As carry trades flip negative, has the Australian dollar topped?

Via Credit Suisse:

While we had previously looked to fade backups in rates ahead of the election — given our expectation for fiscal stimulus discussions to remain stuck, corporate supply to taper off, and the Fed to keep conditions accommodative — the meaningful change to the election calculus overwhelms these considerations and suggests leaning short (and toward steepening) is most prudent.

That is true as far as it goes. The steepener trade will also be aided by the vaccine rush. I buy it enough for us to have shortened duration in our portfolio considerably. But it also has to get through another COVID winter in the northern hemisphere plus all kinds of election stimulus balderdash so I don’t expect it to be smooth trade.

Westpac has more for Australia:

The AOFM borrowing task and funding strategy is expected to be released on Wednesday morning. At first glance, using the budget deficit plus term maturities, the call on investors in 2020-21 is expected to be around $259bn. That assumes, of course, that the budget deficit evolves as forecast (Westpac believes that the actual deficit will be larger) and that it is fully funded via term issuance. However it remains possible that the AOFM’s announced requirement might differ, perhaps significantly, from that assessment. The other variables include the fact that the AOFM has already raised a significant amount of their yearly task ($117bn). So, will that reduce their borrowing requirement, or will they look to achieve a significant amount of “pre-funding” outside of the traditional buyback programmes? Alternatively, it is worth noting that the AOFM could well announce a bigger program than the budget suggests as they will want buffers given the current uncertainties. So how the AOFM approaches their requirement will be extremely interesting and important to market outcomes. While the budget provides little guidance, In terms of total AGS, short-term Treasury Notes are increasingly important. For example, last fiscal year the AOFM issued $90bn, as outstandings rose from $3bn to approximately $58bn by year-end.

Leading into the Budget, Westpac had been of the view that the 2020-21 term borrowing requirement would be around $285bn. At the same time we discussed with investors a range of around $240bn to $295bn. It was our view that anything within that range was already “in the price” and unlikely to provide a significant surprise for markets. So market expectations were basically met and it is therefore not surprising that bond futures have barely moved on the release of the Budget details. Looking more medium term, one question worth asking is whether the demand equation is likely to shift significantly. That is, we often ask who will the marginal investor be? Despite some prior reservations earlier in the pandemic, no “tipping point” has occurred at which further debt funding attracted a penalty. Australian bonds have continued to be bought by global investors seeking yield and also by local ADIs under bank liquidity regulations and by the domestic fund management community for benchmarking purposes. The question is whether they will continue to do so despite record low absolute yields. We think they will, as relatively speaking, AU yields continue to represent value on a “reward for risk” basis versus global alternatives.

Given the scale of the forward deficit profile and the fact that infrastructure remains a Budget focus, there is likely to be ongoing steepening pressure on the 10-30yr curve. Although, again, that is largely as expected and in the price. Long-dated bonds have been issued for some time and valuations are well established, and the AOFM has a good track record of issuing into a positive demand environment at opportunity.

Supply arguments for fixed interest don’t interest me. Much more significant is inflation expectations. The budget massively under-cooked infrastructure spending, as well as demand support broadly, which is why yields fell sharply afterward.

