Why not make it 100% by 2070? Via Bill Evans at Westpac:

Westpac expects mild (5%) dwelling price correction through to late 2021 to be followed by 15% surge over the next two years.

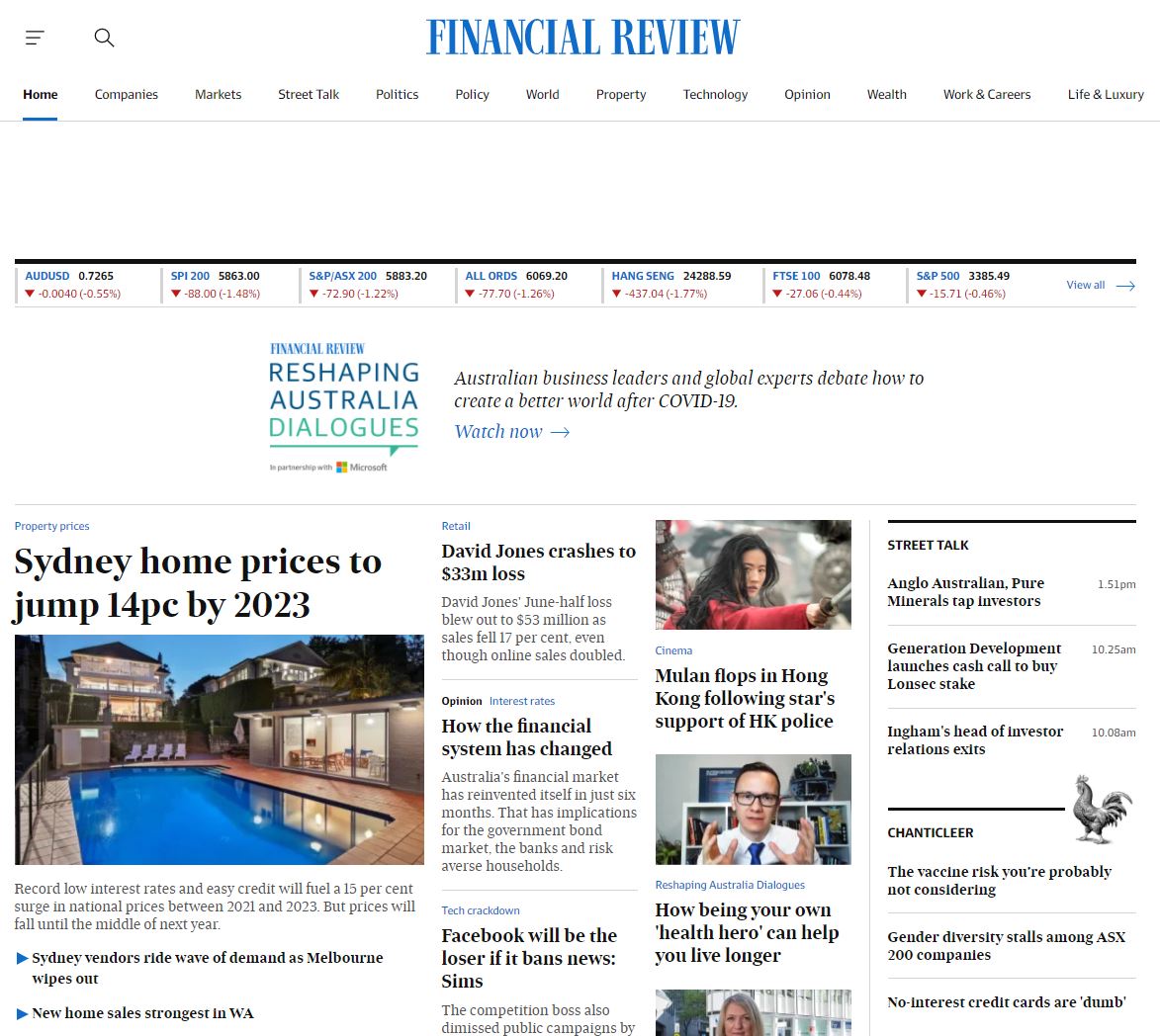

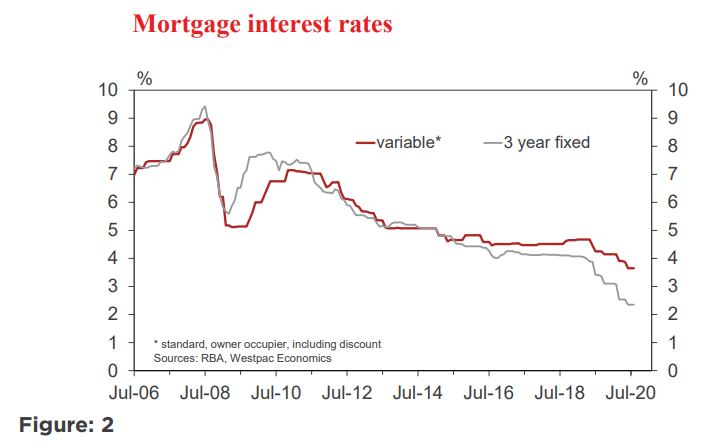

To date our view has been for a 10% fall in prices nationally from the peak in April 2020 through to June next year. From that point we expected increases of around 4% per annum over the following two years. The 10% near term fall was forecast to be distributed between Melbourne (–12%); Sydney (–10%); Brisbane (–8%); Perth (–4%) and Adelaide (–8%).

