European officials commented on major issues in advance of the EC Summit on 15-16 October. ECB members reiterated that it was prepared to ease further if needed but also that it looked for the EC to ratify the Recovery Fund soon. The EC’s Hahn outlined the likely initial issuance of EU bonds in late October. Germany’s Scholz spoke of moves in the EU towards fiscal union.

BoE Governor Bailey reiterated that there was no intention of an imminent imposition of NIRP. The announcement of letters being issued to financial institutions for consultation is intended to ensure the practicalities of NIRP are known and in place.

The UK announced a three-tiered alert system for Covid. The Liverpool area and much of NE and NW England were placed in the highest risk category, requiring the closure of pubs/bars/restaurants, while schools and work places will remain open. Most of England remains in “medium” alert, with London and many other areas remaining on designation watch.

Event Outlook

New Zealand: September’s card spending figures are expected to point to recovery as restrictions ease. Westpac expects a jump of 9% driven by hospitality spending following a 7% fall last month. We also see a reversal in fruit and vegetable prices, the food price index down 1.2% in September after a gain of 0.7%. The REINZ house price index has outperformed in recent months. Strength in sales and prices is expected to persist.

China: The global economic rebound is expected to support a further widening of the trade balance in Sep (prior: 58.93USD, 60USD).

Eurozone: The ZEW survey of expectations rose to a 16yr high of 73.9 on recovery hopes. COVID’s resurgence is now expected to drive a reversal.

Germany: Sep’s CPI will likely see weak consumption and the VAT sales-tax cut continue to dampen prices (prior and market f/c: -0.2%).

UK: A modest deterioration in the ILO unemployment rate to 4.3% is anticipated in Aug. As the government’s furlough scheme winds down, further weakness will be seen.

US: The NFIB small business optimism survey could see a return to pre-crisis levels in Aug as job-creation plans and sales improve (prior: 100.2, market f/c: 101.2). The CPI is expected to moderate to 0.2% after months of pandemic-impacted gains as the rent and services components remain weak.

I’m not going to try to give you a macro narrative for stock prices. They will do what they do. Forex is paying attention to a range of headwinds for risk as the US recovery struggles greatly into no more fiscal stimulus and a resurgent virus:

Advertisement

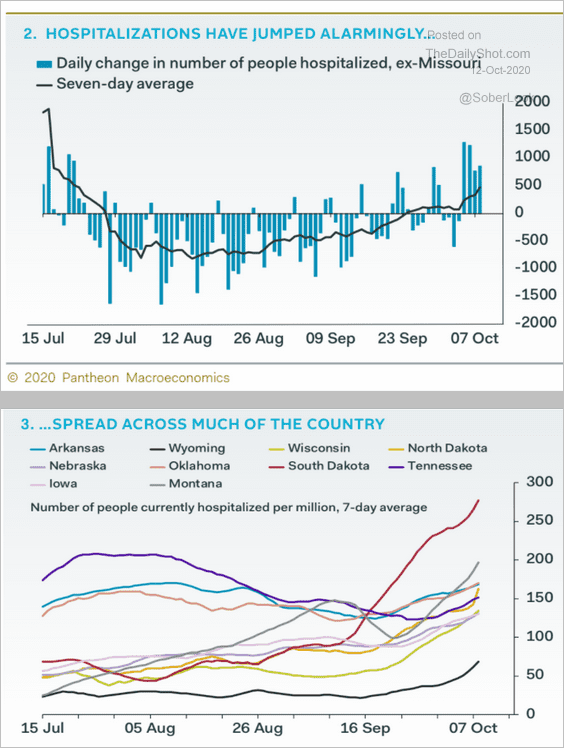

A resurgent virus is about to make it considerably worse:

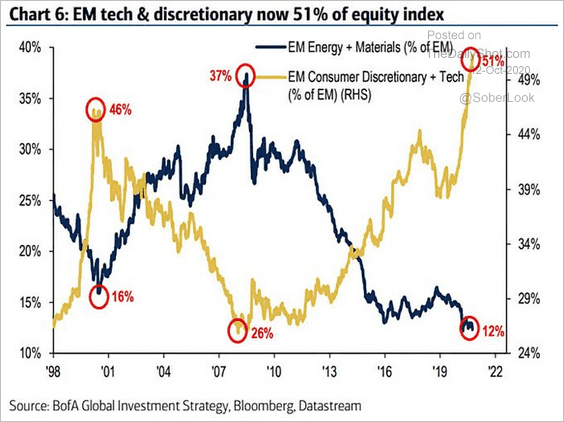

Tech is massively overpriced:

