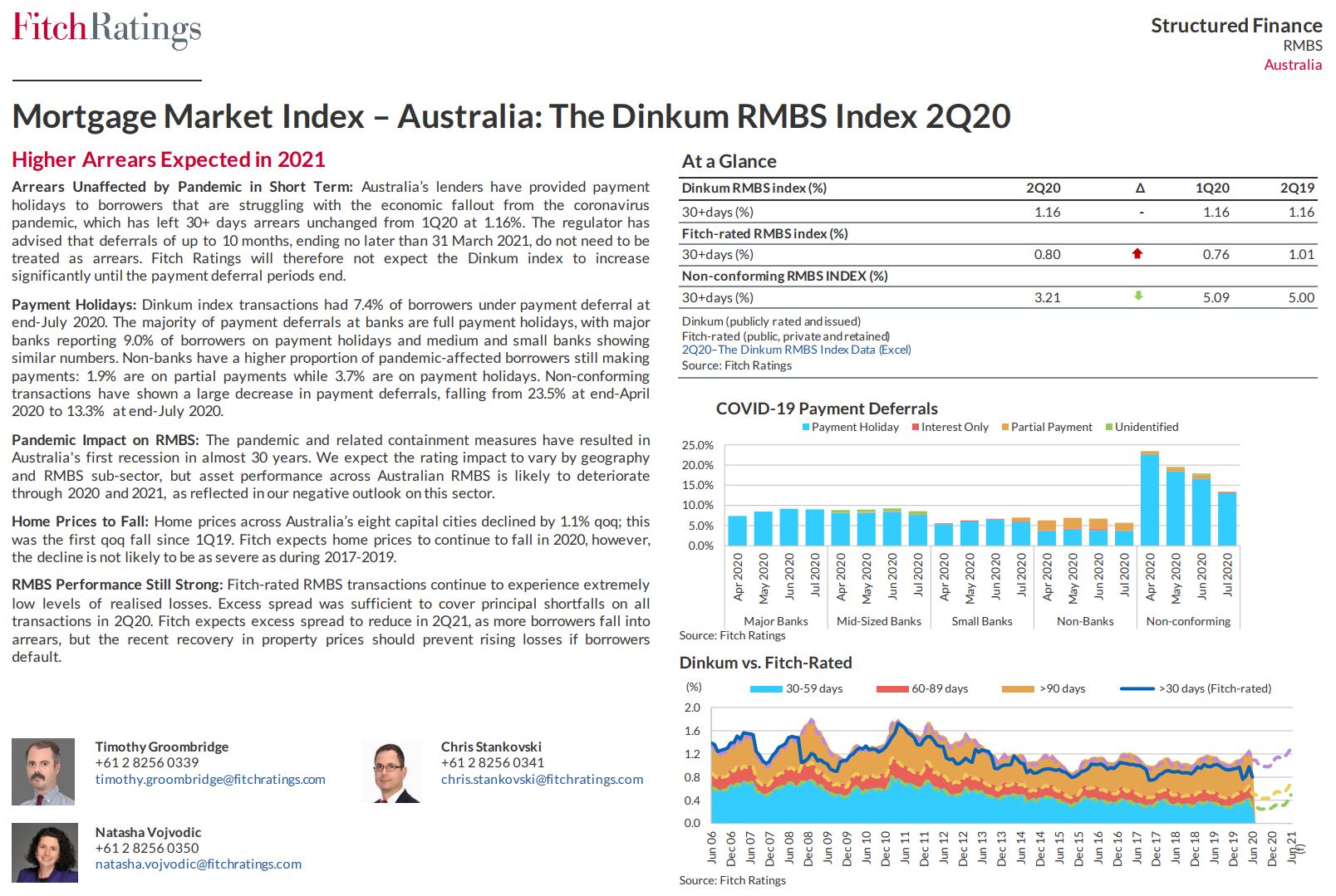

The Dinkum Index from Fitch:

Fake, of course. Arrears are all piled into forbearance loans. Via Banking Day:

APRA has made further regulatory adjustments to the capital treatment of loans to customers affected by COVID-19.