We now expect many capital city markets to be more resilient with a national fall of 5% between April and June next year, distributed between: Melbourne (–12%); Sydney (–5%); Brisbane (–2%); Perth (flat); and Adelaide (2%). Of most importance is that we are much more optimistic about the pace of price appreciation over the following two years with a total expected increase of around 15%.

For the near term, our revised view this means prices nationally are now only expected to fall a further 2.3% out to June next year (prices having already declined 2.7% since April).

We see the house price profile unfolding in four distinct stages.

The first, which has now largely passed, is the initial impact on prices from the collapse in economic activity in the June quarter.

That has seen broad based declines in Sydney (–2.6%); Brisbane (–0.9%); Perth (–2.6%); Adelaide (–0.1%) and a more severe fall in Melbourne (-4.6%).

However, the pace of deterioration outside of Melbourne has been milder than we expected back in March.

The second stage, which will cover the December and March quarters, will be a period of relatively stable prices, possibly with some modest increases, although Melbourne will be at least one quarter behind the other states and will still be experiencing falls in prices in the December quarter.

The third stage will see some limited resumption of downward pressure on prices through 2021, as we see an increase in ‘urgent’ or distressed sales relating to borrowers struggling or unable to resume mortgage repayments. Again, more adjustment is likely in Melbourne than the other cities.

The fourth phase will come once this selling pressure has worked through the system and prices lift again.

This recovery will be supported by sustained low rates, which are likely to be even lower than current levels; ongoing support from regulators; substantially improved affordability; sustained fiscal support from both federal and state governments; and a strengthening economic recovery (particularly once a vaccine becomes available, which we expect in 2021).

Why do we now see prices stabilising near term? There are two main factors behind our change in view:

1. A more substantial boost from lower interest rates, especially low fixed rates

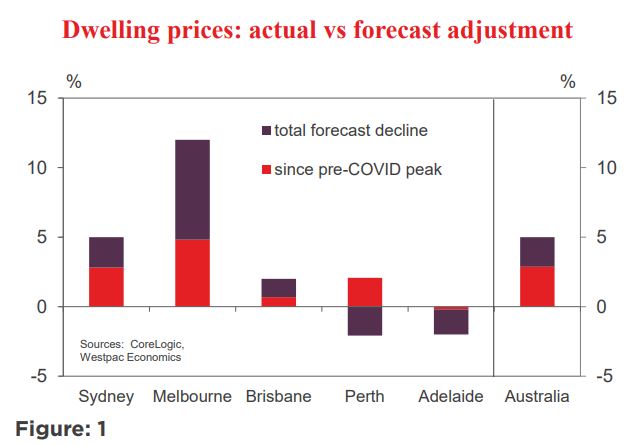

Over the last 12 months the average discounted variable mortgage rate for owner occupier loans has declined from 4.25% to 3.65% (–60bps). Of special interest has been the fall in average 3–year fixed mortgage rate which, for owner occupier loans, has moved from 3.41% to 2.35% over the same period.

This is a record 130bps below the discounted variable rate and 190bps below the discounted variable rate a year ago – while the cash rate has only been lowered 75bps, the pick up for the marginal borrower is closer to 200bps if they now opt to fix.

Borrowers have been drawn to the lower fixed rates on the reasonable assumption that there is little to lose. Further significant reductions in the overnight cash rate, which traditionally impacts variable mortgage rates, are unlikely. The Reserve Bank of Australia (RBA) has identified the current 0.25% cash rate as the effective lower bound.

On the other hand, fixed rates may well go lower. The RBA indicated last week that it is prepared to further increase low cost funding to the banks by extending its Term Funding Facility (TFF), which offers 3 year loans to banks at 0.25%, from at least $152 billion by a further $57 billion. This facility could indeed grow to up $300 billion by mid–2021.

While banks may be expected to mainly use this facility to reduce funding costs – by replacing more expensive offshore funding, scaling back domestic retail deposits (some term deposit rates are still comfortably above 1%), or boosting their liquidity holdings as the Reserve Bank’s Committed Liquidity facility is wound back – there is also scope for cheap maturity– matched fixed rate mortgage funding. On that basis fixed rate mortgages could fall considerably further.

The RBA could also move to lower longer– term fixed rates by extending the duration of the TFF loans and/or targeting.

With such high exposure to the housing market in their portfolios, through both mortgages and small business loans, banks have indicated that they will look to manage these issues in an orderly fashion, minimising market disruptions and allowing a range of options including restructuring.

