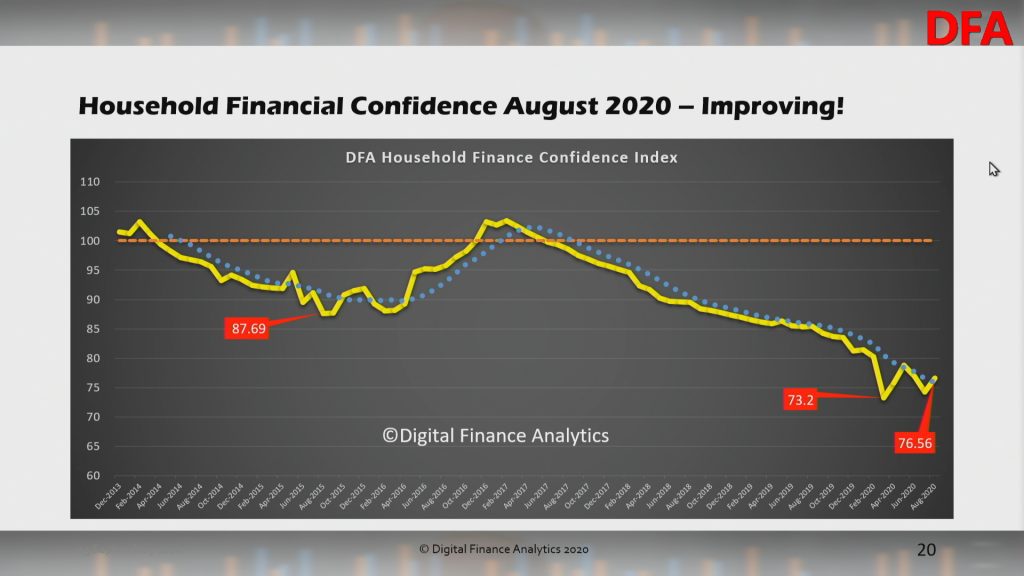

We have released the latest edition of confidence measures based on our surveys. The overall index recovered a little in August, but remains well below the 100 neutral setting at 76.56.

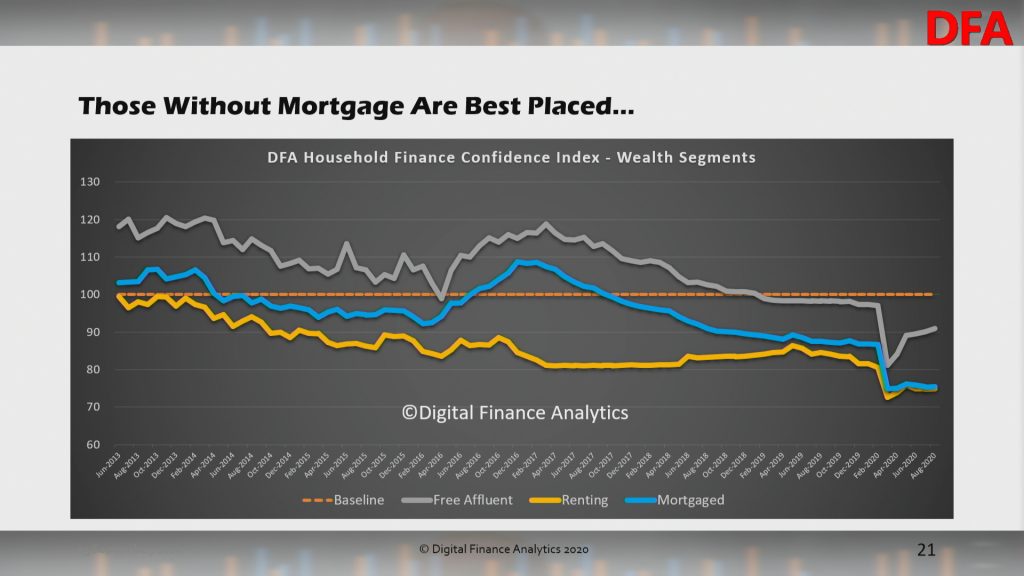

Within the cohorts, more affluent and mortgage free households are best placed, thanks to continued strength in stock markets. Those with mortgages and those renting, not so much. The massive levels of Government support, plus repayment holidays also helped, together with significant superannuation withdrawals.

