DXY was up last night:

The Australian dollar was roughly flat:

Gold fell:

Oil rose:

Metals fell:

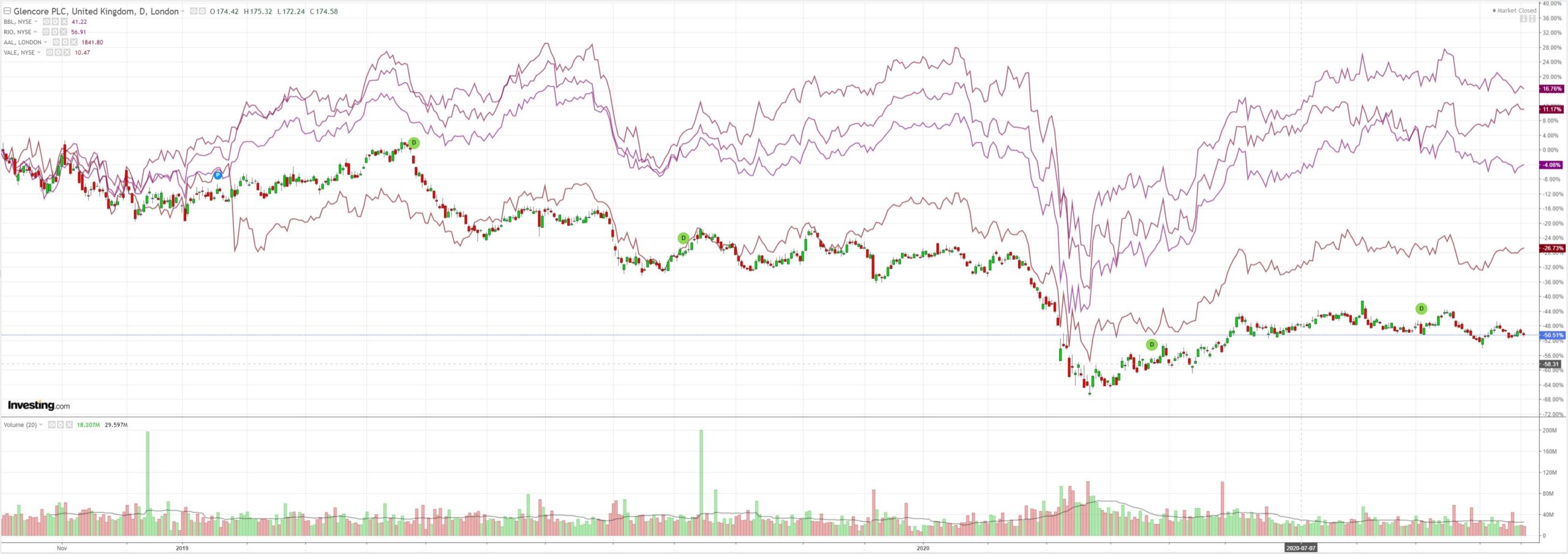

Miners were mixed:

EMs stocks stalled:

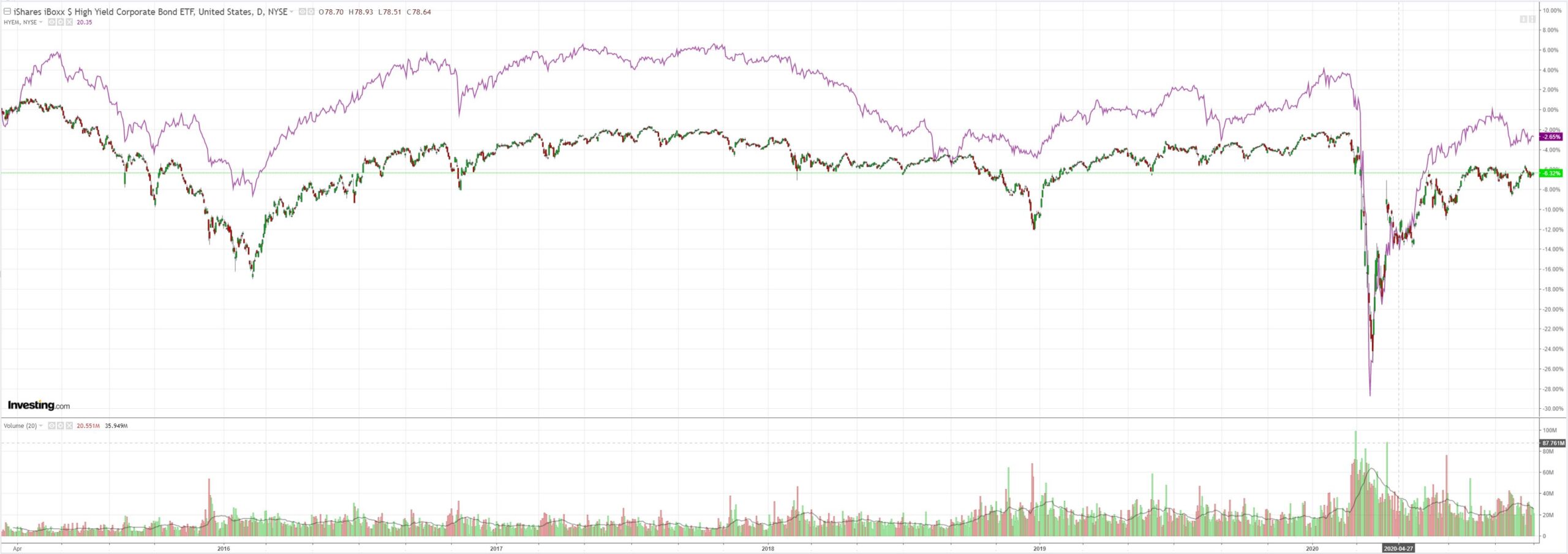

Junk too:

