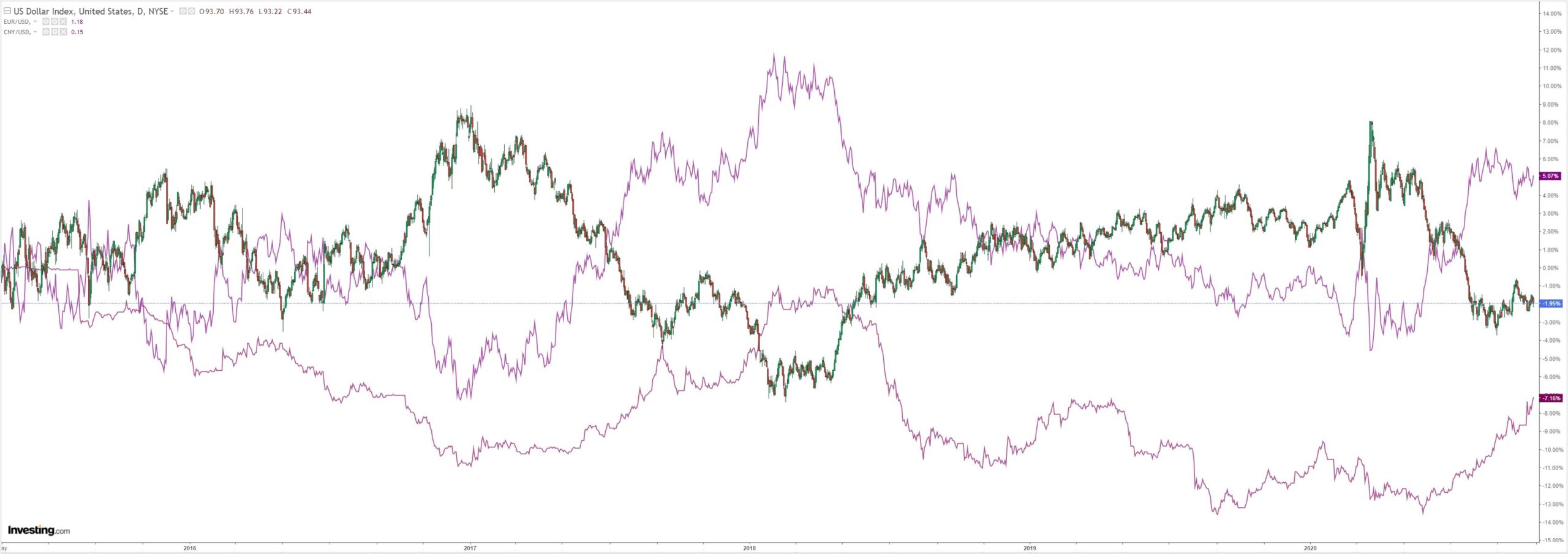

DXY was down last night as CNY and EUR rallied:

Even so, Australian dollar copped it ended at new closing lows for the move:

