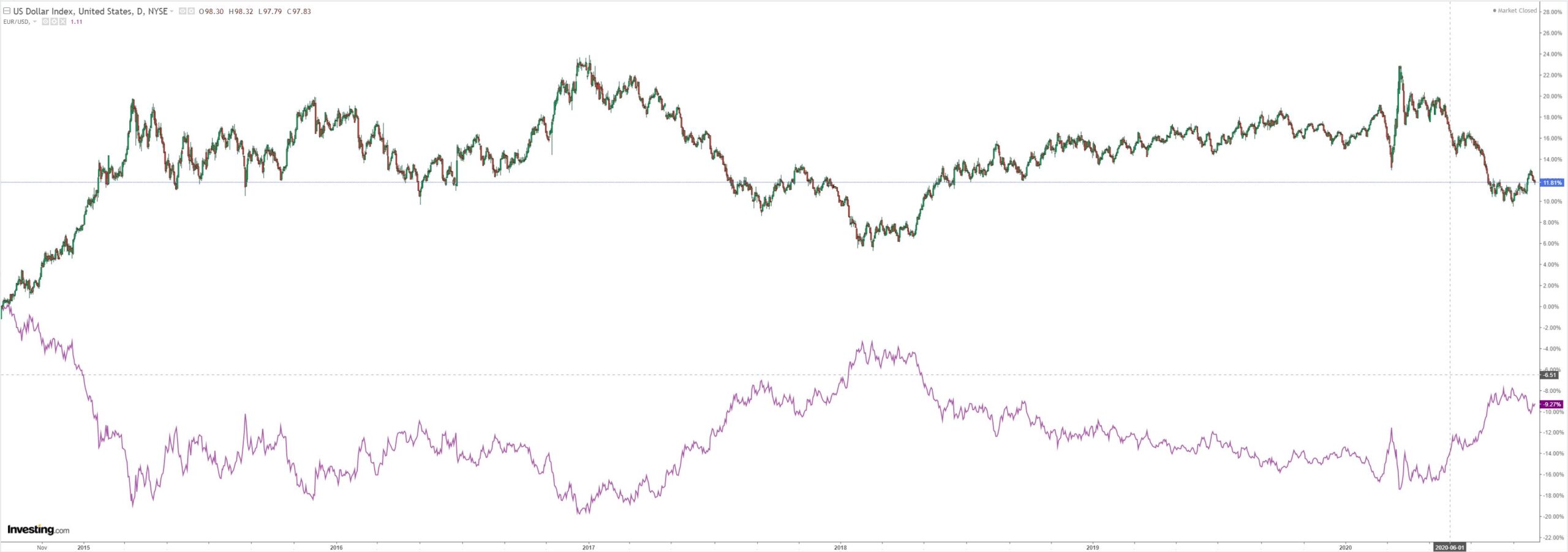

DXY fell again last night:

The Australian dollar popped and dropped:

Gold gained again:

Oil was clubbed:

Metals screamed that the global recovery in trouble:

Miners fell:

EM stocks don’t care:

