Below find a full review of this week’s China data. Apologies for the lateness. Had some “issues”.

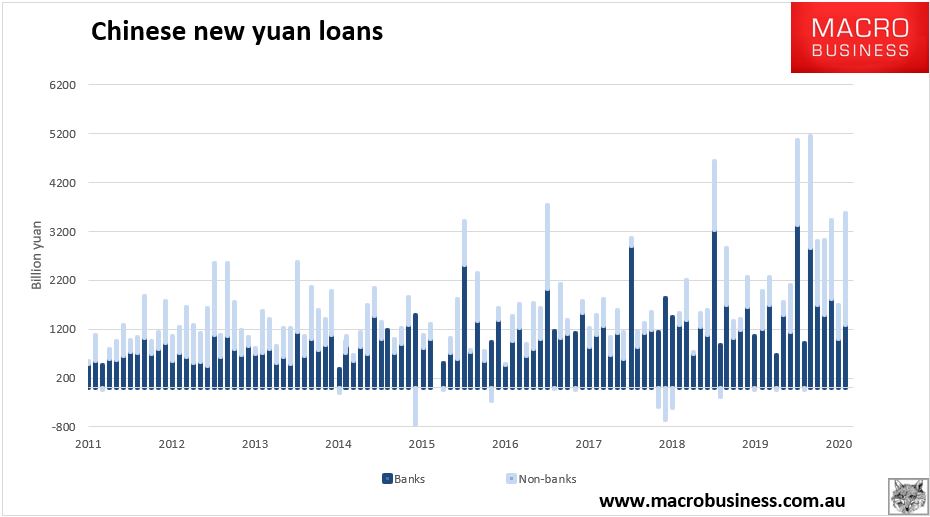

First out was August credit which has had its ears pinned back with TSF at an impressive 3.58tr yuan. Banks made up a lousy 1.2tr of that:

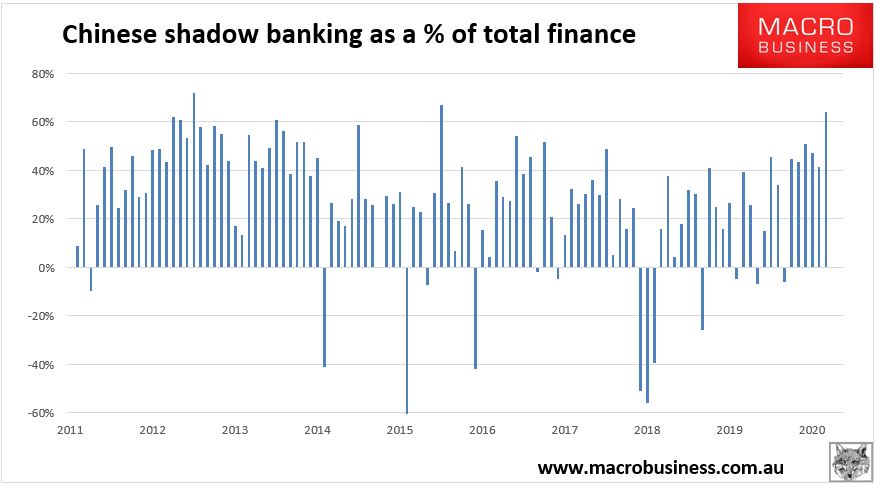

Meaning that shadow finance is roaring ahead again, though this now contains local government bonds so is not a fair label any more:

Advertisement