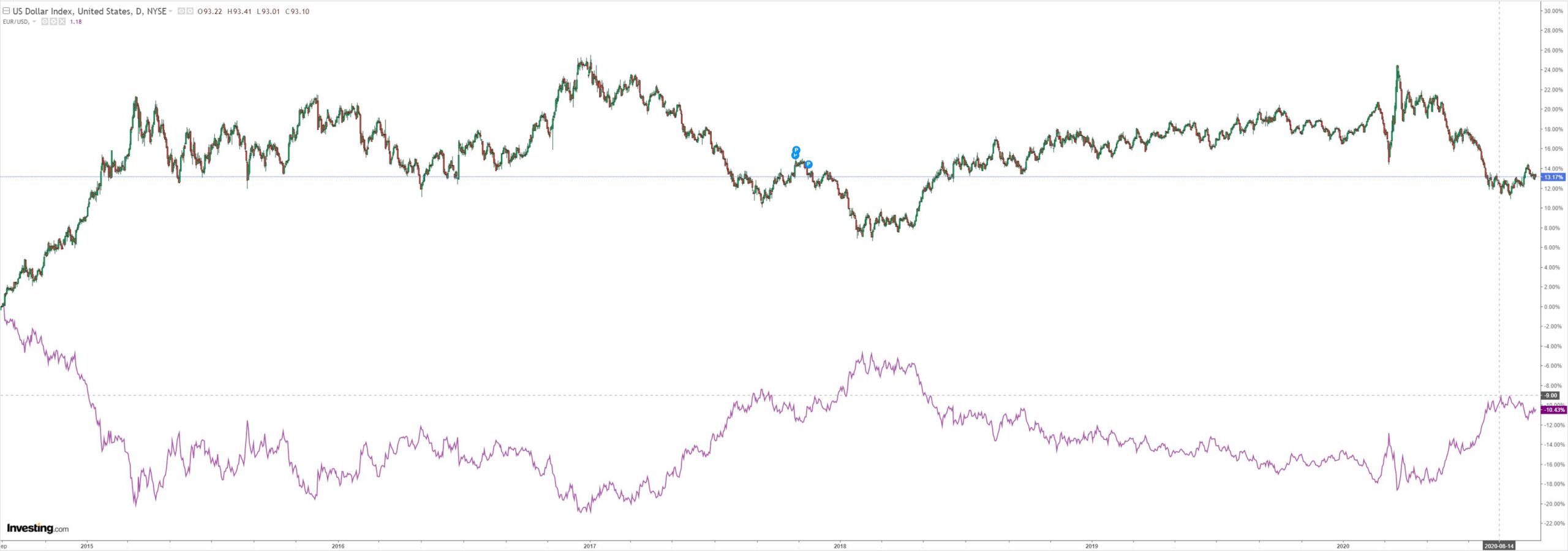

DXY was down last night:

The Australian dollar jumped:

Not gold:

Oil rose:

Metals surged:

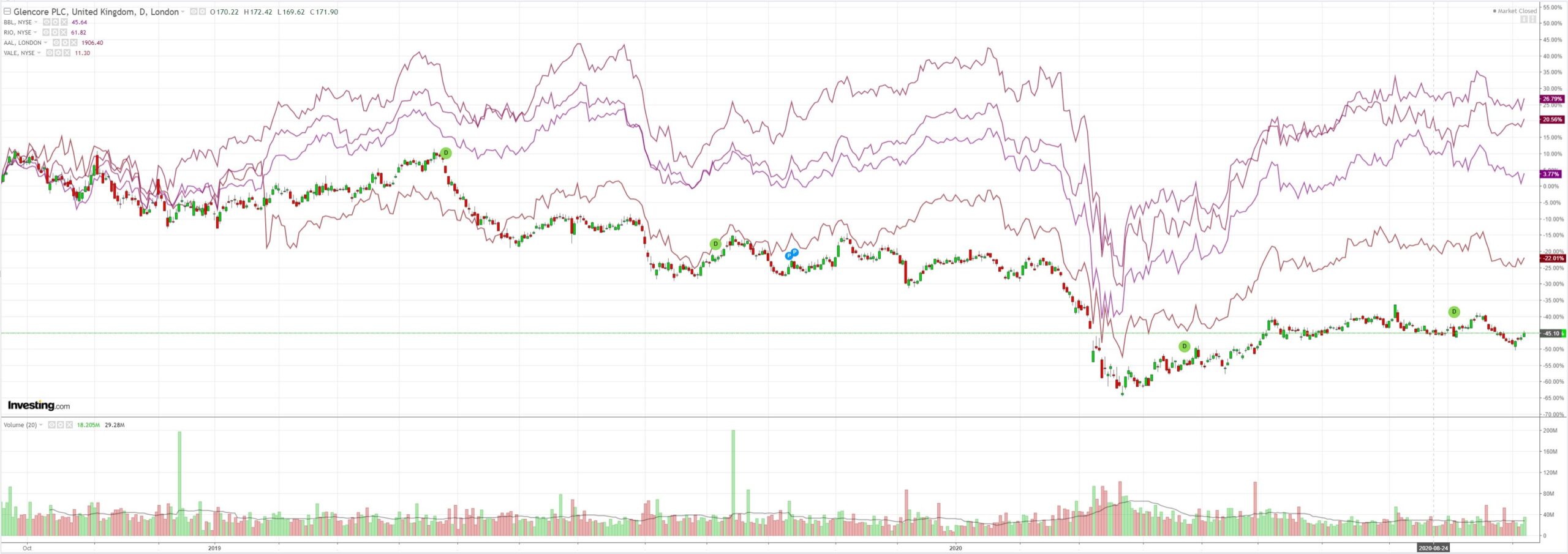

Plus miners:

And EM stocks:

