Voluntary payments into mortgages more than doubled in July, August and September from the previous 12 months, data from non-bank lender Firstmac shows…

Firstmac’s analysis of its $5.8 billion direct retail mortgage book shows the level of additional payments made by borrowers jumped to an average 10.2 per cent of the portfolio in the past three months, compared with the monthly average payment of 4.8 per cent last year…

“There’s obviously a lot of money flowing through the economy and people are choosing to save that money,” Firstmac chief financial officer James Austin told The Australian Financial Review.

“Paying down the mortgage is another form of saving.”

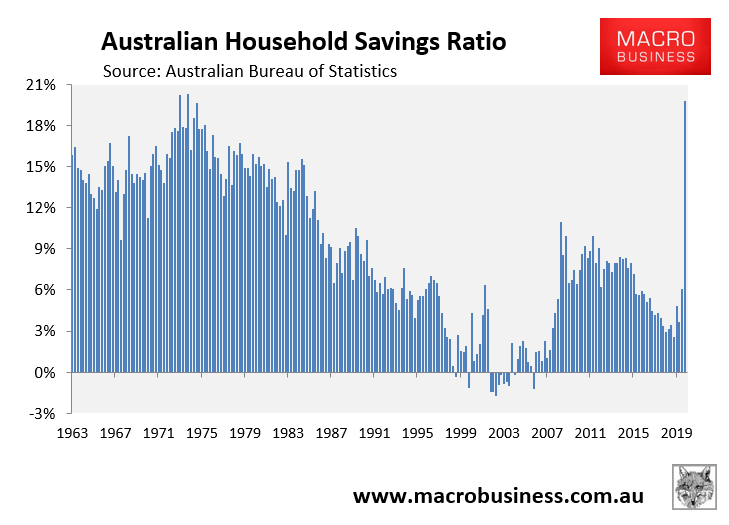

The macro data supports Firstmac’s observations.

Australia’s household savings rate ballooned to a 50-year high in the June quarter:

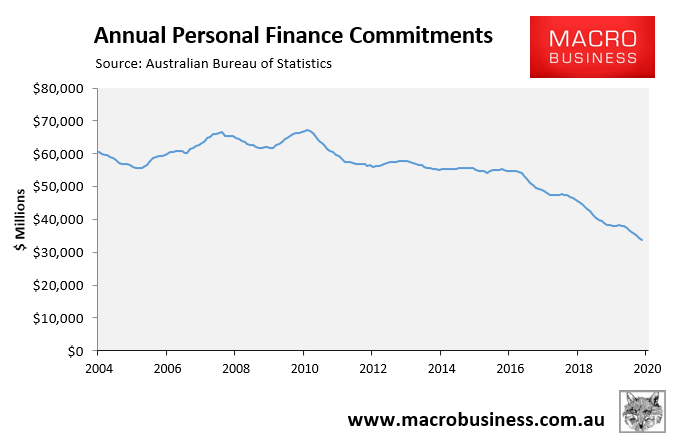

Personal finance commitments have collapsed:

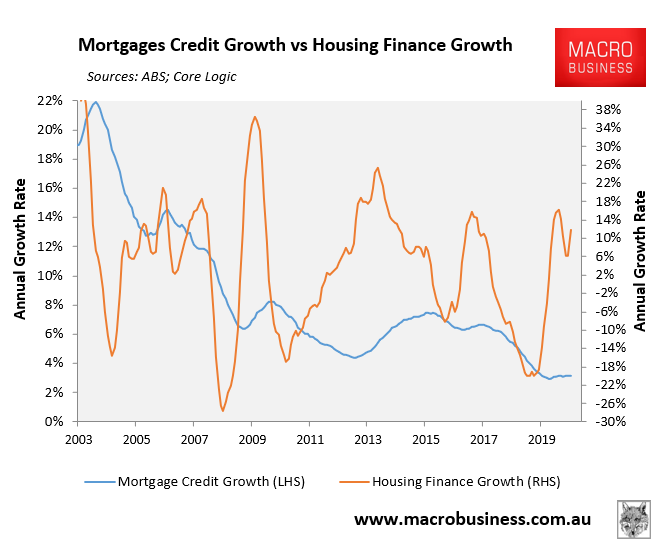

And most tellingly, growth in the stock of mortgage credit outstanding (mortgage growth) has flatlined as new mortgage finance commitments (housing finance growth) has soared:

This should be viewed as a harbinger for the Morrison Government’s tax cuts, with Aussie households likely to save the additional disposable income rather than saving it.

Accordingly, tax cuts are unlikely to have the stimulatory effect to the economy that the Government is hoping for.