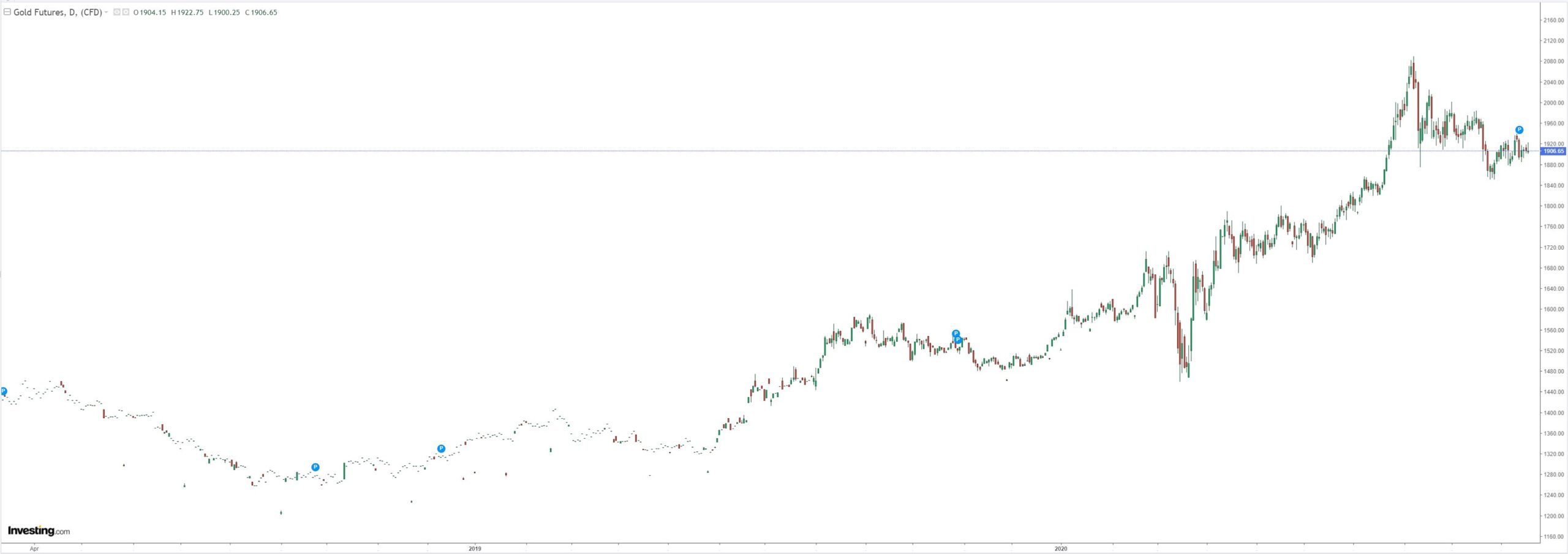

Gold was stable:

Oil too:

Metals did a bit better:

