Paul Keating scattered them briefly but you can’t keep a good cockroach down. Patrick Commins is one:

In an extraordinary attack on the country’s most revered economic institution, the former prime minister damned the central bank’s “indolence” through the COVID-19 crisis, accusing it in a statement of being “way behind the curve in supporting the government in its budgetary funding measures”.

…former RBA board member Warwick McKibbin defended the bank‘s record, saying Mr Keating’s attack on the RBA’s performance through the crisis was misplaced. “This is a recession where it’s fiscal policy that really needs to take the lead,” Professor McKibbin said.

The central bank was already playing its part by buying government bonds in the secondary market, and buying directly from the government would “undermine the credibility of the central bank”, he said.

“The recession in 91 was caused by Paul Keating and his inappropriate policies,” Professor McKibbin said. “He is the wrong person to be criticising the bank, when he was the one who caused that recession.”

Patrick’s “most revered economic institution” is the usual grovelling for access. As for, Wazza. That’s what Keating is arguing. More fiscal. Mountains of it. The RBA can break the stupid surplus obsession.

Wazza returns with head RBA scuttler, John Kehoe, at the AFR:

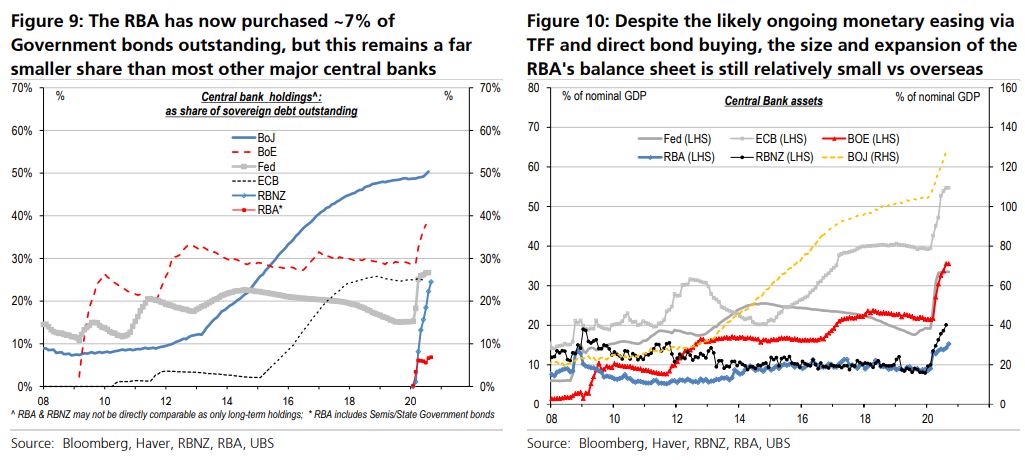

Professor McKibbin said the RBA was already undertaking a mild “Keynesian monetisation of the deficit” through buying more than $60 billion of federal and state government bonds so far, “but it’s not uncontrolled”.

“The bank has done everything by the book they possibly can and the recession is now a problem for [government] fiscal policy – income support and supply side productivity reforms,” said Professor McKibbin, who was the bank’s head of research in the late 1980s.

“You don’t want the political cycle to drive monetary policy.

How is this politicising the RBA? The RBA itself is demanding more fiscal spending from states and Canberra. Nobody has argued its inflation target should be changed or abolished. So long as that hasn’t happened RBA independence is fully intact. More groveling for access.

Another prostrate louse kissing the RBA ring is Bernard Keane at Crikey:

“Monetary policy can now no longer add to nominal demand,” Keating says, “something that now only fiscal policy is capable of doing.”

He’s dead right — further stimulus is now a matter for the government and its fiscal plans, not the RBA. But then he devotes several hundred words to belting the bank because it is “way behind the curve in supporting the government in its budgetary funding measures”.

That’s despite, as he admits, the RBA “showing some unlikely form in pursuing its 0.25% bond yield target for three-year Treasury bonds and a low-interest facility for banks”.

The three-year bond rate of 0.25% target reinforces what was already the case before the pandemic: the government doesn’t have to worry about the cost of borrowing in devising how much fiscal support to provide.

Josh Frydenberg and Scott Morrison are already in the process of delivering more than $200 billion in deficit spending into the economy; they haven’t been sitting in ERC sweating.

Poppycock. Much of that $200bn is already spent. Ahead is vast fiscal retrenchment to the tune to 10% annualised of GDP. Any arthropod that can’t get his facts straight should stay out of the debate.

Former RBA chief Bernie Fraser chimed in:

However, Mr Fraser said the RBA had been doing all it could despite having a “depleted ammunition box” having headed into 2020 with record low interest rates and have since lowered them further.

“I’m surprised [Mr Keating] sees there’s a problem because I haven’t seen a problem with the bank restricting or inhibiting the ability of governments to get liquidity or debt to fund their deficits and so on,” he said.

“I’ve been happy to see the bank express views about the need for fiscal policy and investment in infrastructure and so on because that’s basically what it’s all about. It’s fiscal policy that has to [step in] … the bank can’t do any more other than to keep liquidity there.”

Treasurer Josh Frydenberg also defended the bank, saying it was independent and the comments were a “very nasty, vindictive, unnecessary, misguided attack”.

Bernie the banker who will not want more easing to hit his margins. That Josh Depressionberg can’t see that Keating is defending his best interests is the ultimate condemnation of the pest and policymaker.

Another RBA Murdoch cootie yesterday was Adam Creighton:

But Mr Keating’s call to fire up the metaphorical printing presses and put however much money in the government’s bank account it asks for, is risky and premature.

No other nation — not even the quantitative easing pioneer the Bank of Japan — has directly purchased bonds from its government, let alone dispensed with the pretence of government bonds entirely, and then simply plonked the dollars requested in the government’s account at the RBA.

For Australia to do so would risk undermining “the stability of the currency”, which along with “full employment” is another of the Reserve Bank’s legislative mandates. History shows us that unemployment can’t be shifted for long by monetary policy anyway; money, as they say, is a veil.

Rubbish. The RBA is FAR behind the curve on every monetisation measure:

A good dose of currency instability is exactly what we need. Give us 40 cents. 30 cents! Who cares. Lower the better:

- to devalue wages and asset price externally or it will happen internally;

- to offset collapsed immigration and repair the crashed international student trade;

- to offset broader, epochal Chinese decoupling;

- to offset ongoing virus curtailments;

- to offset exhausted monetary policy and household peak debt with a low currency and booming tradable sectors;

- to repair the budget;

- to fight 23% un and underemployment, and

- to fight tidal deflation.

And that’s the rub. All of this RBA brown-nosing is based upon the very same incrementalism that Keating was attacking. The credibility of that position relies upon COVID-19 being a normal business cycle shock requiring normal, incremental monetary responses.

Look at that list of headwinds and tell me that it’s normal IN ANY WAY. It’s got MASSIVE STRUCTURAL ADJUSTMENT written all over it. Thus we don’t need the usual vermin-led bubble management. We need structural change, including at the RBA.

Keating may be a boofhead but he can see the big picture. Conversely, cockroaches can’t see above the level of the floor.