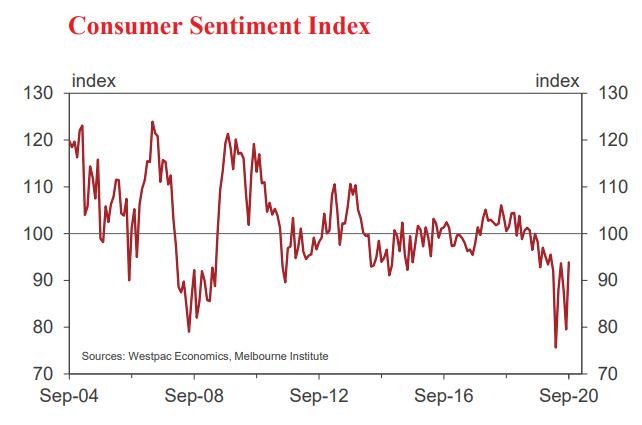

We suspected last month’s 9.5% collapse in the Index was an over-reaction but this month’s 18% rebound is a pleasant surprise nonetheless. It comes despite official confirmation in the survey week that Australia had experienced its first recession since 1992. Clearly this was ‘old news’ with respondents more focussed on the future.

The rebound means the Index is now just 1.6% below the average over the six months prior to the emergence of COVID-19 in March.

Recall that the sharp fall in August was in reaction to the deteriorating virus situation in Victoria which had seen the state government announce hard lockdown measures at the start of the month including ‘Stage 4’ restrictions for Melbourne. But the more concerning message in August was the weakness in other states – in particular, the 15.5% slump in confidence in NSW.

The state had seen persistent clusters of virus cases and combined with Victoria’s problems, sparked concerns of a wider ‘second wave’ outbreak. To a lesser extent these fears were also apparent in Queensland where confidence tumbled 8.1%.

However, Victoria’s new cases slowed markedly once lockdown measures were in place and we saw no evidence of second waves in either NSW or Queensland.

It should be noted that the September survey was completed before the announcement by Victorian State Premier Andrews on September 6 of a slower than generally expected move towards reopening. The disappointment with that announcement could have been expected to dampen the 14.9% surge in confidence in Victoria, although frustration at the extended lockdown measures would likely still be more than outweighed by the clear success they have had in containing the virus.

We do not expect the Premier’s announcement would have had any impact on the positive results in other states.

The best way to assess the September sentiment results is by comparing them with the results in June, when states were in the process of reopening and Victoria’s second wave problems had not yet emerged. The Index nationally was at 93.7 in June. On a state basis confidence is back at its June level in NSW; 5.6% below its June level in Victoria; 2% above in Queensland; 11.2% above in Western Australia and 3.8% above in South Australia.

The impact of the Commonwealth Government’s fiscal support measures targeting households is apparent in the components of the Index. Assessments of family finances are upbeat relative to a year ago whereas the economic outlook and assessment of spending conditions are still significantly weaker. The mix strongly echoes the detail from the June quarter national accounts which showed the wider economy experiencing a sharp recession but household incomes rising in the quarter, largely due to fiscal supports.

The ‘finances vs a year ago’ sub-index lifted by 11.2% to be 3.7% higher than this time last year. The ‘finances, next 12 months’ sub-index lifted by 11.2% to be 4.5% above the level in September 2019.

On the other hand, there is still extreme nervousness about the near term economic outlook. The ‘economy, next 12 months’ sub-index increased 41% but is still 18% below its level a year ago while the ‘economy, next 5 years’ sub-index rebounded strongly from last month’s collapse, to be up 19% over the month and 2% above the level last September.

The ‘time to buy a major household item’ sub-index lifted by 16.3% but is still 12.1% below the levels of a year ago.

Every quarter we assess respondents’ most recalled news items and their qualitative assessment of this news.

These questions have been in place since the survey began back in the 1970s but do not include a clear category that would capture ‘health issues’ such as the Coronavirus pandemic. As such, the impact of virus-related news is only captured indirectly.