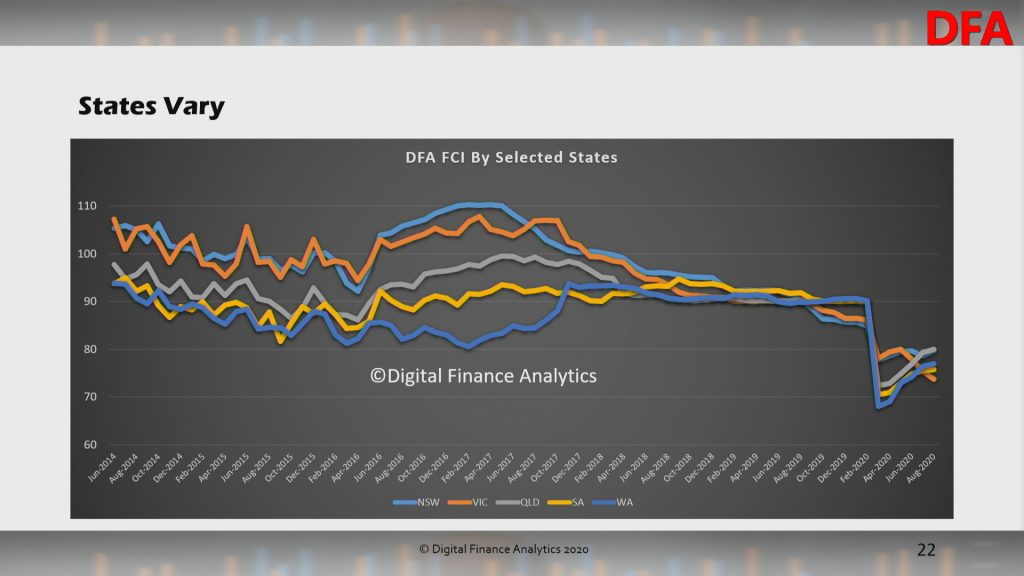

The state variations are striking, with a further fall in Melbourne in response to the latest lock-downs, while WA is looking stronger.

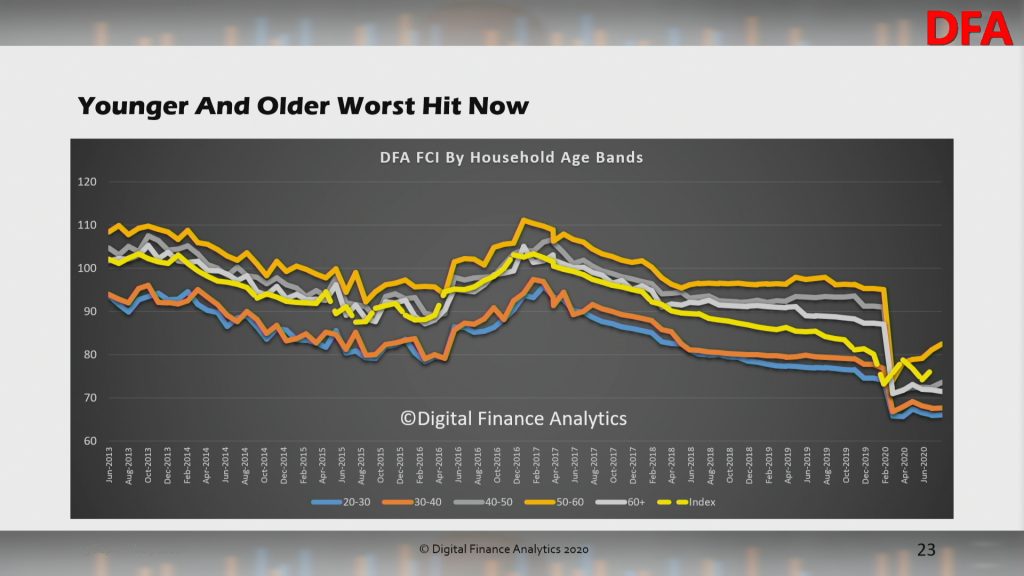

Across the age groups, younger and older households are more exposed, while late middle aged households, who have more financial resources, and less mortgage debt, are more positive.

