The mistake of 1937 is a very useful historical guide for policymakers wrestling with an economic depression. Via the ECB:

The economic conditions can be summarized as follows: 1) There are signs that the depression is finally over. 2) Interest rates have been close to zero for years but are now finally expected to rise. 3) There are some concerns from both policymakers and the market participants over indications of excessive inflation. 4) This is of particular concern to some who point to a large expansion in the monetary base in the past several years as well as the current bank holdings of large excess reserves.

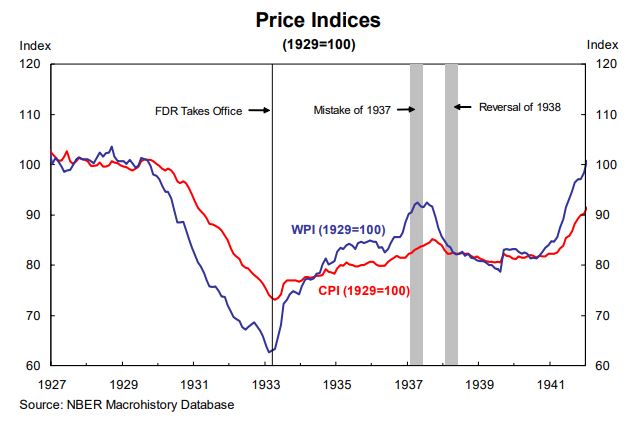

These four conditions characterize the economic outlook of the United States in the early months of 1937 at the precipice of one of the most peculiar policy mistakes in US economic history. These circumstances may sound familiar to Japanese audience. In some respects Japanese policymakers confront the same problems. How should one manage monetary policy in a transition phase from zero short-term interest rate and deflationary pressures back to more normal circumstances? We want to emphasize right from the start, however that fortunately it seems that both the Bank of Japan and the Japanese government have not committed any mistakes of the same order as observed 1937. Yet, it is useful to understand the circumstances and mechanics of the US mistake as a precautionary tale for both current and future policy makers.

This paper addresses the “mistake of 1937”, which reversed the tide of the recovery from the Great Depression in 1933-37 into a short but sharp recession from 1937-38. Between May of 1937 and June of 1938 GDP contracted by 9 percent1 and industrial production by 40 percent. The general price level took a tumble as well. The index of wholesale prices, for example, fell by more than 11 percent, several leading commodity prices collapsed and the stock market lost almost half of its value.

The mistake of 1937 was in essence a poor communications policy. At the time, President Franklin Delano Roosevelt (FDR), his administration, and the Federal Reserve all offered confusing signals about the objectives of government policy, especially as it related to their goals for inflation. These vague and confusing signals about future policy created pessimistic expectations of future growth and price inflation that fed into both an expected and an actual deflation. Nominal rigidities helped propagate these impulses into a full scale recession. We show that this propagation mechanism is particularly damaging at zero interest rates by constructing a stylized stochastic general equilibrium model in which the zero bound on short-term interest rate is binding due to temporary shocks. We simulate this model and show that at zero interest rates, both inflation and output are extremely sensitive to signals about future policy. By “extremely” we mean that if the public’s beliefs about the probability of a future regime change by only a few percentage points, there are very large effects on inflation and output. This effect is independent of any change in the current short-term interest rate, which we assume remains at zero.

In this stylized model, an example of such an effect might read as follows: Suppose the public fully believes that the government is committed to targeting 4 percent inflation. Now assume that in response to recent coverage in the press that the public thinks that there is a five percent chance that the government will change its goals of 4 percent inflation in favor of a zero inflation goal within the next two years. This small change in beliefs in our calibrated model results in double digit output collapse and deflation. The large effects of shifting public beliefs about future policy may help explain how the vague and confusing communications in 1937, which we document in some detail, had such a large negative impact.

We find that the effect of communication is highly non-linear at zero interest rates. At zero interest rates, the marginal effect of creating deflationary expectation by signaling tightening (targeting lower future inflation) is much larger than the marginal effect of signaling loosening of policy (targeting higher inflation).