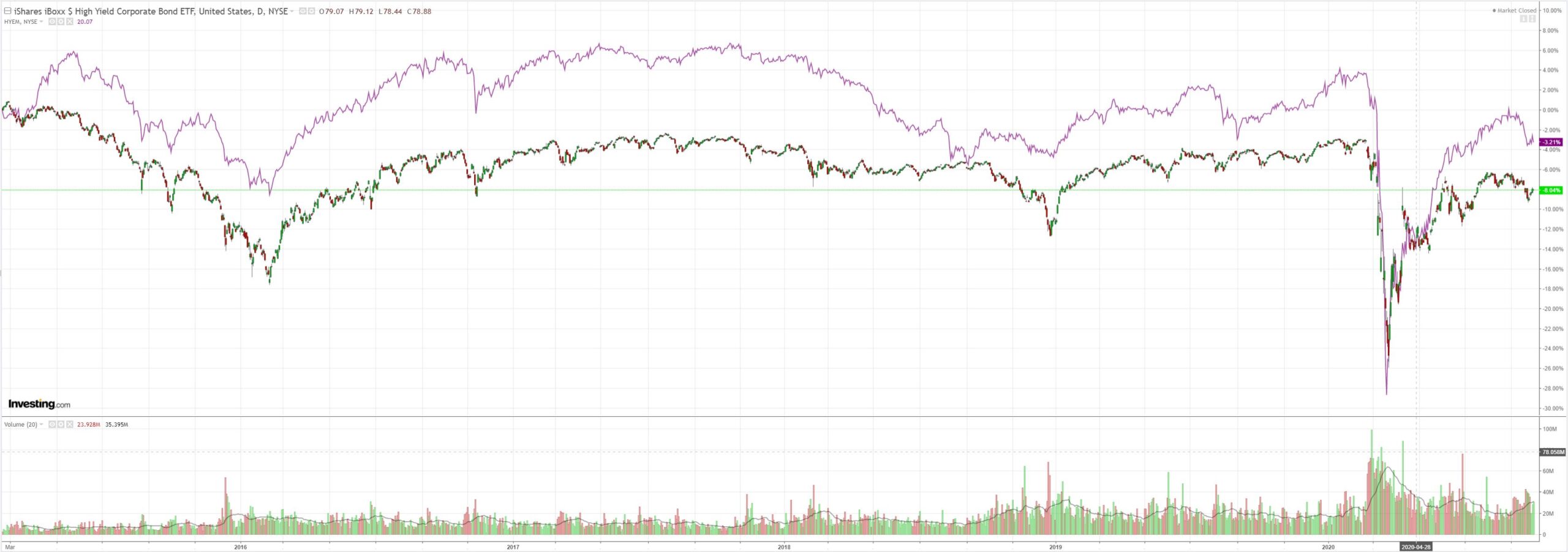

The junk siren sounded again:

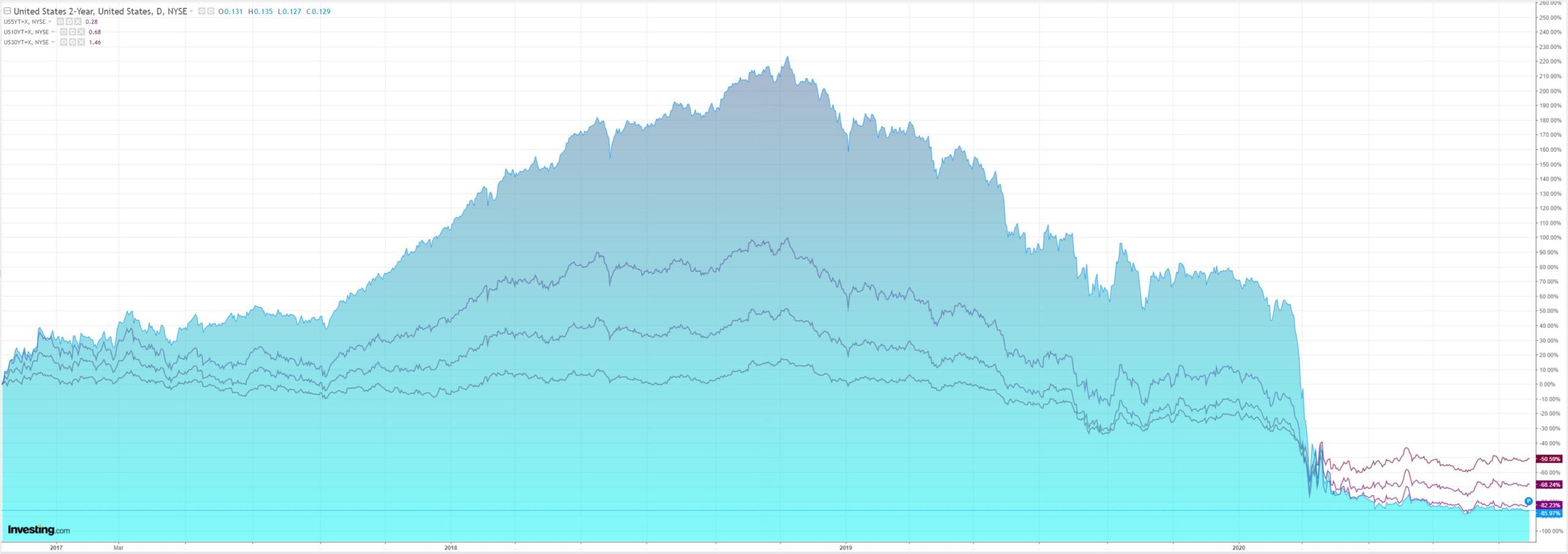

US yields eased:

Stocks crashed up:

Westpac has the wrap:

Event Wrap

US initial jobless claims slowed to 837k (vs 850k estimated, 873k prior). Continuing claims slowed from 12,747k to 11,767k. Personal income fell 2.7% in August (vs 2.5% estimated, +0.5% prior), while spending rose 1.0% (vs 0.8% est, 1.5% prior). The core PCE deflator rose 0.3% in August, as expected, but July was revised from 0.3% to 0.4%. The annual pace rose from 1.4% to 1.6% – back to March’s pace. ISM manufacturing fell from an index level of 56.0 to a still-solid 55.4 (vs 56.5 est.). Much of the slippage was due to a fall in orders and production.