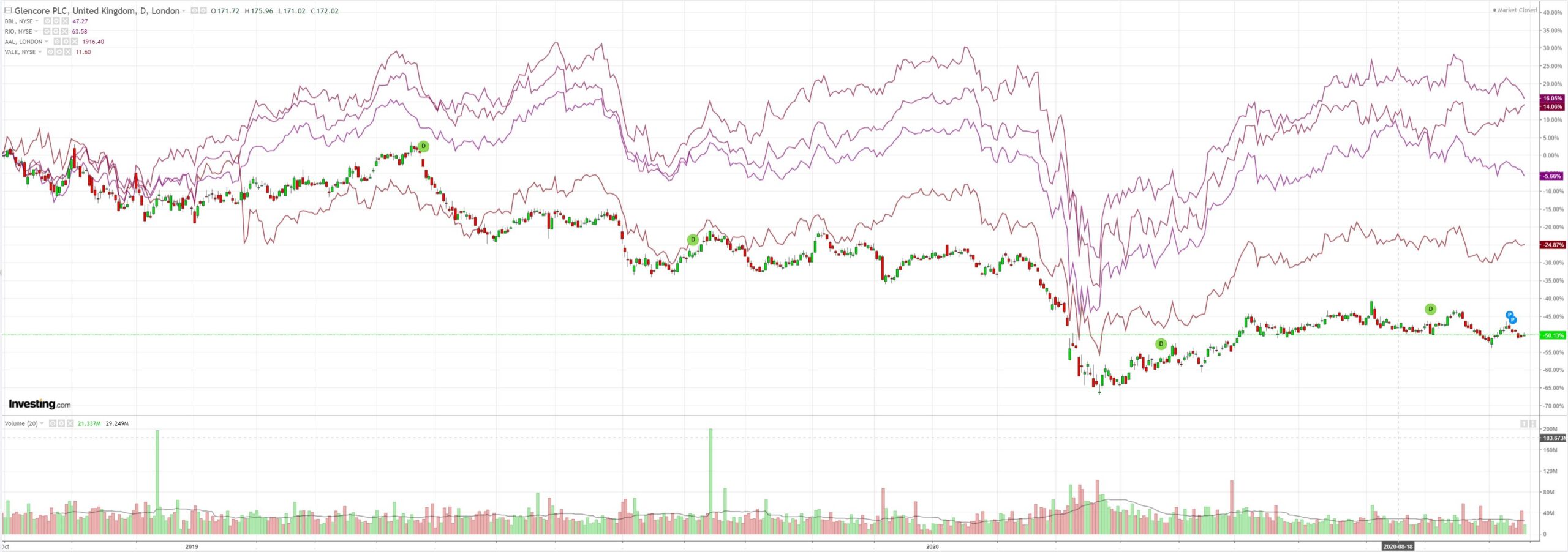

Miners did considerably worse:

EM stocks are near the highs:

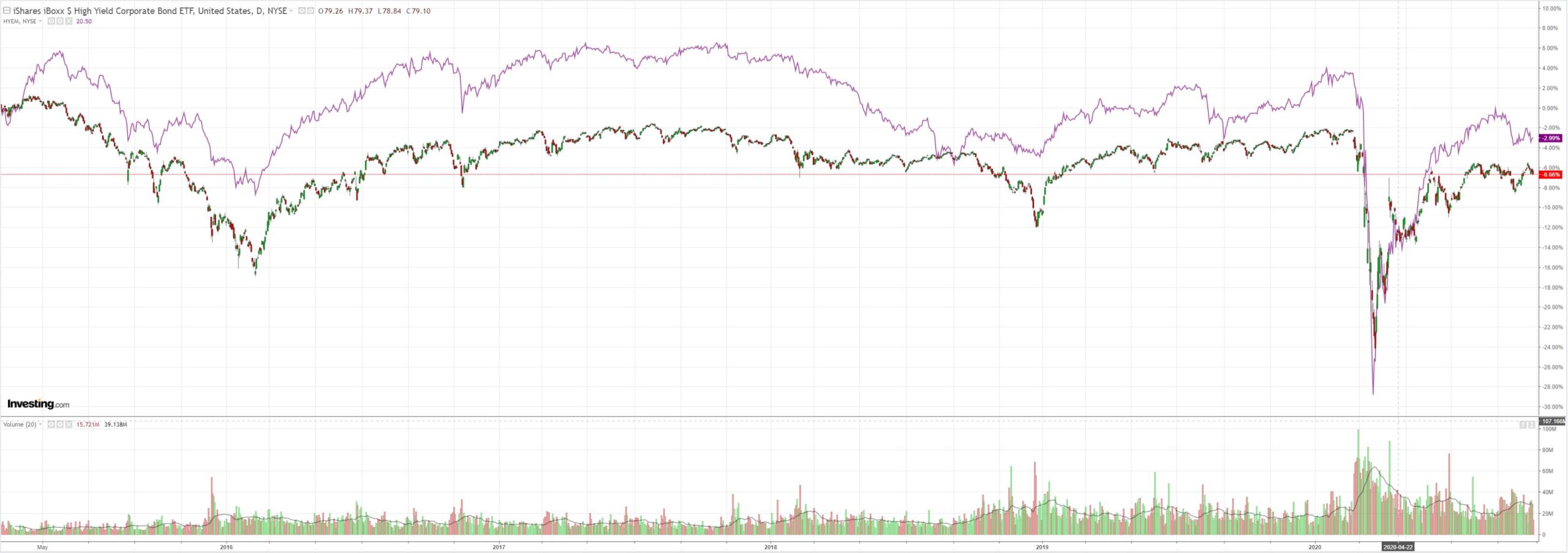

Junk bifurcated:

The US curve is still steepening:

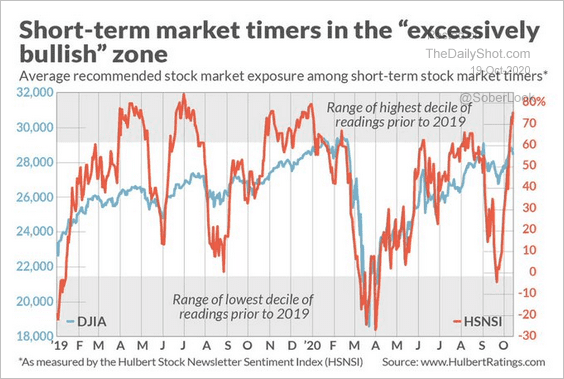

As stocks took a good hit. That’s an unfriendly looking double-top pattern that is forming:

It was the same old story. The market fakeflated into fantasy hopes of more US stimulus before it all fell apart again because it is a fantasy. Go figure. Westpac has the data wrap:

Event Wrap

US NAHB homebuilder confidence survey for September rose to another record high of 85 (est. unchanged at 83), but repeated concerns about input shortages (such as lumber, other key building materials and labour).

The ECB’s Holzman suggested that it would be on hold this month, pandemic risk of concern but not yet meriting further action.

EU/UK post Brexit talks continue to be on hold while the UK Parliament debates its Internal Market Bill this week, with expectations that several amendments may be made. EU/UK discussions over the implementation of the Withdrawal Agreement Act (the divorce agreement, not the trade discussions) progressed well.

Event Outlook

Australia: Weekly payrolls (to Oct 3) will be released. The fortnight prior saw a modest increase of payroll jobs circa 0.3%.

The October RBA meeting minutes will provide additional colour on the Board’s view of risks to the economy and the outlook for policy. The RBA’s Assistant Governor (Financial Markets) Kent will also give a speech at the IFR Australia DCM roundtable webinar (10:00 AEST).

NZ: TheQ3 QSBO survey of business opinion should see a sharp rise from the weak June result of -58.8, although activity is still expected to remain below pre-Covid levels.

US: Housing starts (prior: -5.1%, market f/c: 2.8%) and building permits (prior: -0.9%, market f/c: 2.0%) are stabilising after a rapid recovery in Q2/Q3.

The FOMC’s Quarles (01:50 AEST), Evans (04:00 AEST) and Singh (04:30 AEST) will all speak.

The flighty bird that is equities and risk sentiment now looks quite stretched again:

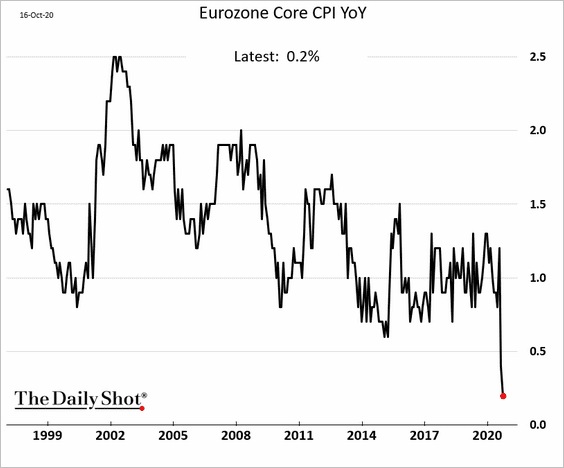

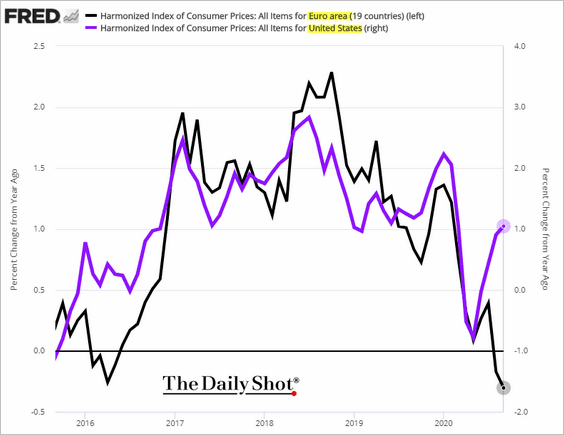

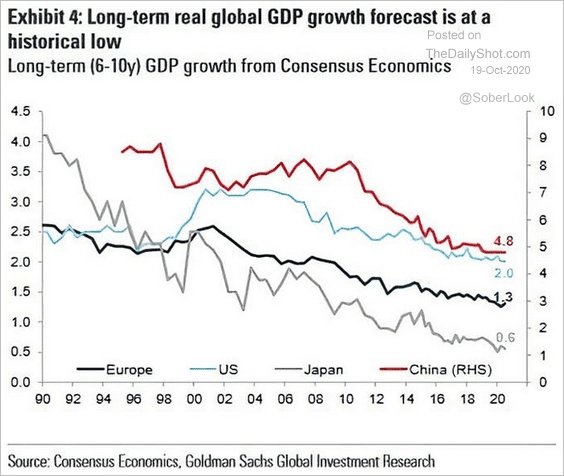

Nor do fundamentals line up well for further fakeflation. Remember, it is very dependent upon a falling DXY and that trade is facing increasing headwinds as Europe succumbs to the virus second wave and its economy sputters. Inflation is broken:

Especially compared to the US:

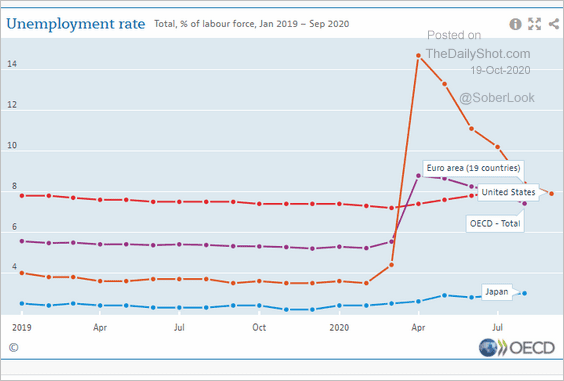

As unemployment rates converge it will stay that way. Europe has a lot more kurzarbeit than headcount losses than does the US:

Whatever bazooka that the ECB is going to pull it will have to be soon. At the end of the day, Europe has a lot more shit to push uphill than the US does:

Goldman sums up the unbalanced market:

With less than three weeks to go, the US elections have taken centre stage for investors, together with renewed risks of lockdowns and news on a potential Covid-19 vaccine.

How are markets positioned for the November US elections? Most positioning indicators remain at neutral levels but have started to pick up since the end of September. Fund flows haven’t shown a clear rotation towards riskier assets: equity registered inflows and money markets outflows, but government bonds have remained very positive. Speculative short positions on US bond futures have also recently been reduced, while US equity future net length decreased slightly. AAII Bulls vs Bear is still in negative territory but has recently started to increase rapidly. Sentiment on the Dollar remained very negative, with speculative future positions still at all-time lows and risk reversal turning more bearish against the Dollar. Sentiment on EM is still far from sending bullish signals but has started to improve timidly. EM fixed income inflows were solid over the last four weeks and turned positive in EM equity. Asset managers’ net positions on MSCI EM continued to increase. Across assets, MSCI EM recorded the largest decline in skew over the past month (Exhibit 1). In the US, equity right-tail risk remains priced, in particular in Tech, and after the recent spike in rates volatility long-term bond options have started to discount the potential for a large increase in rates. Put options on UST bonds have become very expensive vs calls.

Nobody is positioned for risk reversal even as risk climbs with virus numbers, politics and the ECB. If we get another shakeout then the Australian dollar will puke with all of these overbought trades.