DXY is down:

Australian dollar up:

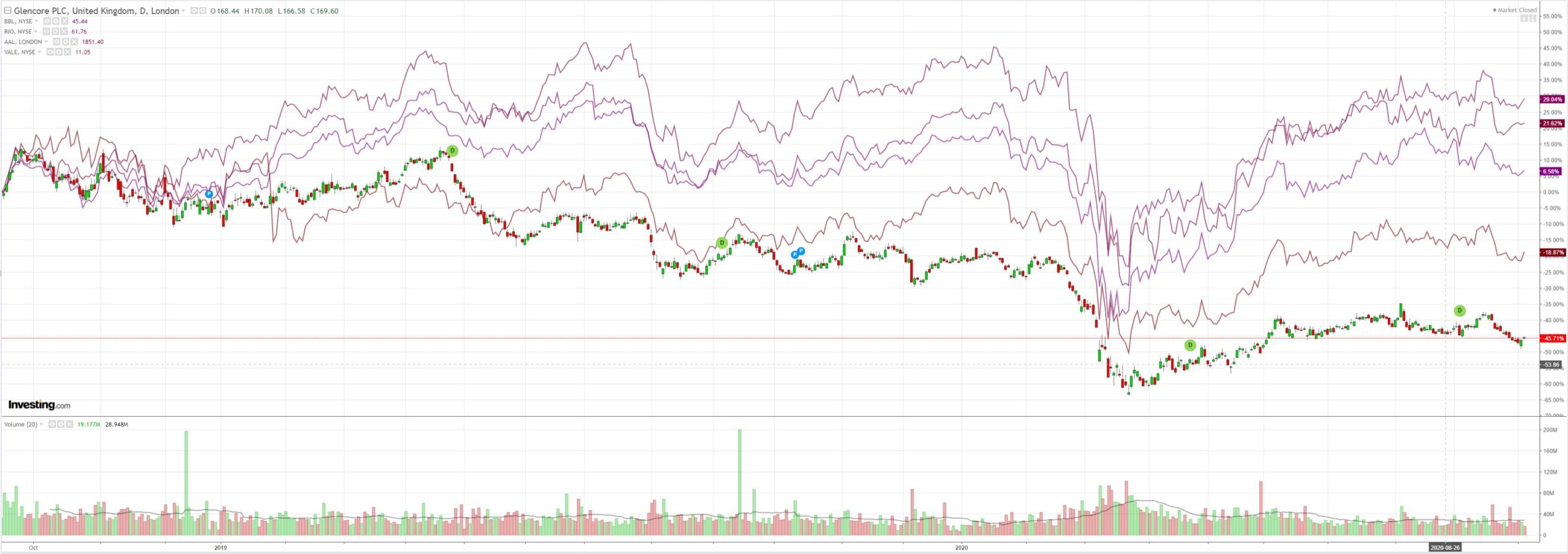

And all commodities plus miners:

Plus EM stocks:

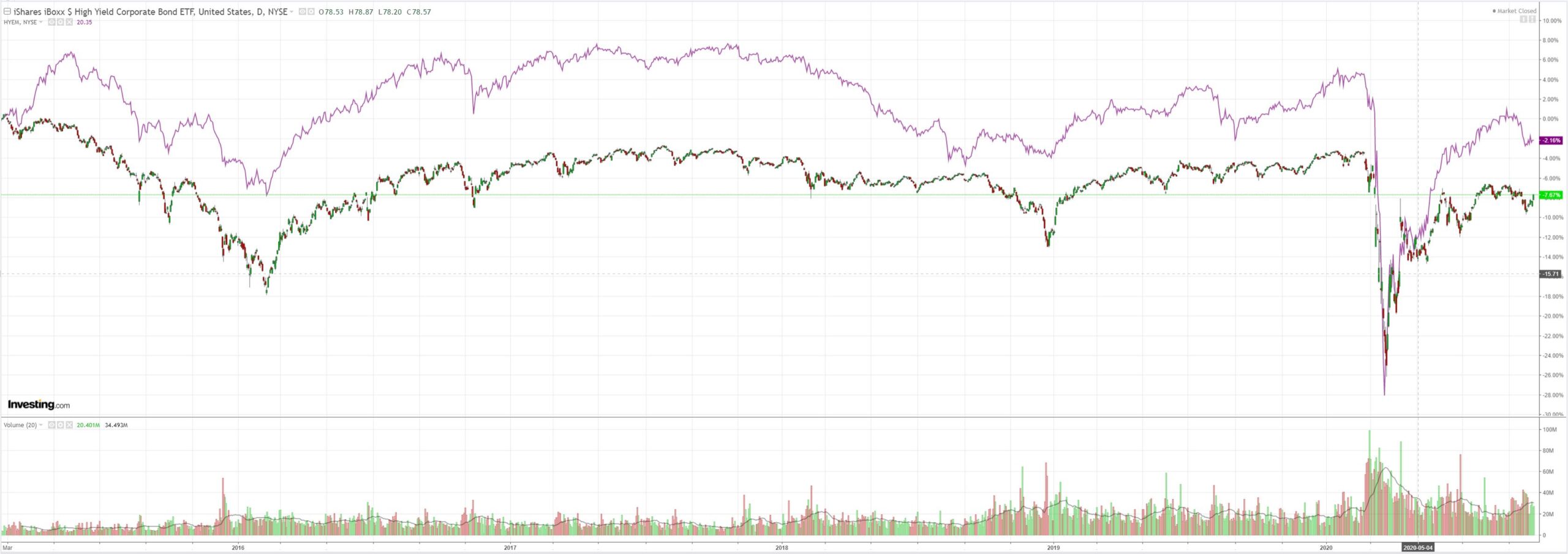

Junk is happy again but not so much EM:

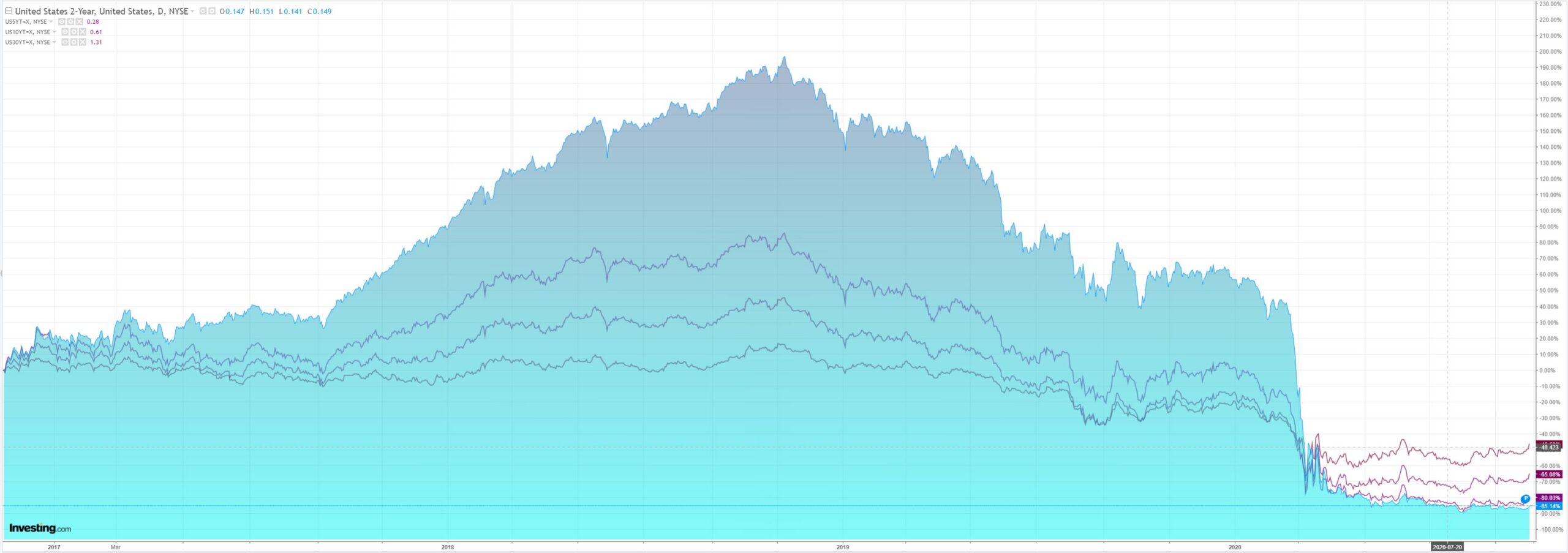

US yields launched:

Along with stockmania:

Westpac has the data wrap:

Event Wrap

US Sept. Service ISM beat expectations with a rebound to 57.8 (est. 56.2, Aug. 56.9) led by solid activity (63.0, from 56.8) and new orders (61.5 prior 56.8) as well as solid employment gains back above 50 to its highest level since February at 51.8 (prior 47.8). Although export and import orders pulled back, the overall profile of the report was solid despite some notable differences within the service sector.

US Markit final Service PMI was unchanged from its flash reading of 54.6.

Eurozone final Markit Service PMI lifted to 48.0 from its flash reading of 47.6 allowing the composite reading to edge to 50.4 (flash 50.1). Although Germany posted a minor expansion (50.6, flash 49.1), weakness due to COVID outbreaks was noted across the region, particularly in Spain (service reading fell to 42.4 from 47.7 in August).

UK’s final Markit Service PMI firmed to 56.1 from its flash reading of 55.1 as the service sector continued to defy negative commentary and the end of Govt. dining support.

Event Outlook

Australia: The August trade balance is expected by Westpac and the market to widen to $5.0bn as the July spike in imports reverses.

The RBA is expected to remain on hold this month. Westpac expects further easing in November.

The Federal Budget will be released at 7:30pm AEST. A high degree of support for the economy is anticipated – see our preview for all the detail.

New Zealand: The QSBO general business situation index is expected to rebound in Q3 (prior: -58.8).

US: The largest trade deficit since July 2008 is expected to widen further in August (prior: -63.6bn, market f/c: -66.1).

JOLTS job openings will continue to be supported by business recovery (prior: 6618, market f/c: 6500).FOMC’s Chair Powell will address the NABE Conference in Chicago at 01:40 AEST. The FOMC’s Harker (02:45AEST) and Bostic (05:00 AEST) will also speak.

Yesterday’s price action went in the diametrically opposite direction to sense. The drive is the new fake it ’til you make dynamic in US politics. Following Trump’s half-dead weekend exhortation to get a stimulus deal done, we had meetings all day between Steve Mnuchin and Nancy Pelosi on the next round with no substantial progress.

On the other hand, the US senate has been shut down and its leader, Mitch McConnell, appears to remain completely in opposition to the stimulus. He is focussed entirely upon getting up his favoured candidate for SCOTUS.

From a political standpoint, why wouldn’t he be? Presumably, internal Republican polling is saying the same thing as every other poll: that Trump’s goose is cooked to the point of burned. As the “blue wave” rises, this is a Republican senate’s last chance to give the Democrats a kick in the teeth before two years in the wilderness, at least. McConnell hates Trump and always has. Plus, they need to get SCOTUS up before they walk.

Of course, I may be wrong but if one backs self-interest in these things then a Republican senate likely won’t pass whatever the White House and Dems agree to.

The only other thought I have is that markets are so convinced now of the “blue wave” that the fear of hung election has receded and the rest of it doesn’t matter. But that comes with nasty triple whammy headwinds for equities of corporate and capital gains tax hikes, as well as doubled minimum wages so how can that be?

Either way, Fakeflation is having none of it. It’s all good on the stimulus front. It’s all good on election front. It’s all good on every front.

Risk is the one thing that isn’t discounted for equities and the Australian dollar.