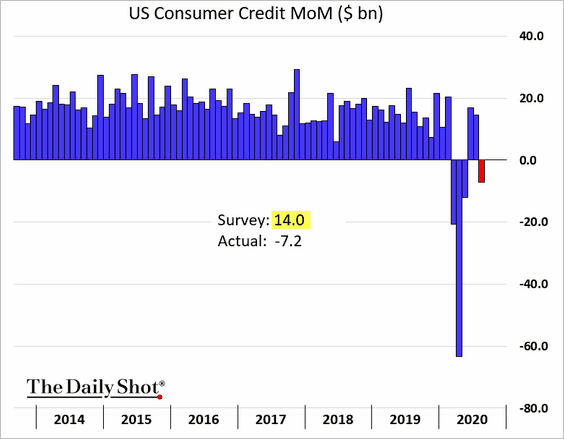

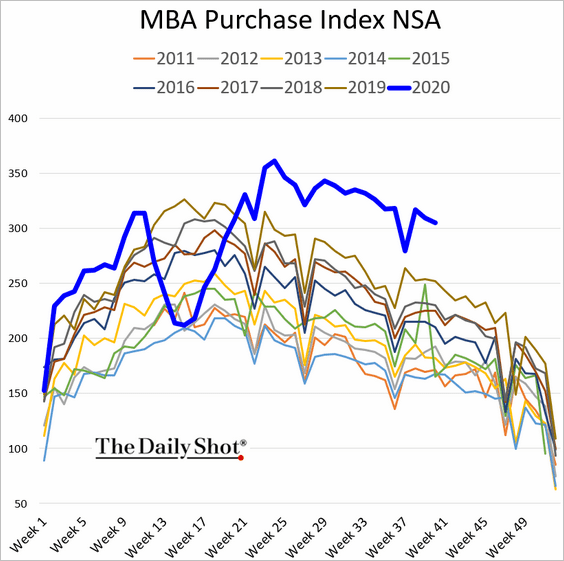

Price action was pushed around by the usual combination of stimulus balderdash. It’s not coming but the market likes to pretend that it is. Meanwhile, the recovery is sliding away:

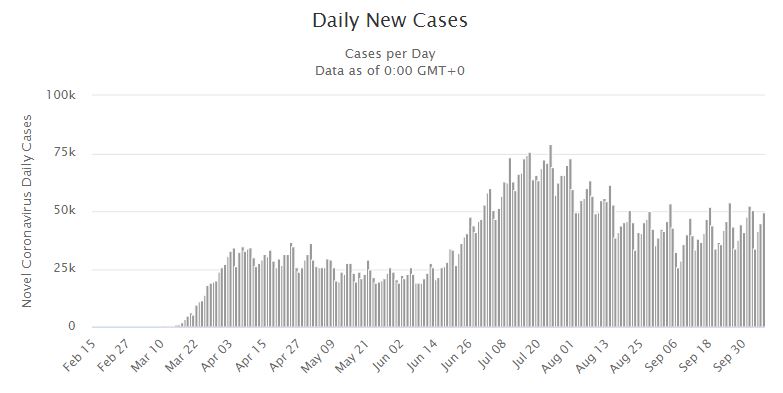

And, the virus third wave is delicately poised:

But, Wall St is nothing if not flexible and it has now moved on to the positives of the “blue wave” election:

The problem is equity valuations make absolutely no sense. And while that remains the case the Australian dollar remains vulnerable.