Markets took a tumble last week, is this the start of the end? It could well be. Markets certainly looked like they were in the final stages of a blow-off top over the last week or two with fewer and fewer stocks driving the gains and technical issues in options markets driving stocks higher. Maybe the Millenial stock jockeys will draw down further on their credit cards to buy more options and give the stock market another leg higher. Regardless, the violent up and down moves suggest we are closer to the top than the bottom.

Your super fund probably isn’t doing anything about it

The question for anyone with super is to work out whether your superannuation fund is managing the volatility or is just a cork tossed into the ocean.

There are a lot of superannuation funds who espouse risk management and asset allocation but don’t do much about it in practice. Asset allocation is widely acknowledged to be the key driver of returns. Most super funds have fixed asset allocation that doesn’t change.

These super funds allocate between equities, bonds, unlisted assets and cash based on how old you are and your risk profile.

- Stock markets at close to all-time valuation highs? Have a 70% exposure.

- Equities have fallen and are at attractive lows? Have a 70% exposure.

- Somewhere in-between? Have a 70% exposure.

These funds are passengers in the market. Content to let the market take them where it may.

Super fund transparency

Newer super funds run Separately Managed Accounts (we run ours like this), so that investors can tell exactly how their super is invested, down to the individual stock.

The other big risk is with the older style superannuation funds is that you just don’t know what you own. You could have lots of equities, you might have hardly any. Good luck finding out.

A telling comment

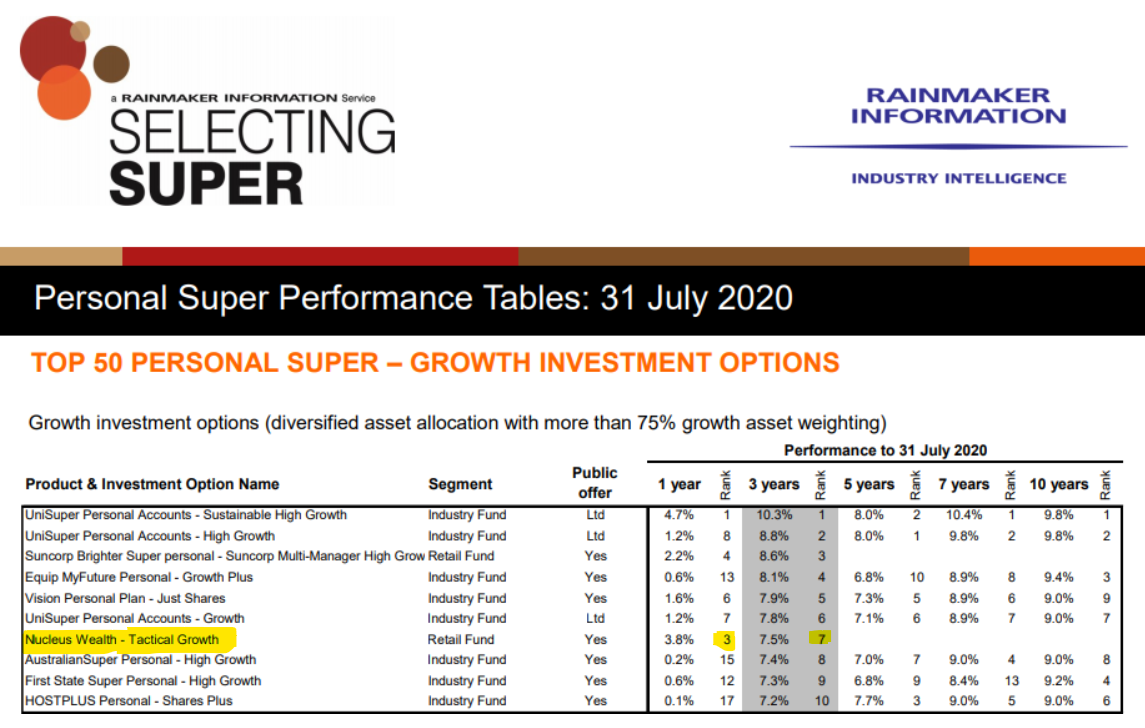

MBFund is a relatively new super fund, with three years’ performance history, putting us clearly in the top ten funds in Australia.

We have a rating from several research houses. However, the response of one prominent research house that won’t rate us (yet!) was particularly telling about the state of the industry:

- We can’t put you in our survey as you are not like other super funds.

- If markets are expensive or risky, you underweight growth assets. Most others keep very constant allocations.

- Also, you invest directly in the underlying stocks and bonds. Most give the money to someone else to manage.

What is your super fund doing?

Most superannuation funds are going to simply bomb your money into the market with no regard to valuation.

For these funds, when ASIC tells you that fees are the most important thing, they are right! If asset allocation is fixed, and these funds invest in a range of similar fund managers, then the returns will be basically the same except for the fees.

Picking the superannuation fund manager who picks the asset consultant who picks the fund managers

There is some skill in picking investment managers. It is a hard skill though, and determining the difference between skill and luck is difficult. Many superannuation funds outsource this to experts like Mercer or Willis Towers Watson.

Normal investors in typical superannuation funds have an added layer of difficulty. You are trying to choose the right superannuation fund manager who has chosen the employee that has chosen the right asset consultant that is good at picking investment managers who are good at picking stocks. There are a few links in that chain.

Some superannuation funds try to get around this by picking a lot of managers. The problem then is that if you pay 1% to 7 different fund managers to pick stocks for you, and they all buy different stocks, then you end up with a portfolio that is effectively the same as the market but you are paying higher fees for it. You could just buy an index fund for cheaper.

The other skill is blending managers. If the manager you have picking stocks is a bear and your bond manager is a bull, you might end up underperforming whatever happens!

The sneaky way to outperformance

An underhanded way is to buy higher-risk assets and call them low-risk assets, usually because they are in an unlisted structure. That way you can call yourself a lower-risk fund but outperform over the long term because you are buying higher-risk assets than everyone else you are being compared to.

Now not all funds are like this. But enough of them are to be wary.

Moral of the superannuation story

If you are invested with a typical fund, it probably has a fixed asset allocation. So, don’t expect them to take steps to preserve your capital and rotate out of expensive markets.

Some superannuation funds will look to drive performance by risk management and asset allocation, many are just along for the ride.

————————————————-

Damien Klassen is Head of Investments at the Macrobusiness Fund, which is powered by Nucleus Wealth.

Follow @DamienKlassen on Twitter or Linked In

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Nucleus Advice Pty Ltd – AFSL 515796.