The closest ‘fit’ appears to be with news on ‘economic conditions’ which had a 42% recall – the highest proportion in nearly nine years. News on this front was still assessed as overwhelmingly unfavourable. Of some interest is the low proportion of respondents who recalled news from overseas – only 11% compared to 25% in March when Australians were anxiously watching virus developments in China; the US; and Europe.

There were some more favourable assessments of a number of other news categories including ‘Budget and taxation’; ‘interest rates’ and, most notably, ‘politics’. Indeed the latter should be welcome news for Australia’s politicians – presumably both federal and state – with an extraordinary 70% of consumers assessing political news as favourable, a

result unlike any seen in the 45 year history of the survey and further evidence of what is proving to be a very ‘strange’ recession.

We always take close interest in the Westpac Unemployment Expectations Index. Sentiment around employment prospects improved by 14.8% in September. While the general assessment of the current jobs market is still one of increasing job insecurity this measure has been telling us a more stable story. Relative to the average level of the index in the six months prior to COVID-19 the index has deteriorated by only 3.3%.

The survey always provides rich insights into the outlook for the Australian housing market.

The ‘time to buy a dwelling” index increased by 3.0% in September, also putting this component at a comparable level with June when respondents were being encouraged by the general reopening of the economy.

In fact, this index has moved on somewhat from June. The overall index is 2.7% above June; NSW is 1% above; Victoria is 2.2% above; and Queensland is 8.5% above. While the index nationally is still 6% below the average over the six months prior to COVID-19, it continues to point to stabilising conditions in the housing market.

This negative sentiment is still evident in consumers’ house price expectations. Recall that the Westpac Consumer House Price Expectations Index tumbled 51% in April in the first stages of the national lockdown. In September it lifted by 21.7% to be a solid 10.7% above the level in June but still 37% below the average level in the six months prior to COVID-19.

While house price expectations remain subdued, confidence appears to be building steadily despite recent recession announcements.

Every quarter we are interested to assess the level of risk aversion amongst respondents. Relative to a year ago ultralow interest rates have lowered the urgency to pay down debt with 17.1% of respondents nominating ‘pay down debt’ as the wisest form of saving down from 20.7%

But preferences have not moved to the ‘riskier’ investments like shares and property (property down from 11.9% to 9.9%; and shares steady around 9%).

Rather the shift in preferences, over the year, has been to bank deposits with 32.7% favouring bank deposits compared to 26.7%.

The conclusion remains that Australians continue to hold extremely risk averse preferences for their savings.

The Reserve Bank Board next meets on October 6 – the same day as the evening announcement of the Federal Budget.

At its latest meeting the Board increased its Term Funding Facilities to Authorised Deposit-taking Institutions (ADIs), by $57 billion, from $152 billion to $209 billion.

The facilities provide ADIs with funding for three years fixed at 0.25%. ADIs, including banks, may use the facilities for refinancing offshore borrowings; purchasing other securities, including government and semi government paper or lending, including for fixed rate mortgages. This enhanced liquidity can be expected to further lower rates across the spectrum.

This follows announcements from the US Federal Reserve that further monetary stimulus is likely as it effectively raises its target for inflation. I think it is reasonable to expect further initiatives from the Reserve Bank to loosen monetary policy.

That approach will be entirely appropriate as its actions complement what is set to be a stimulatory Budget. Bringing forward the July 2022 tax cuts; boosting investment allowances; further one-off payments to low income earners; and an accelerated infrastructure program can all reasonably be expected.

As we have seen in today’s survey, consumer confidence is returning to more normal levels, although the sensitivity to progress in managing the virus and the opening up of economies remains key to the outlook.

You can’t dismiss bad vol and accept good vol, Bill. The message here is the consumer has turned manic depressive as she struggles with the sheer load of debt, house prices, virus, and general chaos.

It’s a writhing ponzi system breaking under pressure.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.