A patient strategy will also be supported by the stimulatory fiscal and monetary policy environment; and ongoing support from the regulator who is already showing patience in the way banks can account for their deferred interest loans.

Theoretically, investors (around 35% of total housing loans) might be more vulnerable but recall the extremely low funding costs which in most Australian markets are below rental yields.

With positive cash flow these loans should make borrowers less vulnerable to financial stress.

This process is expected to be at its most active in the June and September quarters next year although further extensions are likely.

One specific group of investors that may experience considerable additional pressure are those impacted by the collapse in net migration due to the closure of the international borders.

The Commonwealth government forecasts a reduction in net migration in 2020/21 from 232,000 in 2018/19 to 31,000 in 2020/21.

This shock can be expected to have its major effect on the rental market in the high– rise parts of Sydney and Melbourne which typically attract students and other temporary migrants. Around 70% of Australia’s net migration inflow is now from temporary visa holders, the overwhelming majority of whom are renters rather than owners. Furthermore, industry reports point to significant further supply coming on to these high–rise market.

This discussion of the third phase concentrates on the impact of a lift in supply from distressed sellers. However there will be some offset from demand conditions, which will still be strong, supported by record low interest rates; policy stimulus and a recovering economy.

Phase 4: sustained upswing

In the fourth phase, which we expect will continue for at least two years, prices are likely to be responding to the ongoing strong liquidity in the system; record low rates and freely available credit.

Unlike other cycles, the authorities – both fiscal and monetary – will be focussed on lifting the economic growth rate by targeting falls in the unemployment rate. That task is likely to be difficult and ongoing since we expect the unemployment rate to hold above 7% through to 2023.

In addition, the Reserve Bank will be also be focussed on lifting chronically low wages growth and inflation.

Concerns around excessive increases in dwelling prices; the need to limit credit supply; or the size of budget deficits which have dominated the pre COVID policy debate will continue to be superseded by the drive for labour market and inflation targets in 2021–23.

This will be a very constructive environment for dwelling prices.

Aside from ongoing support from policy, housing markets will also be buoyed by a strengthening economic recovery, slowly improving labour markets, the resumption of migration inflows and potential shortages of new stock.

We expect price increases over that 2021–23 period of 15% – around 7.5% per year.

These increases are likely to be distributed as: Sydney (14%); Melbourne (12%); Brisbane (20%); Perth (18%); and Adelaide (10%).

On the basis of those increases we would see affordability modestly worse than long run averages for the nation as a whole, with the advantage enjoyed by the smaller states diminishing.

Readers might see that estimate as optimistic but there are some risks to the upside.

Including the 5% fall we expect out to mid–2021, this would see a cumulative increase in prices of 10% from pre COVID highs over a three–year period where interest rates and credit supply are likely to be at maximum levels of stimulus.

Those upside risks are based on the psychology of markets.

If participants are convinced about our views on the likely favourable conditions in the fourth stage of the cycle they may choose to boost demand earlier than we currently expect providing an even more robust defence against the headwinds we envisage in stages two and three.

Summary: the full cycle

To recap, we see four distinct phases of the housing outlook.

1. Price falls in response to the initial COVID shock – which, apart from Melbourne, are largely behind us.

2. Relatively stable prices in the December and March quarters, with gains possible in some markets although Melbourne will still be experiencing falls in the December quarter.

3. A minor softening in prices through the June and September quarters in 2021 as lenders gradually ease back loan deferrals while seeking to avoid significant market disturbance. These efforts will be supported by ultra–easy monetary and fiscal policy; regulatory support; and ongoing economic growth.

Nevertheless, there will be ‘pockets’ of weakness associated with inner–city high– rise markets in Sydney and Melbourne and those overstretched borrowers who will be exposed by the failure of their underlying businesses.

4. The fourth phase will span at least two years when distressed loans from deferrals have worked through the system – and prices react strongly to ongoing low rates; improved affordability; a strengthening economic recovery and policy stimulus. Dwelling prices are expected to lift by 15% over this two–year period.

I have highlighted the ONLY line that matters in this argument. To be honest, I could shorten that to the phrase “the resumption of migration inflows”. There is no property rebound coming in Sydney or Melbourne before that. Quite the opposite. Prices will fall as rents are eviscerated and investors bolt.

Advertisement

Other capitals look better but they are about to get shocked by the fiscal cliff too. And why is nobody taking account of rates being at rock bottom, with the RBA put dead, so leveraging up has a new risk. In fact, Bill Evans has glossed over an entire suite of risks:

trouble with the vaccine rollout (guaranteed);

therefore slow border openings;

difficulty lifting immigration owing to high unemployment, virus and China decoupling;

China decoupling;

ongoing income shock;

restructuring business as the fiscal cliff arrives leading to double-dip recession, and

stock market bubble burst.

I remain bearish on prices (most especially the SE capitals) and think next year’s troubles are being severely underestimated by an increasingly hysterical spruikfest.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.