From Gareth Aird, head of Australian economics at CBA:

We expect the RBA to leave monetary policy unchanged at the October Board meeting.

We expect the targets for the cash rate and the yield on 3-year Australian Commonwealth Government Bonds (ACGBs) to be maintained at25 basis points.

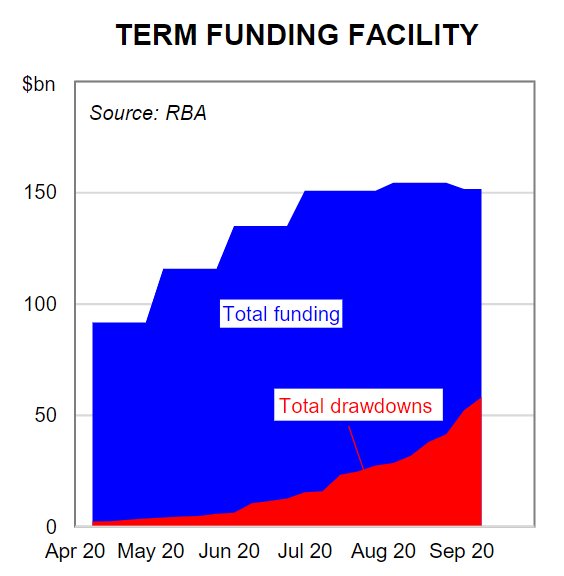

Further near term monetary policy support for the Australian economy is expected to come through an increase in government bond purchases. More changes to the Term Funding Facility (TFF) could also occur.

It’s been a big week in Australian financial markets. The speech RBA Deputy Governor Debelle delivered on the Australian Economy and Monetary Policy has had a significant impact on money markets. Debelle presented an update on the economic impact of the pandemic as well as an assessment of the effects of monetary policy actions. Most importantly for financial markets there was a discussion on ‘other’ options for monetary policy.

The speech has caused a number of analysts to revise their views on the near term outlook for monetary policy. Several analysts now expect policy easing at the October Board meeting that involves a reduction in key interest rates. Indeed financial markets are pricing in a broadly 60% chance that the RBA cuts the cash rate. And the current 0.2% yield on the 3-year Australian Commonwealth Government Bond (ACGB) could be interpreted as implying a 33% chance that the 3-year yield curve target is dropped to 0.10%. So the meeting is clearly ‘live’.

It is our assessment that there has been an overreaction to the content of Debelle’s speech. And we do not look at the speech in isolation, but rather overlay it with other recent communication from the RBA Governor and policy decisions from the RBA.

We do not expect the RBA to cut the cash rate and other key rates at the October Board meeting. We believe the RBA will be acutely aware that the potential costs and risks of doing so at this juncture outweigh the potential benefits. The RBA has been adamant that negative rates are ‘extraordinary unlikely’. And they have generally implied that the costs outweigh the benefits. But tinkering with the cash rate in a very fine corridor between approx. 0.0% and 0.25% carries the risk of other important short-term rates falling into negative territory.

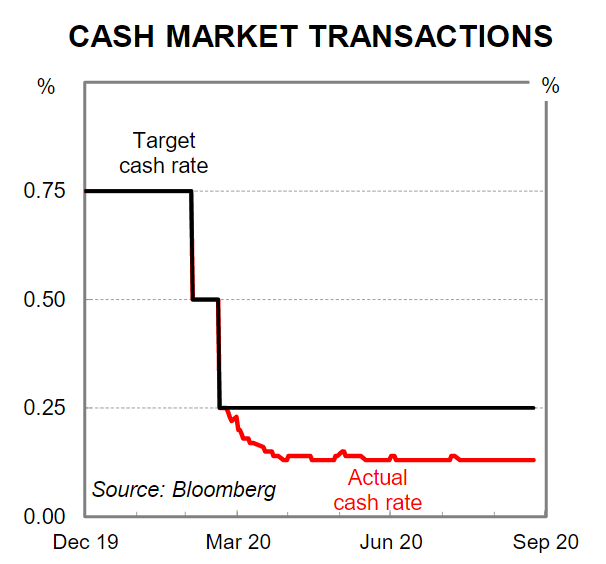

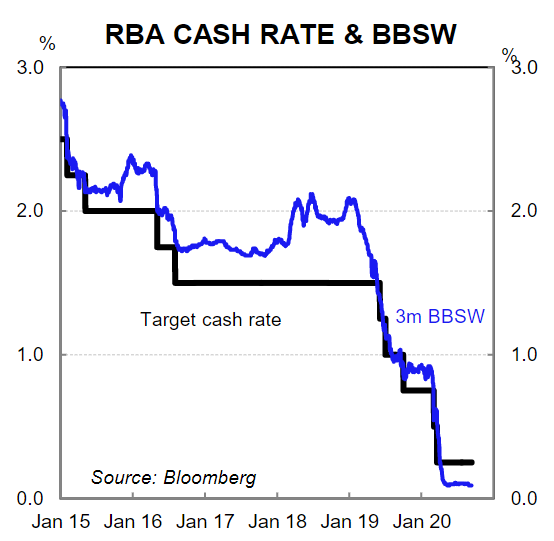

The cash rate target is 0.25%. According to the RBA this is the effective lower bound (ELB). It is also the rate at which banks can borrow from the RBA using the Term Funding Facility (TFF), and of course the yield target for the ACGB 3-year yield. But the traded cash rate sits below the target at 0.13%-0.14% because of the abundance of liquidity in the system and the fact the RBA pays 0.10% on retail bank’s cash balances held at the Reserve (known as Exchange Settlement accounts or ES accounts).