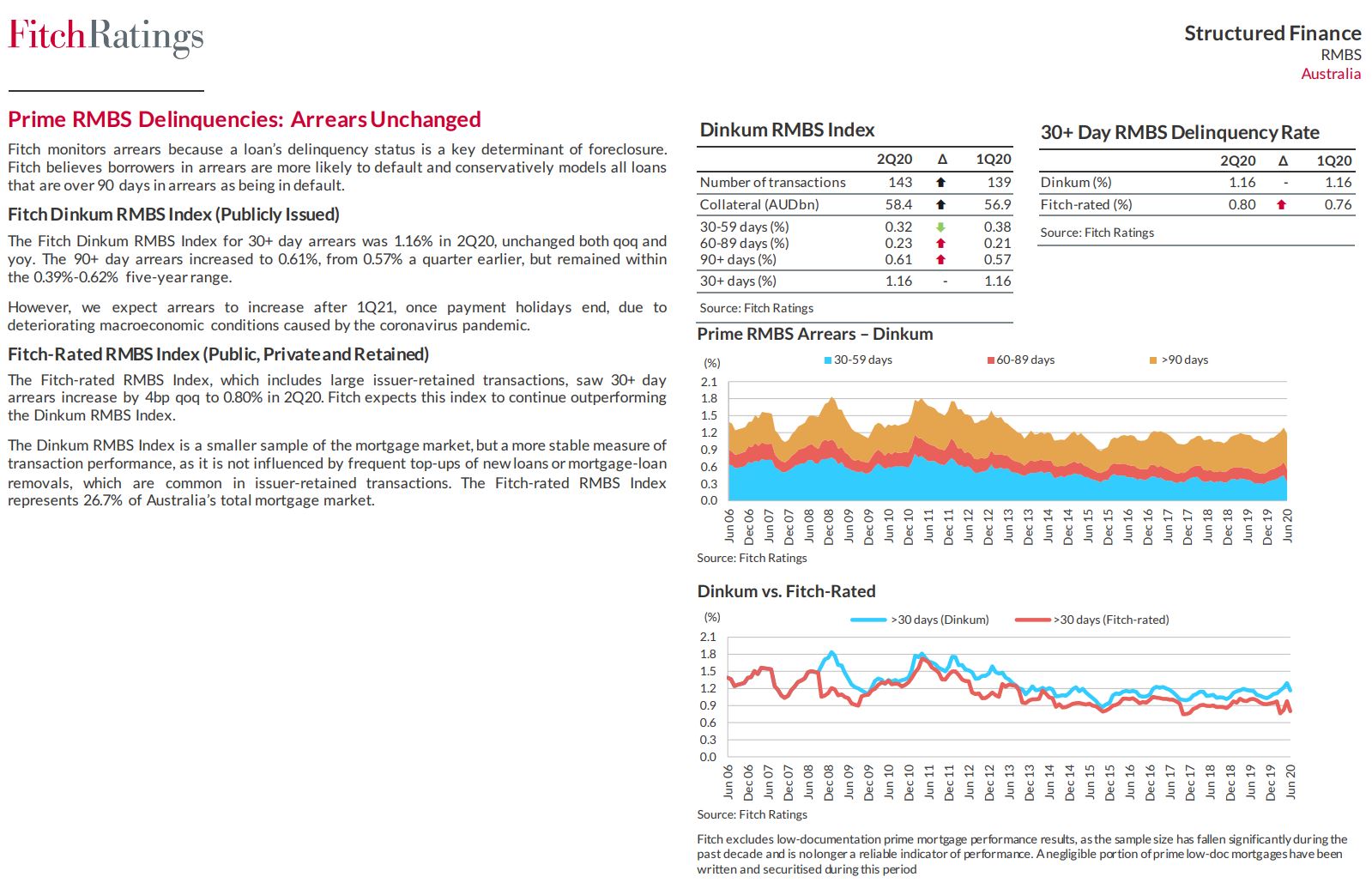

The Dinkum Index from Fitch:

Fake, of course. Arrears are all piled into forbearance loans. Via Banking Day:

APRA has made further regulatory adjustments to the capital treatment of loans to customers affected by COVID-19.

The full text of this article is available to MacroBusiness subscribers