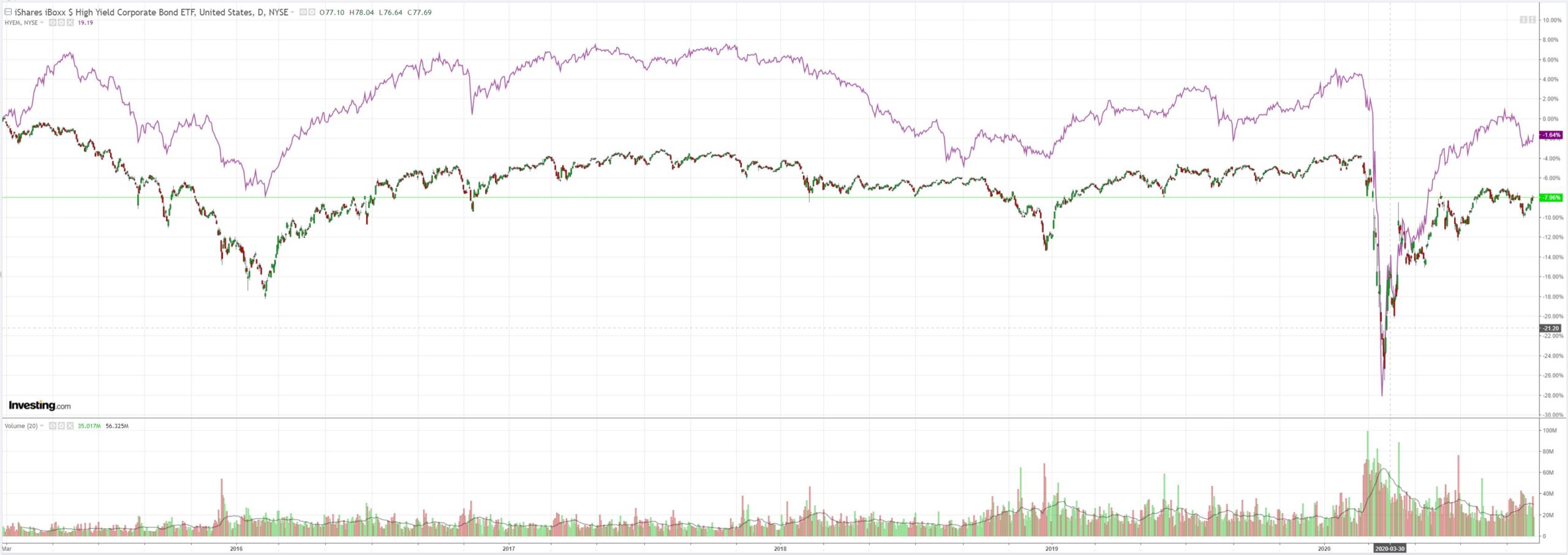

The junk siren has gone silent:

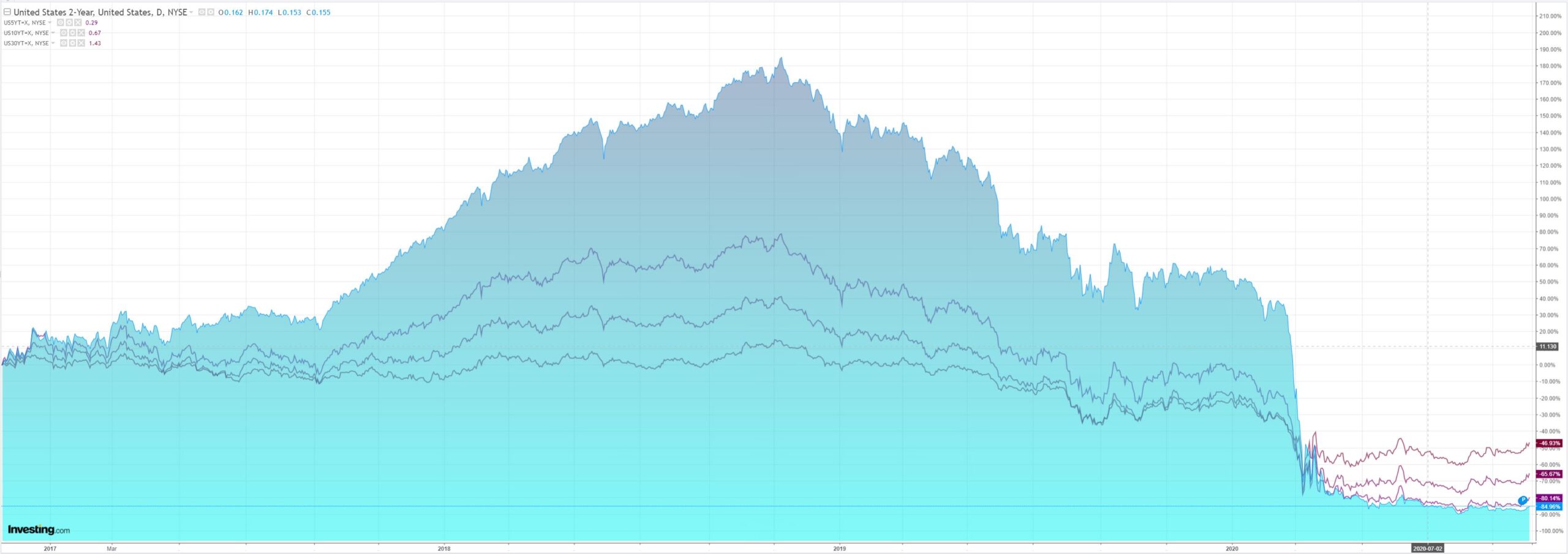

The US yield curve is steepening:

Stocks to the moon:

And so much for pricing election risk! The failure to pass a $2tr stimulus package was overwhelmed by the tweet of a drug-addled, dead duck maniac that has lost the support of his own party and country but not markets!