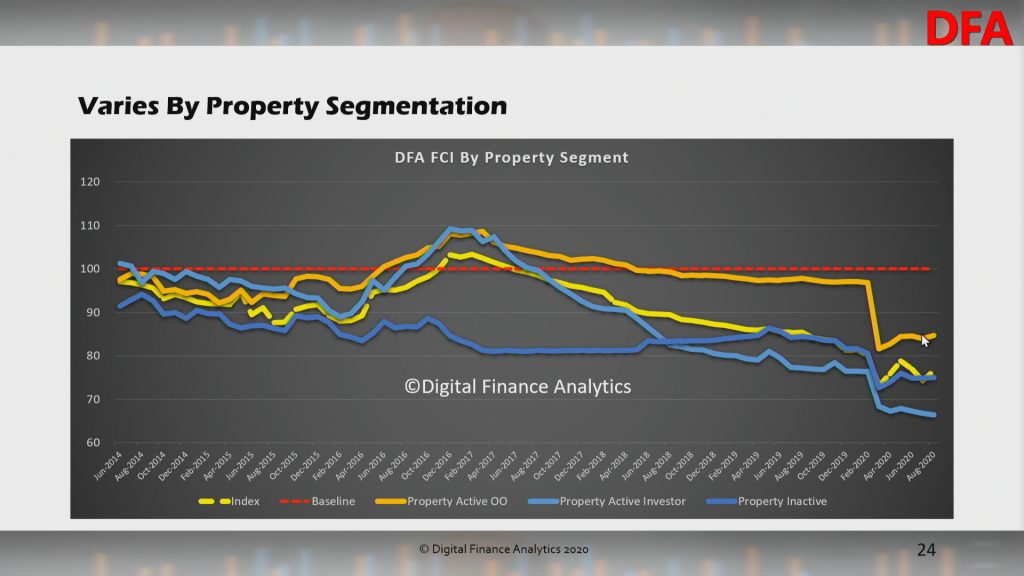

Across the property segments, owner occupied property holders are more positive relatively speaking, thanks to lower mortgage rates – this despite higher mortgage stress. However, property investors continue to wrestle with poor returns, limited capital growth, and pressure to commence repayments on mortgage balances. Many are still considering disposing of property in the months ahead. Renters are caught with more limited income, despite rents slipping in some areas. There is also concern in this cohort about the status of deferred rentals down the track.

