Finally, it seems to have sunk in that there is no more US fiscal stimulus coming before next year which weighed on everything. It is the election, of course, which sees Dems campaigning for more stimulus and Reps for less having given up on a rump victory.

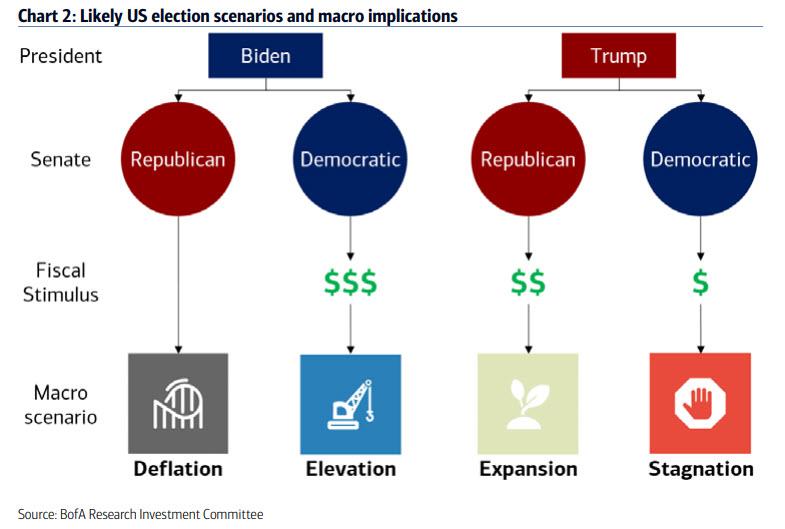

This sets up the dynamic for the post-election environment as well. BofA has some reasonable material on that:

1. President Biden + Democratic Senate = Bullish Elevation

While many investors say they fear the impact of a “Democratic sweep” because of higher expected taxes and greater regulation, BofA counters that a unified government would be bullish:

The desire to maintain majorities through midterm elections in two years incentivizes a pro-growth, pro-employment agenda now (fiscal stimulus, industrial policy) & redistribution only later (if ever). This is particularly urgent for Democrats, who have struggled historically to motivate voters in midterms;

Even if progressives impose new taxes & regulations, the bank expects that the planned consumption and investment incentives would more than offset the drag.

2. President Biden + Republican Senate = Bearish Gridlock

If Republicans retains the Senate they are very likely to block further stimulus under a Democratic President. After $21tn of monetary & fiscal stimulus in 2020, $0 of follow-on support would be deflationary.

Indeed, political parties historically have used obstructionist tactics when out of power to thwart key legislation, most often through the “rediscovery” of commitments to “fiscal discipline”.

Trades: in this scenario investors should prepare for lower returns and higher volatility. Raise cash and buy Treasuries, munis, and high-quality corporate bonds.

3. President Trump + Any Senate = Uncertain Stagnation

This is the “status quo” scenario: after the election, basic support packages may be easier to pass, but BofA doubts whether President Trump and a Democratic House would find enough common ground to pass transformative, pro-growth legislation. The case of infrastructure is instructive: both parties agree on the need for more resources for transportation, energy security, etc., but talks have always broken down over “red line” issues like immigration. That said, with a GOP Senate, investment may come more easily for R&D and industries relevant to national security.

However, the risk of volatile stagflation also rises with a divided government. Policies that have increasingly bipartisan appeal, such as regulating Silicon Valley or countering the threat from China, would require massive (and in this case, unlikely) domestic public investment to offset related frictions.

Trades: long stagnation winners e.g. tech, consumer discretionary, large caps, IG bonds…but with less leverage and lower market beta.

4. Contested election = Buying Opportunity

…there are several unusual but plausible scenarios and no real historical precedent…the same features of the US economy that made every investor in the world desperate to buy US assets in 2020 will still exist in 2021, no matter the election outcome: the deepest and most liquid financial markets, strong institutions, the rule of law, and the most productive, creative workforce”.

Trades: treat any market decline on a contested election as an opportunity to buy risky assets and sell volatility.

Advertisement

I will add that I don’t see option two as overly bearish given it will also result in lower tax hikes. Here’s my best guess for the outlook for AUD in each:

DXY down, AUD up (though not very far given US yields spreads widen more than Australian).

DXY up, AUD down as risk retrenches.

DXY slowly down, AUD down too as risk remains upside down.

4. DXY up, AUD thumped.

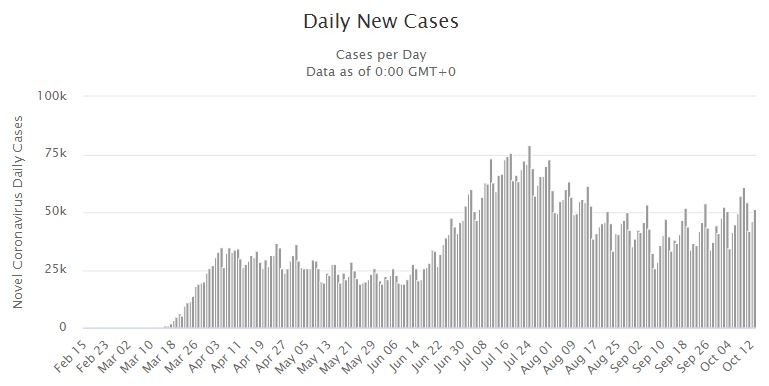

We need to add some virus calculations too. It looks increasingly likely the Biden Administration will inherit a US third wave larger than any previous. Heading into the second winter the base is very high and accelerating:

Advertisement

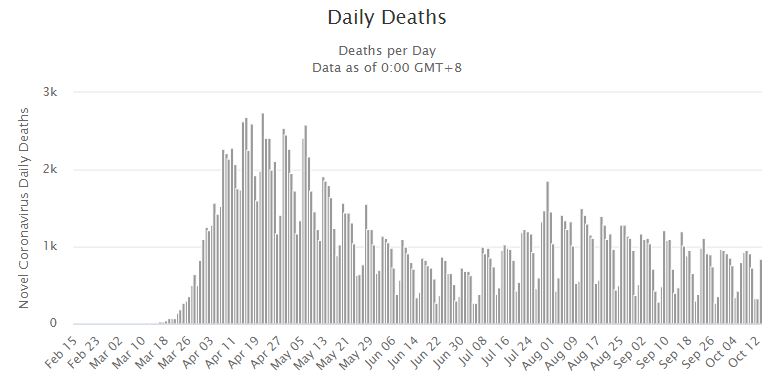

Deaths are about to rebound:

Vaccines and advancing treatments will help after Q1 but that’s too late for the inauguration period. Biden is on record saying he will listen to science. I don’t foresee a national lockdown but regional and local lockdowns are much more likely under Biden than Trump.

Advertisement

Finally, I will say that a Biden Administration’s softer stance on China is a tailwind for AUD, especially if the local CCP insurgents get a second wind, though that is speculative.

So, I am still struggling to find any bullish scenario for the AUD in the near term. Medium-term, with the most likely outcome being a blue wave election, there’s some modest bullishness for the battler deeper into 2021. But even that does not get very far given the further we get into next year, the more Australia’s misfired budget will weigh on yield spreads and the lower iron ore price will go as Chinese restocking tops out.

In short, the vast majority of gains in the AUD are already behind us.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.