Move Fast, I Am Waiting To Sign! @SpeakerPelosi https://t.co/RYBeWWuPC2

— Donald J. Trump (@realDonaldTrump) October 7, 2020

The only problem? It’s the Republican senate that won’t pass the legislation. God knows what will happen when El Trumpo ends his five-day uber-steriods course. But let that pass. Buy a random tweet!

Even though:

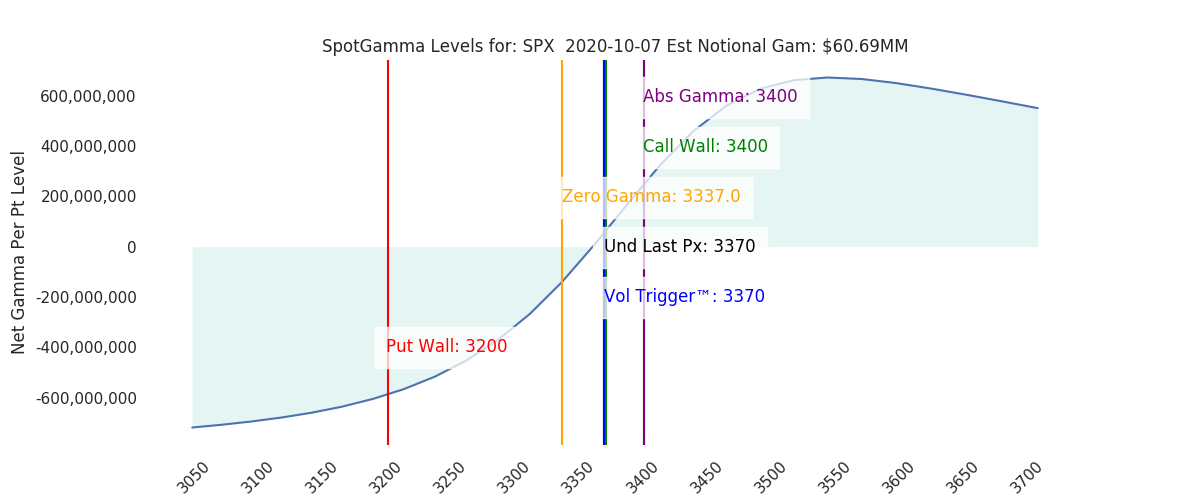

These days the equity market is reduced to daily jawboning to support key technical levels and let the robots do the rest. From SpotGamma:

It’s not your grandfather’s discounting mechanism that’s for damn sure.

Still, election risk has subsided even as stimulus has crashed. The end of a drug-addled, dead duck maniac in the White House is bullish is it not? And a clean sweep will eventually deliver more fiscal, from Goldman:

1. President Trump’s announcement that he has instructed Secretary Mnuchin to end talks with Speaker Pelosi on a COVID relief bill likely signals that the odds are very low that Congress will pass a large fiscal package before the election. While we had not expected further pre-election fiscal relief, these developments are still surprising, for two reasons. First, the President himself had pressed publicly for an agreement just a few days earlier, so this represents an abrupt shift. Second, one would expect politicians in both parties to want to continue negotiations, if only to maintain the appearance of progress as the election approaches. While President Trump’s decision to call off further negotiations might be an attempt to put political pressure on Speaker Pelosi to compromise, this seems unlikely to produce an agreement on a large fiscal package.

2. The focus now looks likely to turn to piecemeal legislation. Last week, Speaker Pelosi indicated she would be willing to put a standalone bill providing additional relief to airlines on the House floor for a vote. In addition, on Tuesday (Oct. 6), President Trump endorsed standalone legislation to provide more funding for the Paycheck Protection Program (PPP) and another round of stimulus payments ($1,200 per individual). However, the President already supported these policies, so while this represents a shift in legislative strategy, it does not represent a change in position.