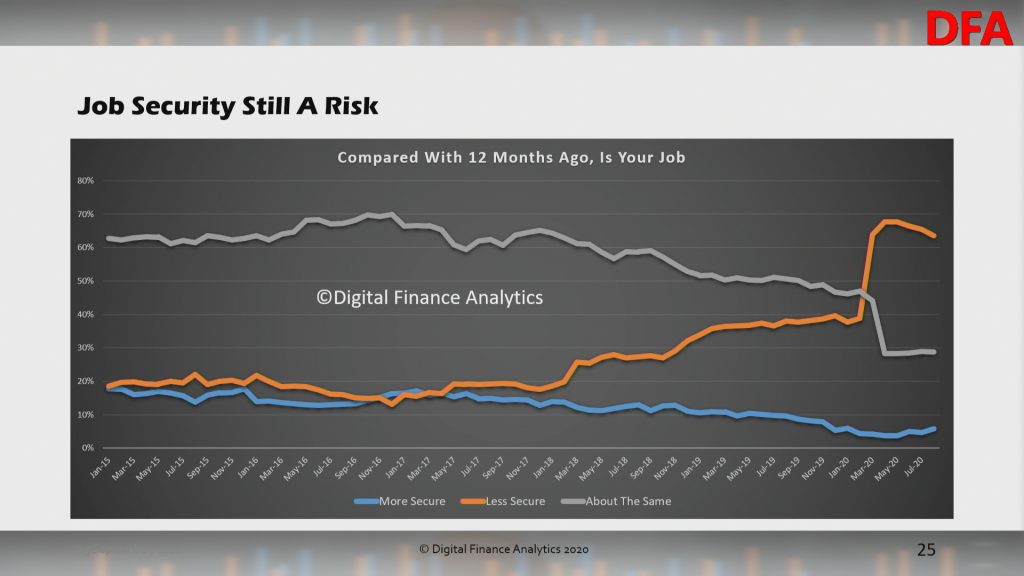

Within the moving parts of the index, job security remains a significant issue, though there was a slight easing in some areas, while in Melbourne things have degraded significantly. Many self-employed households are under severe pressure, with up to one in three concerned about the future of their business.

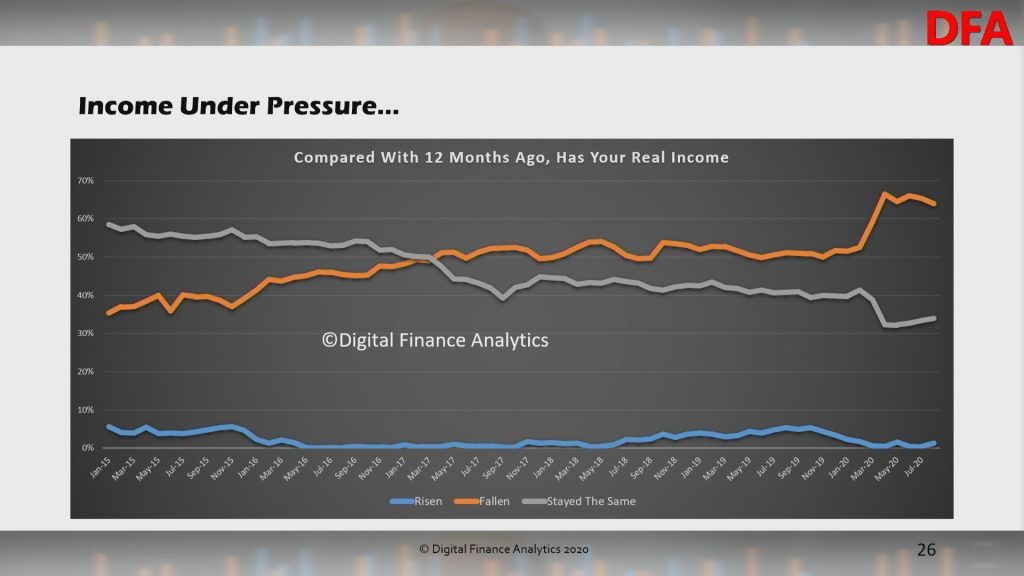

Income pressures remain to the fore, despite JobKeeper and JobSeeker. Some households have received higher incomes, though these will be reducing in September. Others have received no support despite income compression. The majority suggest real incomes have declined in the past year.