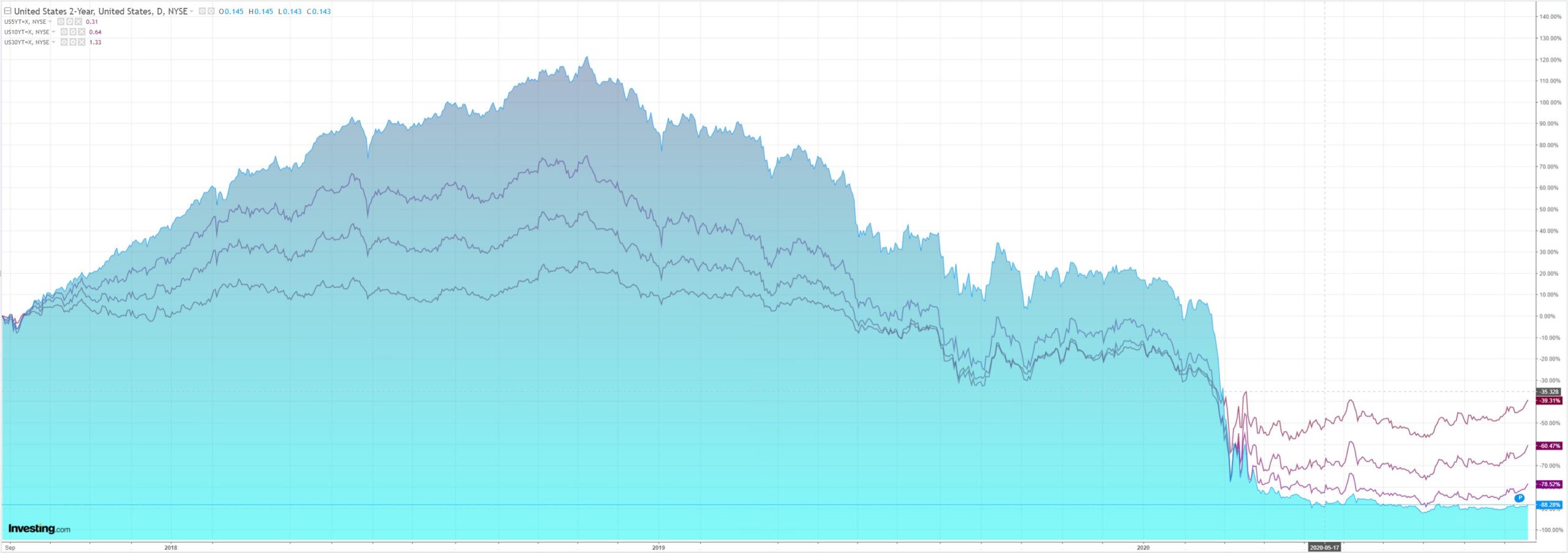

US yields backed up some more:

Stocks firmed:

Wesptac has the wrap:

Event Wrap

US September home sales surged 9.4% to an annualised 6.54m homes (est. 6.30m) on the back of record low mortgage rates and a surge in demand for single family homes. Weekly initial jobless claims slipped to 787k (est. 870k) and continuing claims fell from 9.397m to 8.373m (est. 9.625m) – the lowest level since March when claims began to surge. The Sep. Kansas Fed survey rose to 13 (est. unchanged at 11).

Eurozone Oct. consumer confidence was close to expectations at -15.5 (est. -15, prior -13.9). German Oct. GfK consumer confidence pulled back in line with expectations to -3.1 (est. -3.0, prior -1.7). French Oct. business survey data held firm at 90 (est. unch. at 92) despite the rise in COVID restrictions.

UK Oct. CBI business trends was firmer than expected at -34 (est. -50, prior -48), with optimism lifting to 0 (est. -17, prior -1). Though acknowledging the better outlook, CBI officials voiced concern over rising COVID restrictions and stuttering EU/UK trade talks.

Event Outlook

NZ: Westpac expects a 0.9% rise in the CPI in Q3 as a result of higher fuel prices and seasonal influences. This would see annual inflation lift slightly to 1.6%yr.

Japan: TheSep CPI will be impacted by the government travel discount roll-off and weak oil prices (prior: 0.2%yr, market f/c: 0%yr). Travel restrictions and business closures have kept both the manufacturing and service PMIs in contractionary territory at 47.7 and 46.9 respectively, though ahead a recovery in South-East Asia should support demand.

Eurozone: The Markit manufacturing and service PMIs for the Eurozone and Germany will be released, with initial signs of a virus resurgence and government restrictions to weigh on business sentiment all around.

UK: British consumers remain cautious amid a second wave of infections. The recovery in retail sales is expected to lose momentum in September and to the end of the year (prior: 0.8%, market f/c: 0.2%). Manufacturing and service activity is also set to decline in October, with services to bear the brunt of tighter restrictions (manufacturing – prior: 54.1, market f/c: 53.1 – services – prior: 56.1, market f/c: 53.9).

US: The ongoing spread of COVID has had a minimal impact on the Markit PMIs which are expected to remain expansionary in October (manufacturing – prior: 53.2, market f/c: 53.5 – services – prior and market f/c: 54.6).

The final Presidential debate from Nashville, Tennessee will begin at 12:00 AEST/21:00 EST.

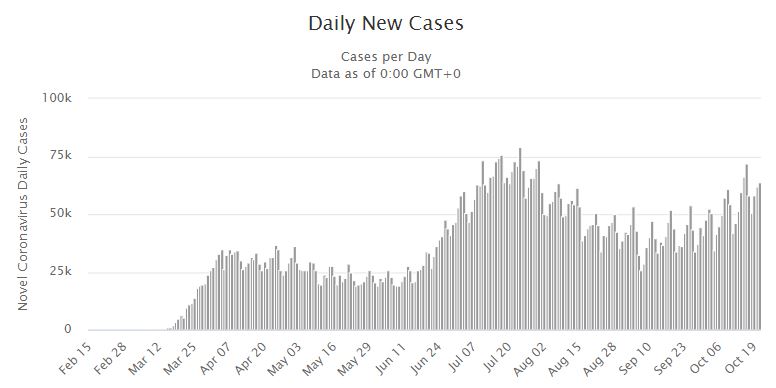

There are some days when one has to question the sanity of the market. US stimulus theater is ongoing. There is none coming. At the same time, what is coming is the virus, and lot’s of it:

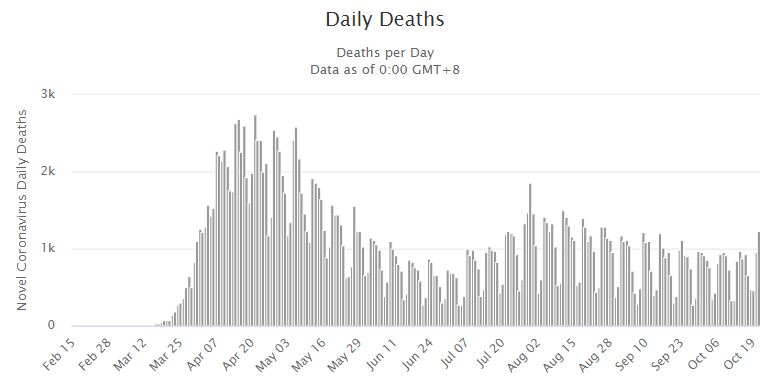

And the death march has roared back right on cue:

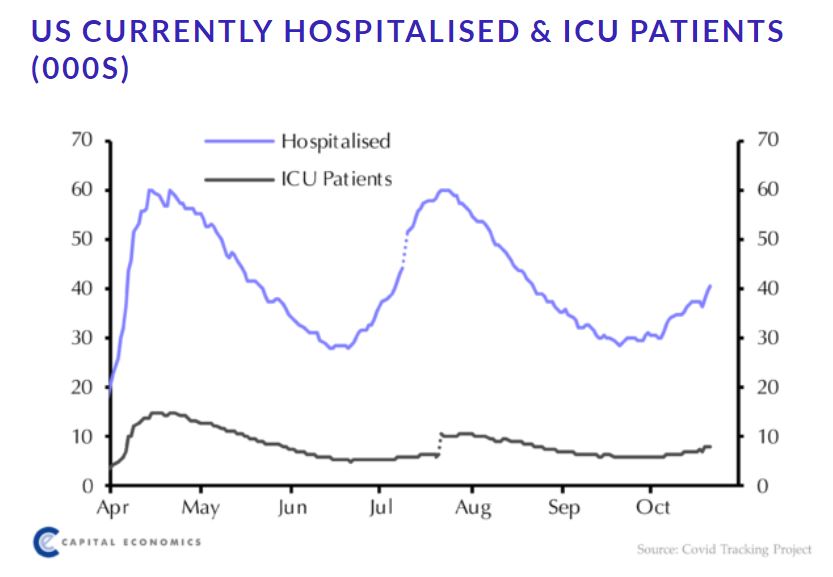

Led by spiking hospitalisations that are going to get much worse:

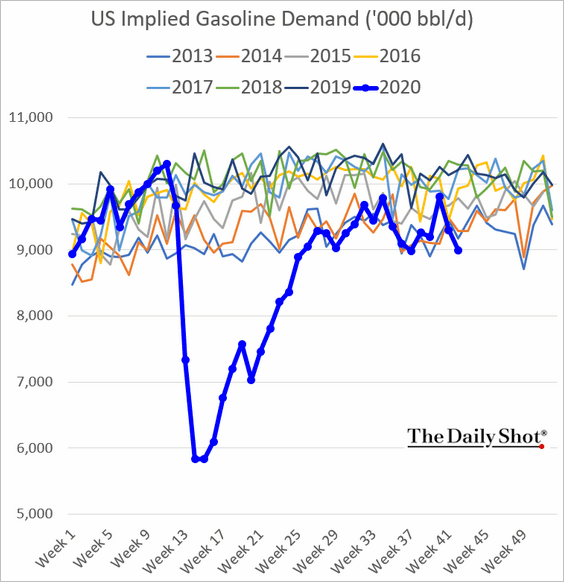

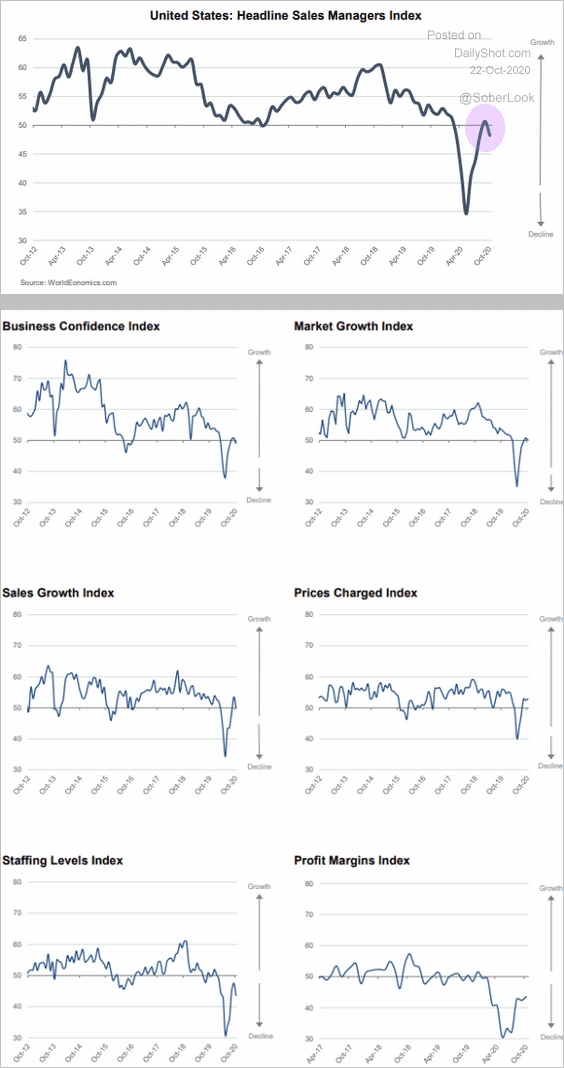

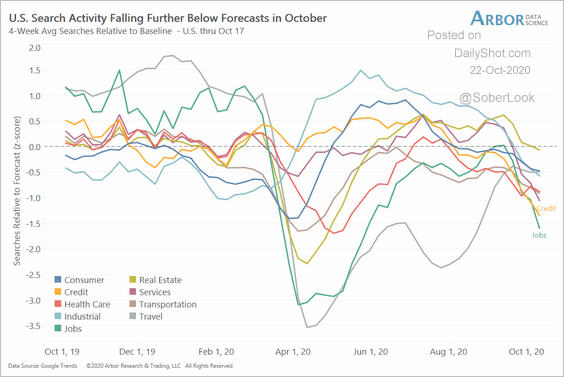

The US economy has begun to roll over and it will get worse as the virus runs riot all over again in winter and the private sector shuts:

Even as the economy loses fiscal stimulus for the next five months.

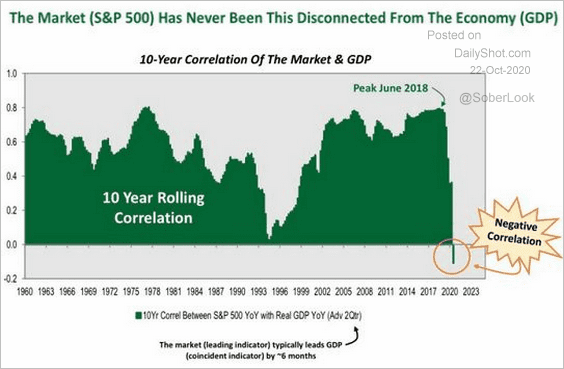

Yet we have the bond market pricing in a pick-up in inflation based upon an election we haven’t had leading to a bid for banks that will be forced to pick up the tab and this:

I’m all for discounting the future but sometimes you’ve just got look out the window at the people keeling over in the street.

There has to be a risk of a second-round rude awakening for markets.