One month and three month Bank Bill Swap Rates (BBSW) sit even lower at 0.08% to 0.09%. To have a material impact on the traded cash rate the RBA would likely need to drop the cash rate target below the current traded cash rate –to say 0.10%. The RBA would also need to reduce the interest rate paid on ES balances which is currently 0.10%. Conceivably they could take the interest rate paid on ES balances down to 0.01%. But making these adjustments carries the risk that BBSW goes below 0.0%, ie. trades into negative territory. Given everything the RBA has said to date on negative interest rates, we think the risk of BBSW turning negative will be a clear deterrent in shaving key interest rates from here.

Indeed Governor Lowe spoke on this subject at the House of Representatives Standing Committee on Economics on 14 August. More specifically he stated, “we are prepared to do more if we think that doing more would get extra traction. Judgement at the moment is that, given the nature of the problems the country faces, us moving interest rates by five or ten basis points isn’t really going to make a material difference. There’s not going to be much traction from that; the problems are elsewhere.” We agree. And we do not think that the RBA will have changed their assessment of this so soon after Governor Lowe made these remarks.

Other things to consider

– The RBA increased the size of the TFF at the September Board meeting and made the facility available to June 2021. The RBA considered this, “a further easing in the stance of monetary policy”. The economic outlook has not changed in any material way over recent weeks that would constitute an easing of monetary policy over back-to-back meetings. Indeed we think that the outlook has improved and we recently upwardly revised our profile for GDP. We expect the RBA will upgrade their profile for GDP and employment in the November Statement on Monetary Policy(SMP).

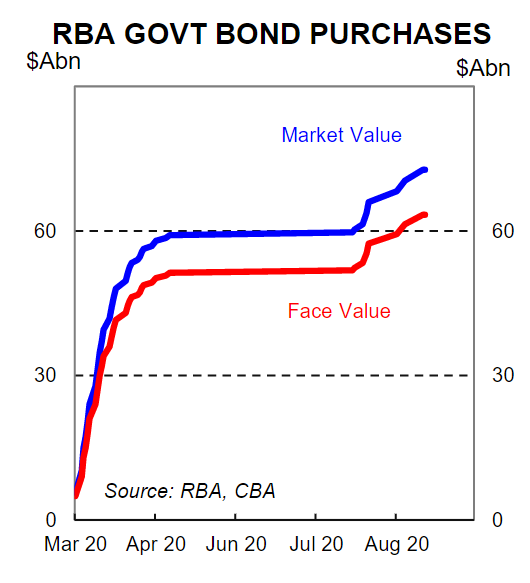

– The RBA has the capacity to ease financial conditions through more aggressive government bond buying without having to change their monetary policy stance. Their policy framework is already set up to allow them to inject more liquidity into the system through government bond buying. They can ramp up their purchases of both Commonwealth and State bonds, which could push yields lower and exert some mild downward pressure on the exchange rate thus delivering a loosening in financial conditions without cutting rates. In addition it would be consistent with Governor Lowe’s calls for the public sector to continue to deliver more infrastructure. And it would provide key support to very large government borrowing programs.

– Confidence is very important. There has recently been an encouraging lift in consumer confidence. We think that making adjustments with interest rates at these very low levels carries the risk of undermining the recent improvement in confidence. This is something that we believe the RBA will be cognisant of when weighing up the various options it has at its disposal.

– The housing market has held up very well over the Covid period and dwelling price falls have been minor. New lending has increased over the past three months and mortgage rates sit below rental yields in most markets. The housing market, which is one of the most interest rate sensitive parts of the economy, is not in need of further rate support.

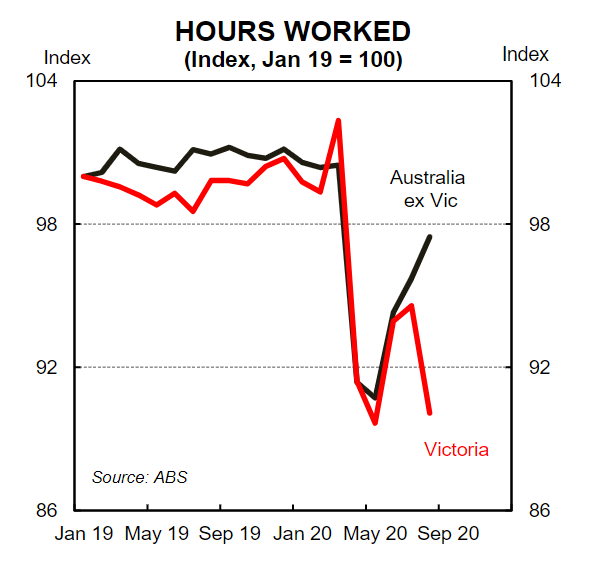

– Around five millions residents of Victoria have been in lockdown for the past ten weeks. If there was a case to tinker with the current interest rate structure for a questionable marginal benefit it was surely when Victoria entered lockdown, not when it’s on the cusp of exiting lockdown.

At this stage we believe an increase in the rate of government bond purchases is the most likely next step from the RBA on the monetary policy front. We believe the RBA will not introduce new policy options until the current actions have been expanded. That leads us to conclude that monetary policy is on hold in October.

All up, Tuesday 6 October is shaping up as an incredibly important day on the Australian economic calendar. The RBA Governor will deliver the monetary policy decision at 2.30pm (AEST).And in the evening at 7.30pm (AEST) the Federal Treasurer will hand down the 2020/21 Commonwealth Budget. It is our expectation that the main event on the day will be the Commonwealth Budget.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.