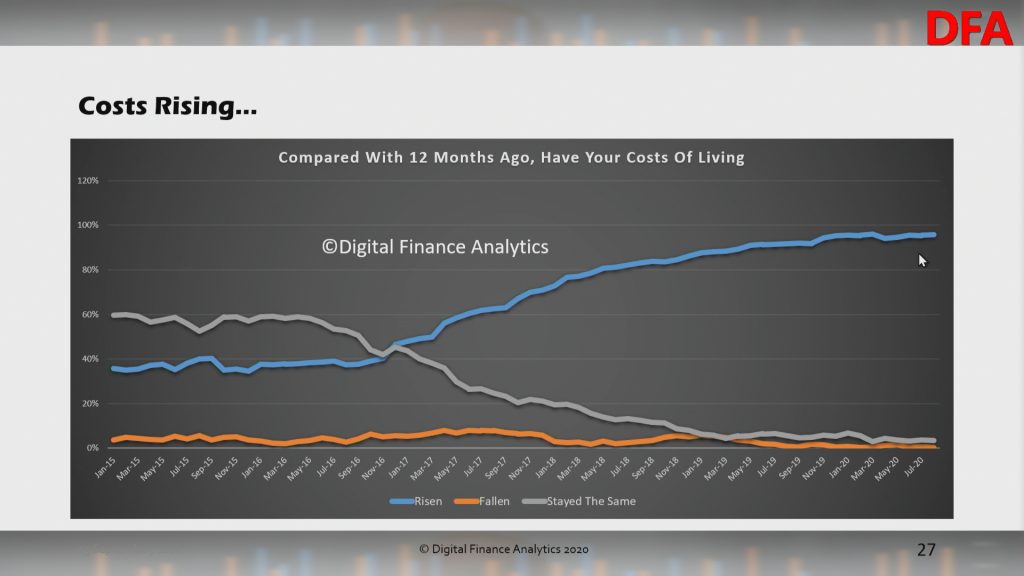

Costs of living continue to run above the official CPI figures. Food staples appears to be rising quite fast, despite lower spending by some households on transport and petrol. School fees and health care costs also figure.

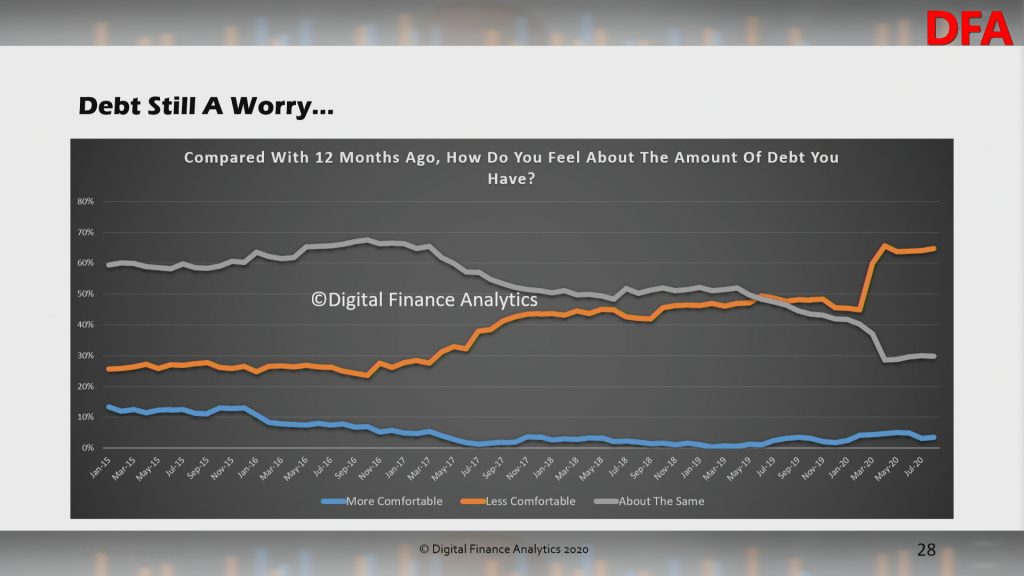

Households are under considerable debt pressure despite the current repayment holidays. Given income pressures, meeting future debt commitments registered as a significant risk. This is consistent with high levels of mortgage and rental stress.