Advertisement

But then, perhaps, the weakening economic outlook was just what the robots needed to return to buying themselves:

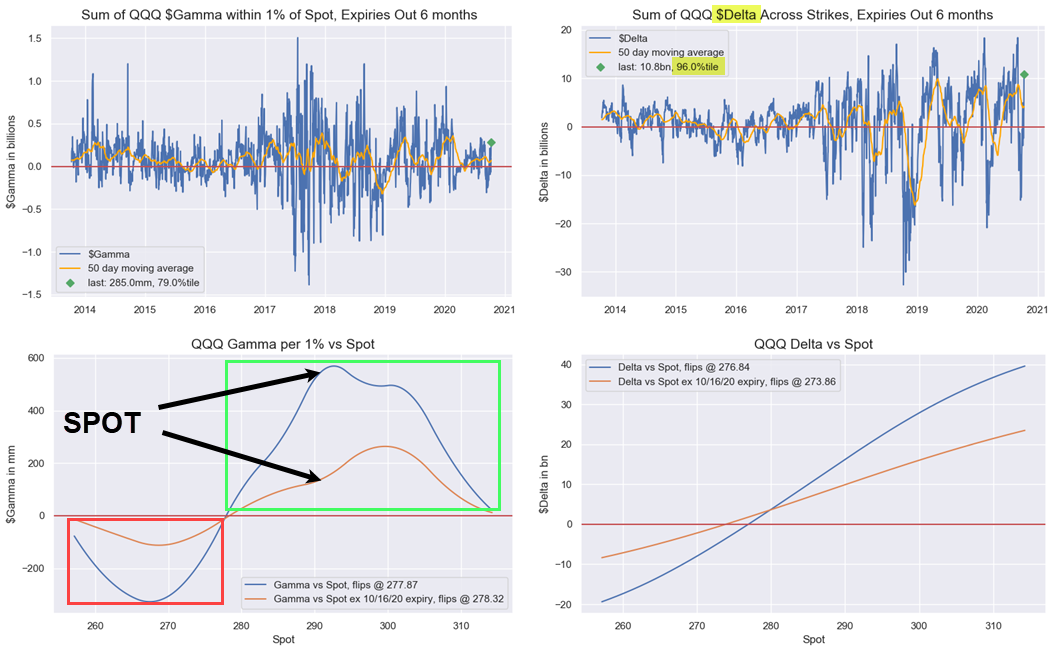

Nomura’s Charlie McElligott wrote in his morning note when looking at today’s exponential “panic grab” price-action in Equities futures, “the buy flows are being driven by a legacy dynamic in SINGLE-STOCK VOL which you’re now well-familiar with, where we see massive upside call strikes suddenly back ‘in-play” on the meltup this week into their Friday’s expiration in some of those mega-cap Tech stocks (AMZN in particularly, but ADBE and NFLX as well) that traded back in August, forcing what looks to be “short Gamma” -type buying / hedging this morning from the Dealer short them in order to stay neutral.”

Said otherwise, the same “gamma squeeze” dynamic we observed in mid/late August when Masa Son’s SoftBank ended up buying billions in call spreads, sparking a meltup in tech names is back and just like in August, liquidity is dismal which likely means that SoftBank is back for round three (after a failed attempt to squeeze the Nasdaq higher two weeks ago).

To this point, JPMorgan strategist Shawn Quigg wrote last week that the market’s low liquidity environment “lays the groundwork for dealer positioning (i.e., gamma imbalances) that can further exacerbate existing market trends, and volatility dynamics (e.g., prices up/volatility down to prices up/volatility up). As such, market participants now closely follow large dealer gamma imbalances ahead of potentially impactful macro events, primarily in options on the S&P 500, to gauge potentially trend accentuating dealer flows.”

Alternatively, if the “Nasdaq whale” so wishes dealers can again be squeezed by a rerun of the August meltup, something which we are seeing in real time today with the help of a handful of exceptionally large trades in thin markets which as JPM admits, “increase the potential for exacerbated stock moves as dealers hedge exposure.” That said, at least back in August NQ futs were well in the green, so this time we also have the short squeeze of futures traders to consider as risk explodes higher amid the concurrent gamma squeeze.

All I can say is that the Australian dollar is lagging the renewed bubble bid and for good reason.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.