CoreLogic’s head of research, Eliza Owen, believes concerns surrounding the ‘mortgage cliff’ are exaggerated:

COVID-19 exacerbates the risk that high housing debt has to the Australian economy. In the March quarter, the ratio of household debt to annualised household disposable income sat at near-record highs of 142.0%.

With widespread unemployment, there is increased likelihood borrowers could fall behind on mortgage repayments, with the potential to generate forced sales. This in turn could increase the supply of listings, and put further downward pressure on dwelling values.

Many banks offered a pause on mortgage repayments early in the pandemic to reduce this risk. As of June 2020, the value of housing loans deferred was $195 billion, or 11% of total housing loans.

These ‘mortgage holidays’ are temporary, and were initially in place for 6 months from March 2020. This led to concerns over a ‘September cliff’, where mortgage holiday repayments and fiscal support policies would be repealed as the economy was yet to recover.

However, it is important to remember that no entity has an interest in seeing residential mortgages fall off a ‘cliff’ come September. Residential mortgage lending accounts for about 60% of bank lending. Housing accounts for about 53% of household wealth, and the accumulation of wealth in housing eases pressure on the government to fund Australians in retirement.

Thus, it is unsurprising to see that both banks and statutory authorities are looking to extend repayment deferrals where it is needed. In a letter to banks, APRA advised that for loan repayment deferrals provided prior to September 30 2020, ADIs could continue to apply a ‘temporary capital treatment’ to a total deferral period of 10 months, or up to the end of March 2021. The ‘temporary capital treatment’ means that APRA does not count a deferred loan as in arrears, or as restructured.

Interestingly, of this deferred volume, only 8% had a loan-to-value ratio of more than 90%. In addition to the national property price upswing of 8.9% between July 2019 and April 2020, it likely that relatively few of the borrowers deferring their mortgage repayments are in a negative equity position.

This is important, as recent research from the RBA has highlighted that foreclosure on mortgages is far less likely when the borrower is in a positive equity position.

It is also worth keeping in perspective that not every Australian has the same level of risk when it comes to housing and debt. For example, around 30% of Australian households own their home without a mortgage. RBA research suggests that over 50% of loans had prepayments of at least 3 months, and about 30% of loans had prepayments of at least 3 years. However, this is not to say parts of the market are without risk.

The same data set showed just under one third of mortgage holders had less than one month of prepayment, and that this group with low repayment buffers were more likely to experience financial stress.

The markets more likely to see a dangerous combination of negative equity and mortgage arrears have recently been mining regions, such as the north western region of WA.

More recently, there is evidence to suggest more severe price falls and disruptions to loan repayments could occur across inner-city apartment markets of Melbourne, and potentially Sydney.

Eliza Owen may end up proven right. However, there are good reasons to be concerned.

First, the ending of mortgage repayment holidays will more or less coincide with the unwinding of emergency income support (e.g. JobKeeper), early superannuation withdrawals, and the temporary moratorium on insolvencies. Thus, there is the potential for a large number of forced sales driving property prices lower.

Second, the risk is greatest for highly leveraged, negatively geared landlords in Melbourne and Sydney. These markets are most exposed to the collapse in immigration, and both property prices and rents are already falling.

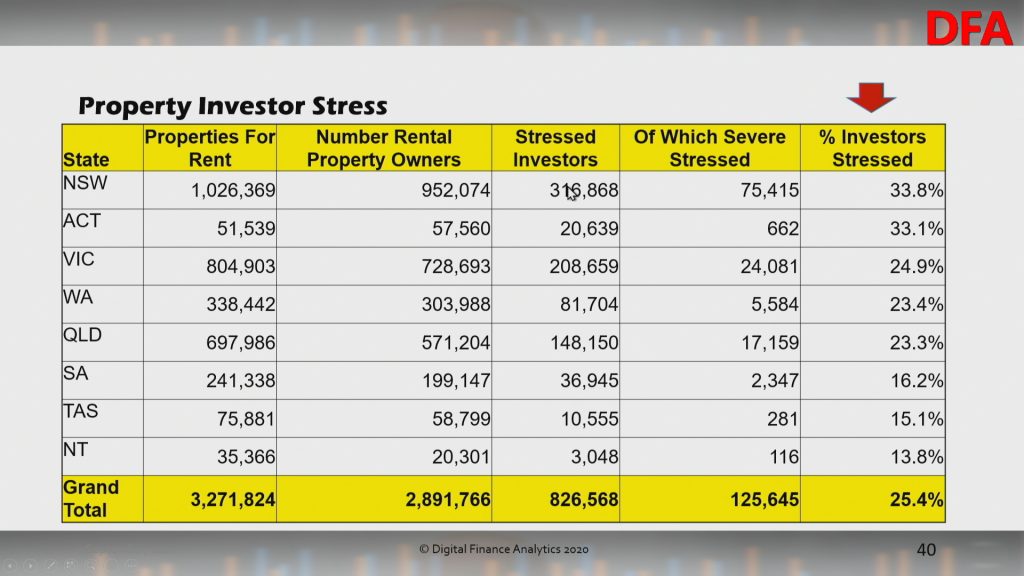

According to Martin North’s latest mortgage stress survey, one quarter of property investors (around 50% with a mortgage), were cash flow negative in August:

As shown above, a significant share of landlords in NSW (33.8%) and VIC (24.9%) are experiencing mortgage stress, with 7.9% in NSW and 3.3% in VIC experiencing “severe stress”.

With property investors experiencing both falling income and wealth, many will be heavily incentivised to cut their losses and sell.

This, for me, is the key risk facing the Aussie property market in 2021.