The mortgage repayment cliff “will be devastating”

Economist Jason Murphy believes that the mortgage repayment cliff will hurt the housing market and economy in one of two ways:

- It will drain the economy of household disposable income; and

- It could lead to a significant number of forced sales, driving property prices lower.

From News.com.au:

In the next few weeks 450,000 Aussies will be getting a call asking them for money they may not have. The knock on effect will be devastating…

Six months ago banks handed out loan deferrals like lollies. Now they’re coming to take the deferrals away…

The boss of the Australian banking association calls it the “largest ever customer contact process in the industry’s history.”

Hundreds of thousands of mortgage customers and around 100,000 small business loans are up for reassessment, and banks will be keen to get people paying again…

The missed payments need to be made up, and the extra interest is added on top…

Westpac CEO Peter King confirmed on Friday that some customers are now in strife…

As the tidal wave of loan deferral phone calls happens around Australia, the after effects will spill out and affect the rest of us. This will happen in two ways…

In the best case scenario, people who were worried they were going to lose their job actually didn’t. They simply start repaying their loan. That’s great news for the banks but it is not always best for other businesses… If this effect is large it could hurt sectors of the economy that depend on consumer spending…

The hardest conversations banks will have with deferred customers are ones where they can’t start to repay again.

Houses will get sold… The impact of any forced sales will be felt in the housing market. If a lot of people are forced to sell their properties at once, there could be a rush of supply.

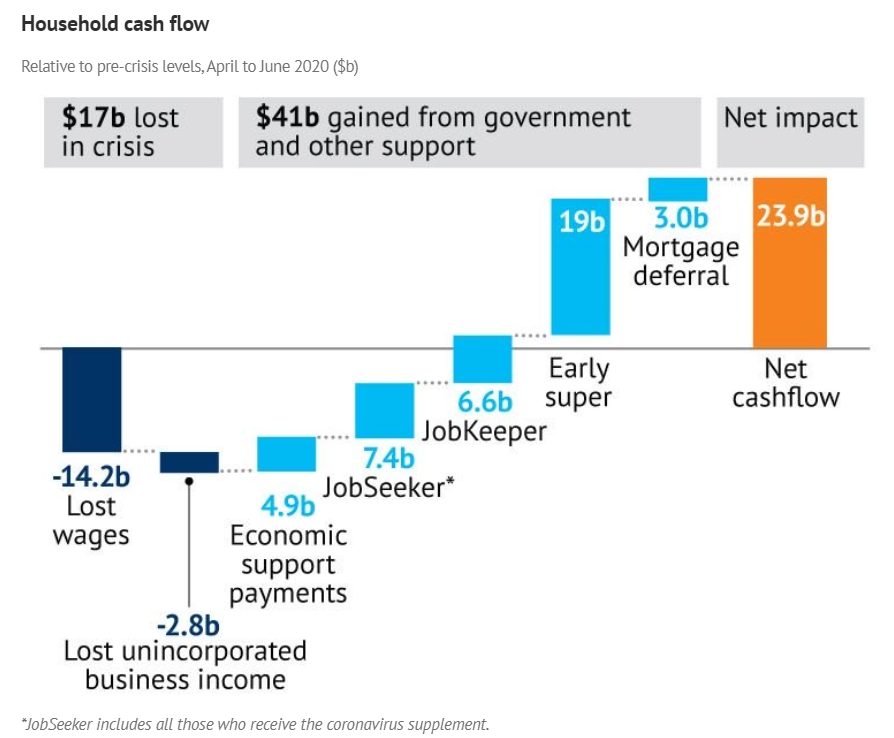

According to AlphaBeta, the gain to household disposable income from mortgage repayment holidays is only small at around $3 billion. Thus, recommencing repayments won’t have too much of an impact on household disposable income in isolation:

The bigger concern is that the mortgage repayment ‘cliff’ is scheduled to coincide with the unwinding of other ‘cliffs’, namely reductions in JobKeeper and the JobSeeker supplement, as well as the expiry of early access to super.

As shown above, the unwinding of all of these emergency measures in concert will clobber household disposable income, resulting in even lower consumption spending and reducing the ability of Aussies to repay their debts.