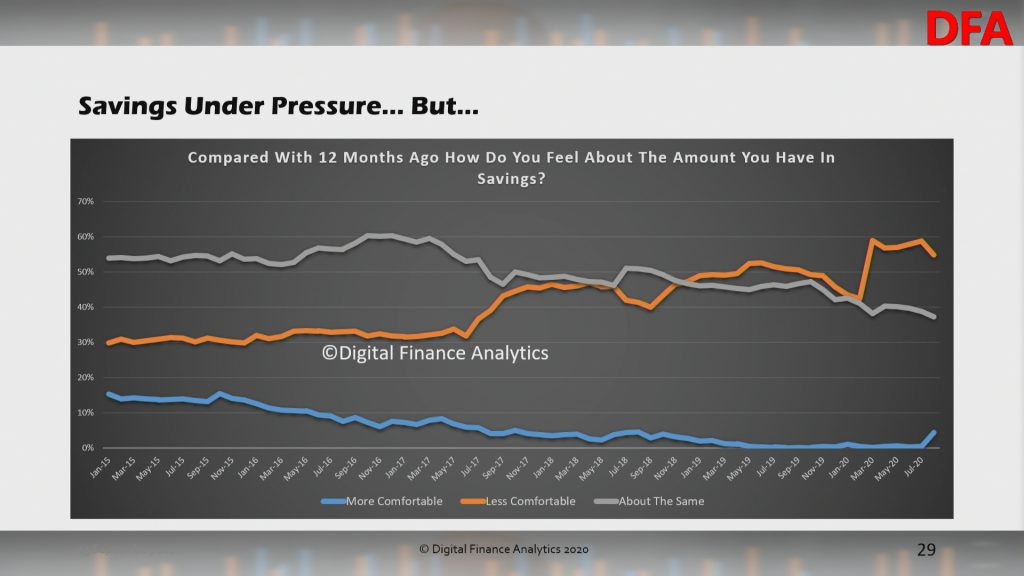

On the other hand, those receiving additional support, pulling money from superannuation, or repayment holidays are saving hard, as a hedge against future uncertainty. That said, many Australians reliant on income from bank savings continue to see their ability to service debt crushed by close to zero returns on deposits. Buy Now Pay Later facilities are in vogue to spread the costs of purchases, and as a way to manage cash flow. About 20% of users end up paying late costs, making this “free” credit expensive.

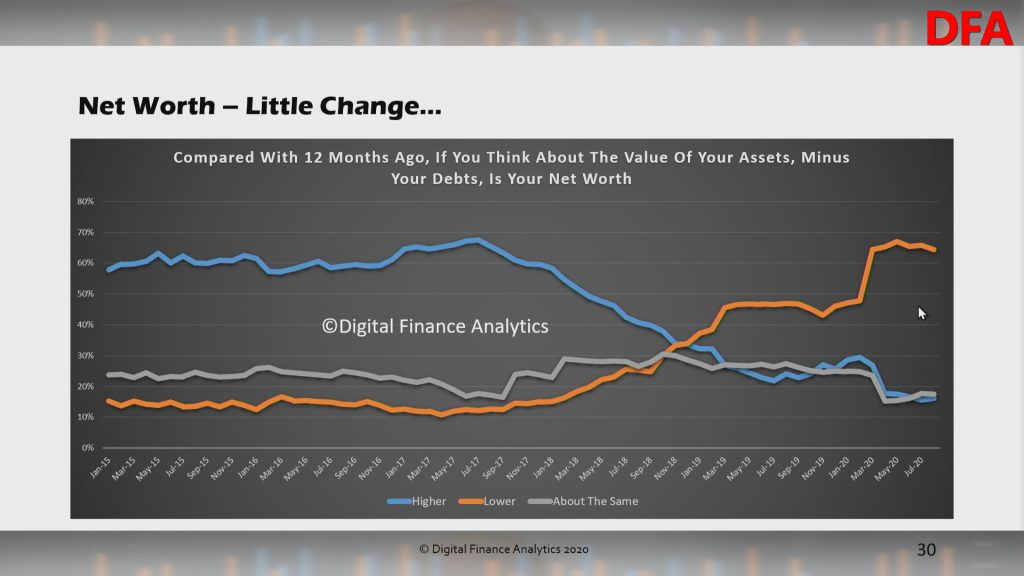

Finally, net worth remained relatively static as the elements in the index shifted. There is considerable confusion in the minds of many households who hold property, given the mixed data available about the property market. Many still believe the Government will stop home prices falling. Nevertheless, households remain cautious ahead of the impending cuts in support, and this does not bode well for greater consumption ahead. The major pain point is small businesses, may of whom have not been able to benefit from JobKeeper. This should be a focus for the Government in the upcoming budget.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.