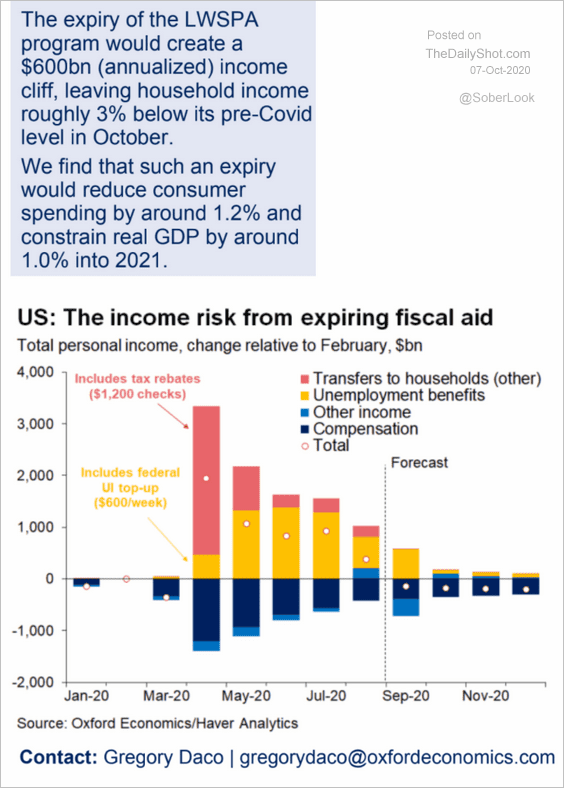

3. A piecemeal approach might allow for only a very limited amount of fiscal relief. Since the White House and Democratic leaders appear to support standalone airline relief legislation, enactment of another $25bn in airline aid looks increasingly likely. Passage of standalone legislation authorizing another round of PPP loans for hard-hit businesses is possible but not likely, in our view. A standalone PPP bill is possible as members of both parties support it, but it is unlikely because lawmakers in both parties would likely want to attach additional measures to such a bill, like a renewal of the expired extra $600/week unemployment benefit, or aid to schools. If so, a simple standalone bill could quickly become a renewed negotiation over a broader fiscal package. A standalone bill to authorize another round of stimulus payments to individuals is even less likely, as neither party has made this a priority even though both parties appear to support such payments as part of a broader package.

4. Broader fiscal relief looks like a post-election issue. If the election results in a status quo election outcome (i.e., Republican White House and Senate, Democratic House) then Congress might pass some fiscal relief measures in a lame-duck session of Congress before the end of the year, including further PPP funds, a partial extension of the extra unemployment benefit, and money for schools. By contrast, if Democrats win control of the White House and Senate, we would expect Congress to enact a much larger fiscal package, as we recently described, but we would not expect it to pass until early 2021.

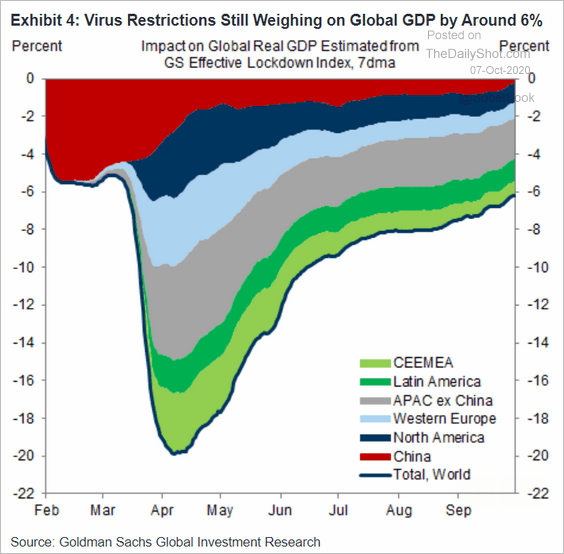

But also large, very equity market negative tax hikes. Oh well! Global growth is slowly returning:

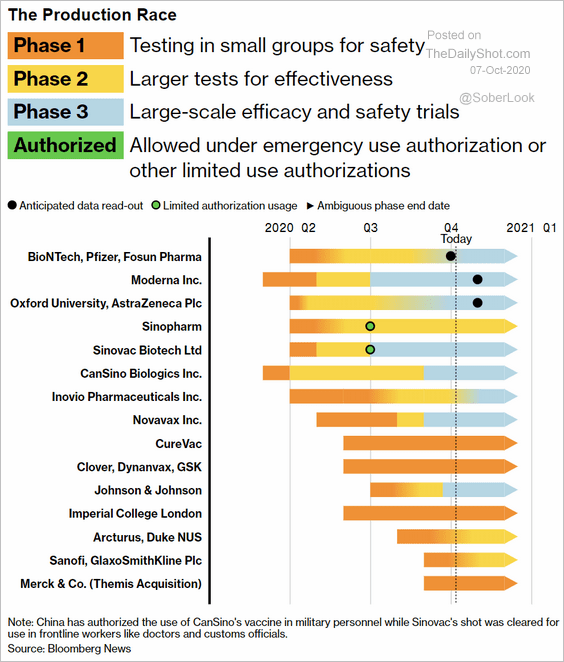

And there is is this, as troubled as it will be:

And Fed minutes may have tantalised markets:

While the economic outlook had brightened, market participants continued to see significant risks ahead. Some noted concerns about elevated asset valuations in certain sectors. Many also cited geopolitical events as heightening uncertainty. In addition, most forecasters were assuming that an additional pandemic-related fiscal package would be approved this year, and noted that, absent a new package, growth could decelerate at a faster-than-expected pace in the fourth quarter. In light of these and other risks, as well as the ongoing pandemic, market participants continued to suggest that the supportive policy environment and the backstops to market functioning remained important stabilizers.

…Participants continued to see the uncertainty surrounding the economic outlook as very elevated, with the path of the economy highly dependent on the course of the virus; on how individuals, businesses, and public officials responded to it; and on the effectiveness of public health measures to address it. Participants cited several downside risks that could threaten the recovery. While the risk of another broad economic shutdown was seen as having receded, participants remained concerned about the possibility of additional virus outbreaks that could undermine the recovery. Such scenarios could result in increases in bankruptcies and defaults, put stress on the financial system, and lead to disruptions in the flow of credit to households and businesses.

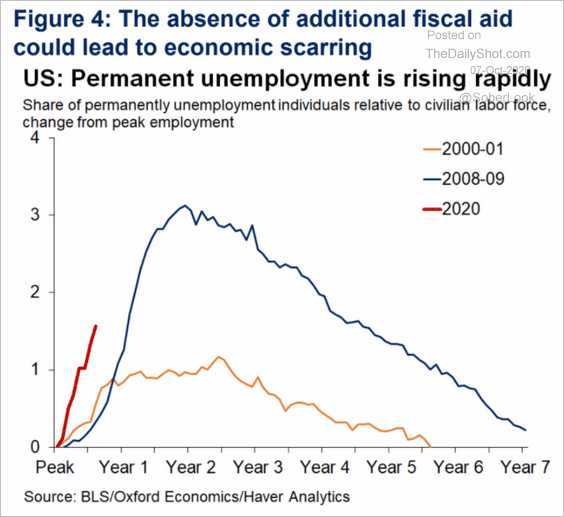

Most participants raised the concern that fiscal support so far for households, businesses, and state and local governments might not provide sufficient relief to these sectors. A couple of participants saw an upside risk that further fiscal stimulus could be larger than anticipated, though it might come later than had been expected. Several participants raised concerns regarding the longer-run effects of the pandemic, including how it could lead to a restructuring in some sectors of the economy that could slow employment growth or could accelerate technological disruption that was likely limiting the pricing power of firms.

So, now that those assumptions have proven false the Fed will ride to the rescue?

And so, we solider on into this extreme-risk dystopian future pricing for risk-free utopia.

The Australian dollar dragged along for the ride.