Our interpretation of this finding is that if a policy maker is uncertain about the nature of the real shocks and wishes to be conservative he should err on the side of allowing some excess inflation.

The large effect of communication, and this peculiar asymmetry, is unique to an environment in which the short-term interest rate is zero. The reason is that this environment is susceptible to what we term deflationary spirals. The dynamics of the deflationary spirals are that if the public expects a more deflationary regime in the future, this expectation creates deflationary expectations in all future states of the world in which interest rate are zero (i.e. when the zero bound on the short term interest rate is binding).

Those states of the world, in turn, depend on each other and they create a vicious feedback effect that may not even converge to a bounded solution (for some parameter values) in the approximated solution of our model.

Because our theory relies on shifting public beliefs about future policy, a natural place to look for evidence for the theory is within the newspapers in 1937-38. In the next subsection we document several narrative newspaper accounts that are consistent with our hypothesis. In addition we construct a new index based on newspaper records which summarizes the intensity of communication policy at a given time. We find evidence of an increase in policy communcation in the months we identify with the mistake of 1937.

Transpose this analogy onto today’s circumstances. The virus is not beaten. Borders will remain shut. Further outbreaks will entail curbs on activity.

Advertisement

Yet the wider conversation has tuned to booming house prices. Rebounding jobs markets. Reopening economies. Treasurer Depressionberg is about to unleash stunning fiscal austerity while pretending he’s boosting spending, via Domain:

A deficit well beyond $200 billion is now expected, dwarfing the previous record of $54.5 billion set by the Rudd government during the depths of the global financial crisis in 2009-10.

One senior member of the government, speaking on condition of anonymity, said the size of the spending to be revealed in the October 6 budget would shock many observers, describing it as an “astounding” injection of assistance into the economy.

Some of the spending will be due to the government bringing forward its already legislated personal income tax cuts. Just pulling forward tax changes due to start in mid-2022, which includes taking the top threshold for the 32.5 per cent tax rate to $120,000 from $90,000, would cost the budget more than $14 billion over two years.

The $680 million HomeBuilder program, which ends on December 31, is being considered for extension over fears the employment-heavy construction sector will start to run out of new work by the middle of next year.

…Federal Education Minister Dan Tehan will today announce a “recovery payment” worth 25 per cent of pre-COVID revenue for child care services in Victoria that will be available until January 31 next year.

…The budget will contain extra infrastructure spending, spread across the entire country including tourist-dependent regions which have been heavily affected by the closure of the international border.

Reserve Bank deputy governor Guy Debelle is expected to give an upbeat assessment of the economic recovery on Tuesday after the fourth major bank forecast an end to the COVID-19 recession and Prime Minister Scott Morrison said hundreds of thousands of new jobs would be created before Christmas.

Dr Debelle will also be called upon to provide details about possible plans to remove the central bank’s committed liquidity facility (CLF) – a scheme devised to provide commercial banks with short-term liquidity in times when there is tighter supply of government bonds.

In a speech titled The Australian Economy and Monetary Policy, to be given to the Australian Industry Group, Dr Debelle is expected to highlight last week’s extraordinary employment turnaround – which showed the biggest monthly fall in the jobless rate in 32 years – and whether that could indicate the end of the recession.

The bullshit turnaround it should read.

There’s mixed message across the board. Radical tightening/loosening of fiscal support. Radical tightening/loosening of monetary support. Booms and busts in wages, inflation and assets all around.

Aussie’s are about be smacked by tightening conditions amid the worst economy since 1930, that the ABS claims is driving booming employment, as the health emergency bubbles away, most of the nation’s borders remain shut, and all with interest rates at zero.

Advertisement

Does anyone really see a consistent and reliable narrative and plan here to lift confidence, lower savings, boost spending and increase investment? If you do then please tell us what drug you’re taking so we can all have some.

Dumb and Dumber are heading into the mistake of 2021.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.