Australian economic recovery is faltering, and more policy stimulus is likely

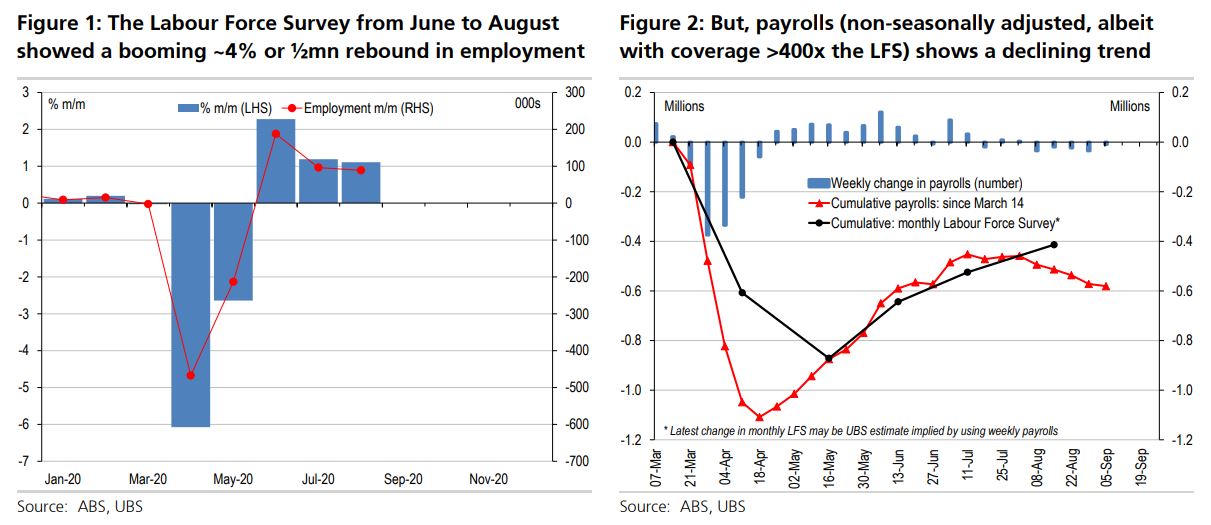

The Australian economy initially significantly outperformed global trends, with Q2 GDP down ‘only’ 7% q/q, and a strong rebound in early Q3 data, seeing the unemployment rate surprisingly drop back to 6.8%. However, recently there are signs the recovery is slowing, or even stalling. Much of this weakness is driven by a 2nd wave of COVID resulting in tighter mobility restrictions in Victoria, which are starting to ease, albeit only quite slowly. Worryingly however, the rest of Australia also softened. In contrast to the Labour Force Survey – which showed employment boomed in the three months to August by near ~4% or ~½mn jobs – payrolls have trended down since July, decreasing by 1% or implying >-100k. Similarly, pre-COVID, the 0.7mn unemployed in the LFS was the ~same as JobSeeker. But, August LFS unemployment fell back to <1mn, while JobSeeker rose towards ~1.5mn (and ~1.7mn including ‘other’ Youth Allowance). This indicates the true labour market is far weaker, with implied unemployment >10%. There is also still another ~3mn+ on JobKeeper, who will need to be ‘directly paid’ by their employer when the subsidy tapers. Furthermore, retail and car sales dropped drop back sharply in August, after booming in prior months. Indeed, the 2nd wave of COVID globally raises the risk of renewed lockdowns, including keeping Australian borders shut for longer, with the Treasurer now expecting no migration in FY21/22. Hence, we still expect Q3 GDP to recover only 0.6% q/q, and Q4 just 1.0% due to the fiscal cliff, seeing the unemployment rate lift sharply towards 9% over coming months.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.