U.S. House Speaker Nancy Pelosi said there are still major differences to be bridged in the negotiations over a fiscal stimulus package with Treasury Secretary Steven Mnuchin.

Event Outlook

Australia: The preliminary estimate for August retail sales was much weaker than anticipated; both Westpac and the market expect the final estimate to confirm a 4.2% fall in the month.

NZ: ANZ consumer confidence continues to be weighed down by Covid anxiety (prior: 100.2).

Euro Area: In September, the CPI is expected to partially recover August’s 0.4% fall with a 0.2% gain.

US: Employment growth is expected to slow further in September, though the monthly gain for nonfarm payrolls is still expected to be around 950k (prior: 1371k, market f/c: 868k). Having moved materially lower in recent months, the unemployment rate is expected to steady, only edging lower from 8.4% to 8.2%. Labour market slack will continue to place pressure on wages; average hourly earnings is expected to post a modest gain in September(prior: 0.4%/mth, Westpac and market f/c: 0.2%). September Uni of Michigan consumer sentiment is expected to remain broadly unchanged, having lagged activity data (prior: 78.9, market f/c: 79.0).

Negotiations over the 1.5tr-2.2tr US stimulus package did not go well. Given today is the last day to get the deal done it does not look good.

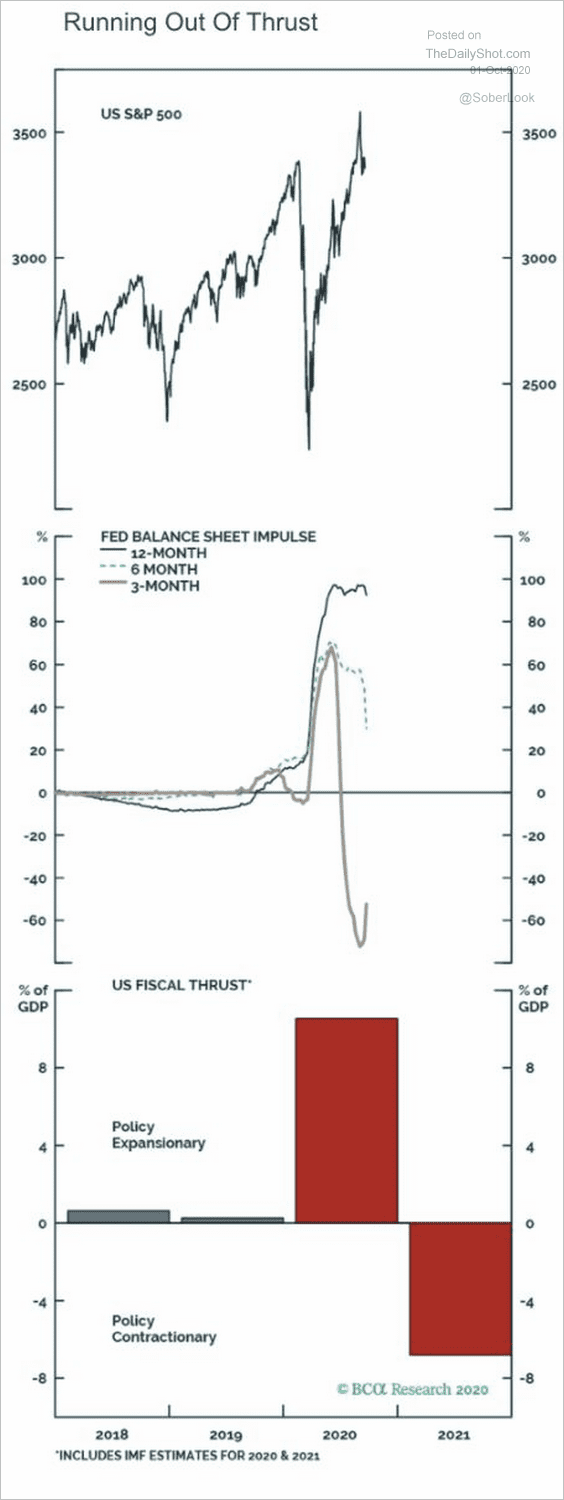

Most markets rightly saw this as a major blow to global growth. For some reason, stocks and DXY saw it as positive. I know they don’t price risk much these days but when a risk becomes reality it’s another story, or should be. Markets are “out of thrust”:

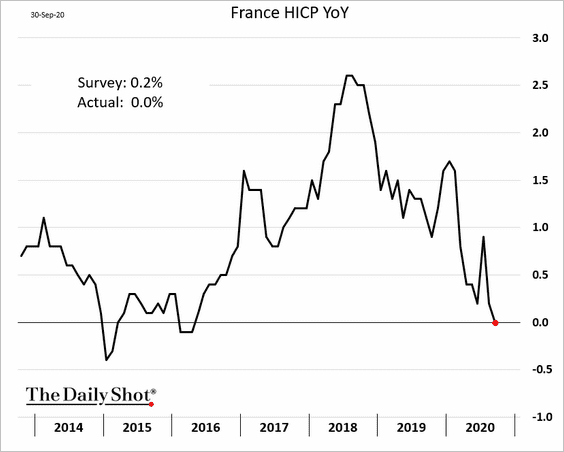

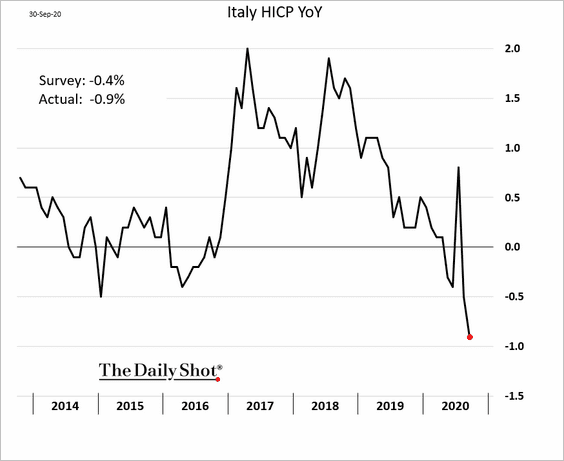

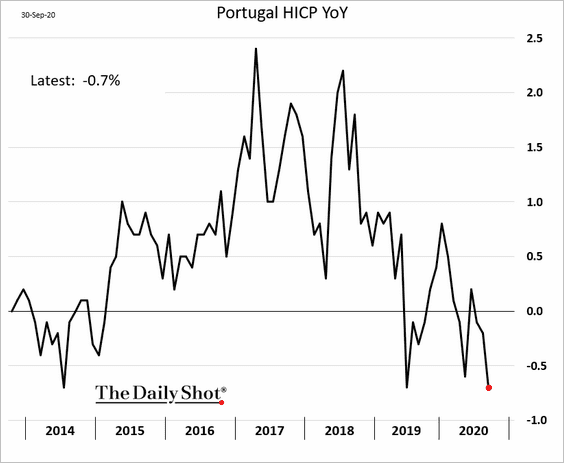

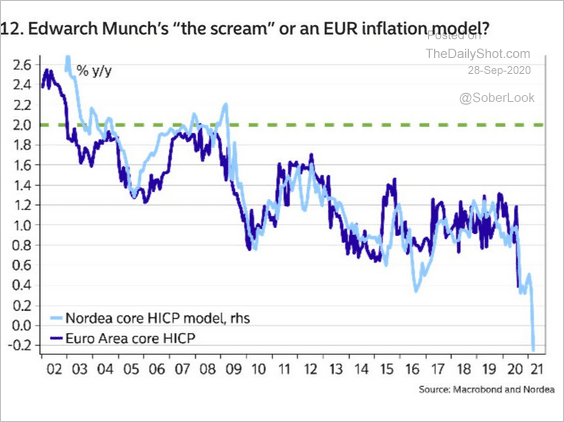

The other major development was European inflation which, unsurprisingly, is cratering as EUR runs riot:

Another major headwind to the seriously overheated falling DXY trade.

My best guess is stocks are in “crash up” mode again as technicals and quanty metrics drive the robots to bid even as the ground falls away beneath their…do they have feet? DXY is falling in sympathy.

But the outlook is deteriorating fast:

- virus on the rebound in US and Europe;

- no US fiscal deal;

- Fed tightening at the margin;

- crazy US election dead ahead;

- hard Brexit risk;

- markets massively overbalanced towards reflation.

A lower AUD still looks odds on to me in the short term.