The latest RBA Bulletin contains an interesting report on COVID-19’s impact on Australia’s residential rental market, which it claims is experiencing “an unprecedented shock” with “reducing demand for rental properties at the same time as supply has increased”:

The COVID-19 pandemic is an unprecedented shock to the rental housing market, reducing demand for rental properties at the same time as supply has increased. Households most affected by the economic impact are more likely to be renters, and border closures have reduced international arrivals. The number of vacant rental properties has increased as new dwellings have been completed and some landlords have offered short-term rentals on the long-term market, particularly in inner Sydney and Melbourne. Government policies have supported renters and landlords. Rents have declined, partly because of discounts on existing rental agreements and it is likely that rent growth in many areas will remain subdued over coming years…

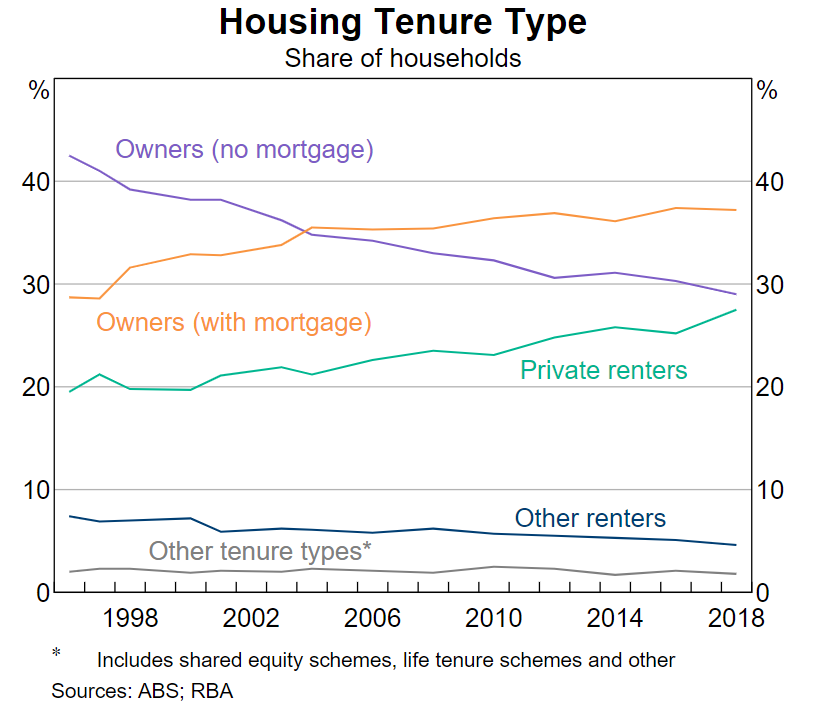

One-third of Australian households rent, mostly in the private rental market (Graph 1). Renters tend to be younger than owners, with close to two-thirds of households headed by someone under the age of 35 renting. Renters also tend to have lower incomes and spend a larger share of their disposable income on housing costs compared with owner-occupied households (both outright owners and those with a mortgage).

The full text of this article is available to MacroBusiness subscribers

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.