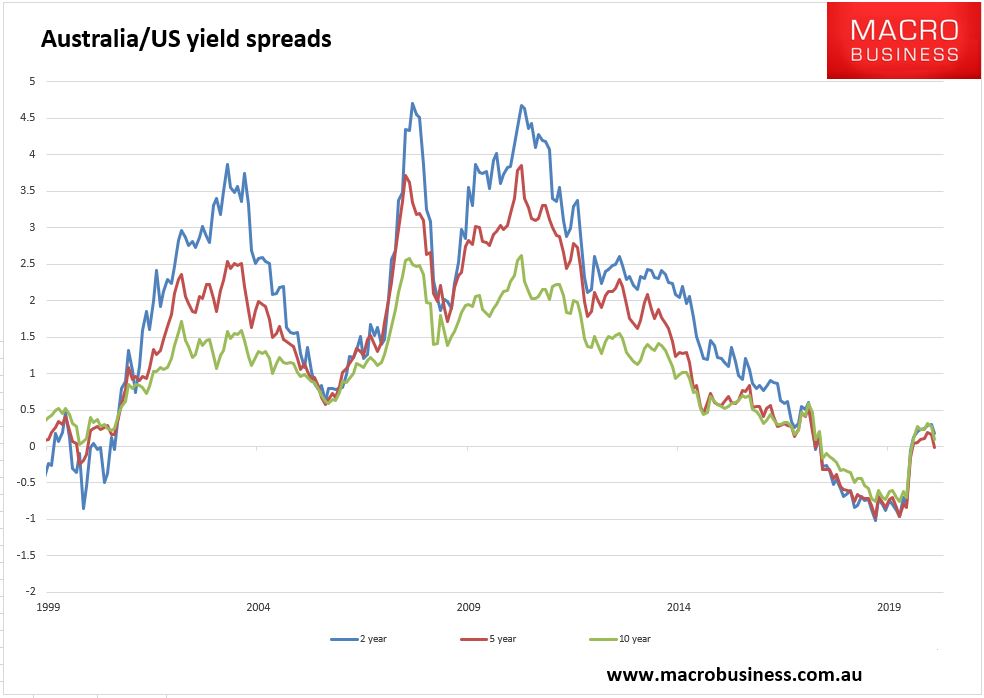

These two arguments are getting me excited about the possibility that the Australian dollar has topped out. Next year the great likelihood remains that DXY will resume falling as the slow global recovery continues. But, if US fiscal remains so much more aggressive and better targeted than the Depressionberg Unstimulus, then the AUD will resist that DXY push and may even fall anyway as the RBA is forced to close the gap to an exceedingly easy FOMC. The AUD/USD yield spread has already rolled across the curve and inverted on the five year:

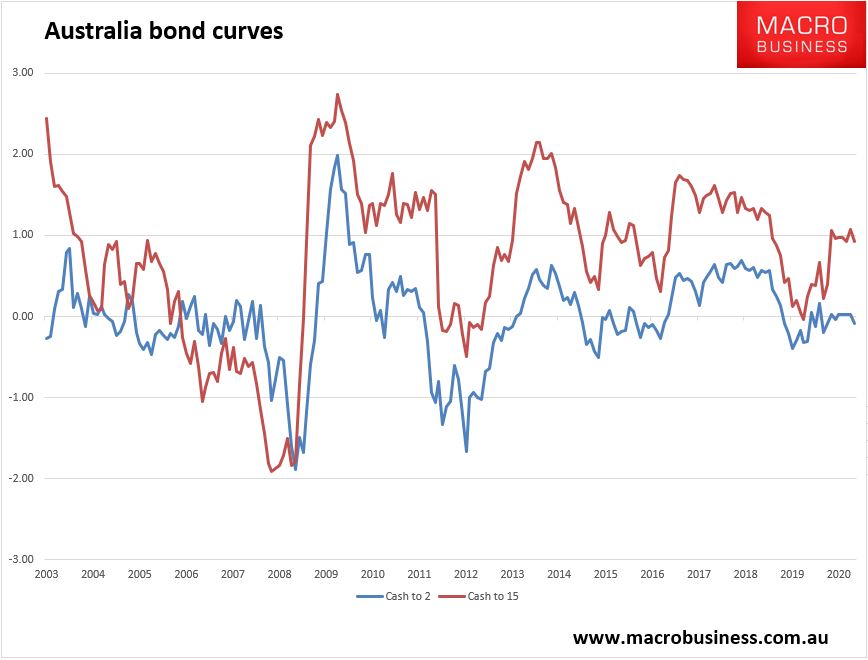

Plus the curve here is still too steep assuming the RBA is going march out the curve with “operation twist” and QE:

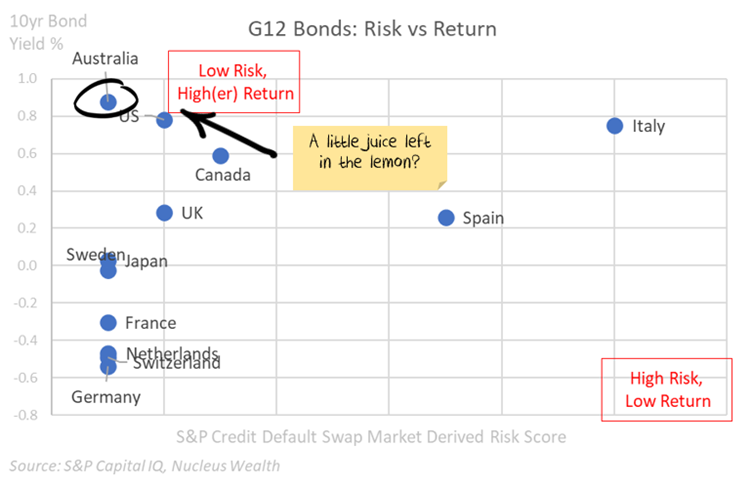

As well, Aussie bonds are still very good value versus just about everywhere else:

So there is plenty of room for yields and the spread to fall.

There will still be terms of trade support for the AUD through mid-2021, which is about when I expect iron ore will begin a big mean reversion, so I can’t say for certain that the currency has topped out. What we can say is that the carry trade domino is moving into place.

David Llewellyn-Smith is Chief Strategist at the Macrobusiness Fund, which holds large offshore investments to benefit from a falling Australian dollar.

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance.