Gareth Aird, head of Australian economics at CBA, forecasts that Australia’s Q2 GDP will contract by 5.4% when the ABS reports tomorrow:

Key Points:

We expect Q220 real GDP to contract by 5.4%.

Annual growth, revisions aside, should drop to -4.7%.

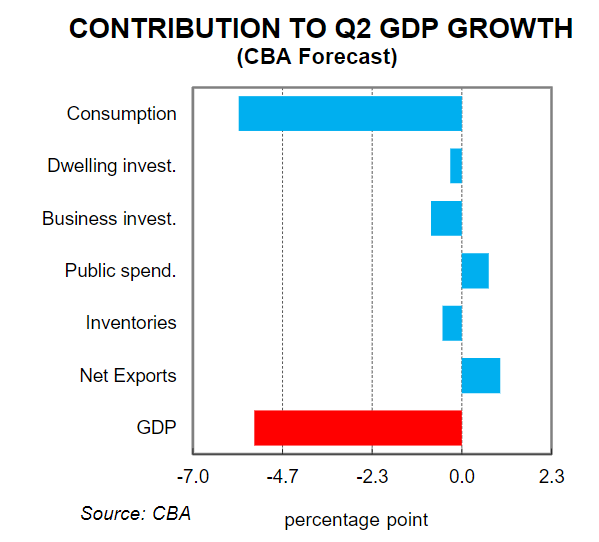

Household consumption will fall sharply while dwelling investment and business investment will also post declines.

Public spending and net exports will make solid positive contributions to growth.

We expect nominal GDP to also contract by 5.4%which would see annual growth fall to -3.8%.

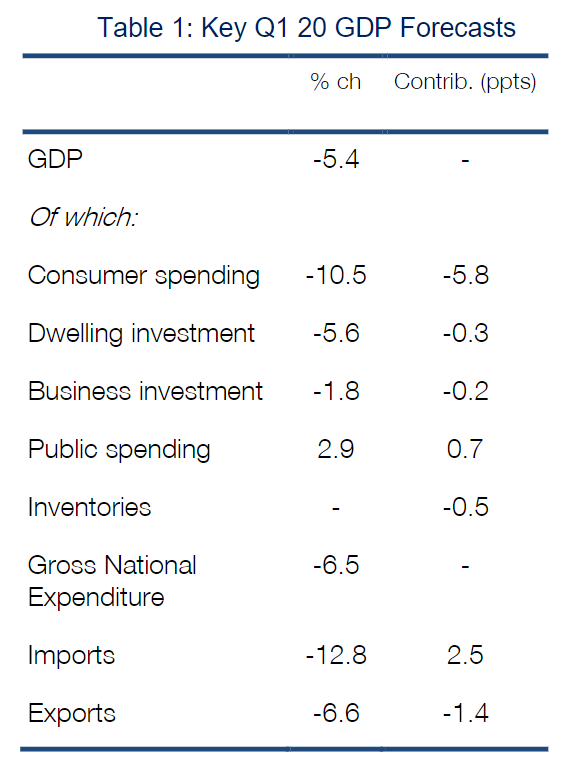

The Q2 20 national accounts will be one for the history books. The COVID-19 pandemic and resultant moves from policymakers to shut down large parts of the Australian economy will have a massive negative impact on production in the June quarter. On our estimates real GDP contracted by -5.4% in Q2 20. Such an outcome would be by far the biggest quarterly fall in GDP according to the ABS records which date back to 1959.

The components of GDP are likely to indicate that the contraction in output was limited to the domestic private sector. Public demand and the external sector contributed materially to growth (see Table 1). In summary, the data for Q220 is expected to show:

–a huge fall in household consumption: CBA(f) –10.5%;

–a chunky fall in residential construction because of a decline in new construction and alterations & additions: CBA(f) –5.6%;

–a modest fall in business investment: CBA(f) –1.8%;

–strong growth in public demand because of a lift in both recurrent expenditure and capital investment CBA(f) +2.9%;

–a rundown in inventories which will subtract 0.5ppts from growth

–a solid 1.0ppt positive contribution to growth from net exports.

The broadly unchanged terms of trade over Q2 will have a negligible impact on nominal GDP which will be weighed down by disinflationary forces (recall that Q2 CPI was -1.9%/qtr). We have the GDP deflator flat in Q2 which means we expect a quarterly fall in nominal GDP of 5.4% which would see annual growth drop to-3.8%. The drop in nominal GDP is weighing on the revenue side of the Commonwealth budget.

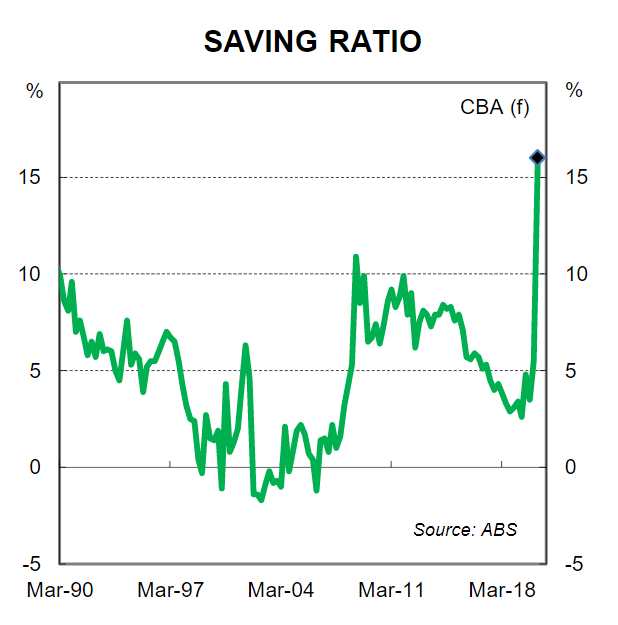

The household income account will be particularly important in Wednesday’s national accounts. Very early on in the pandemic we were able to identify, using our internal data, that a positive income shock to the household sector was underway. Government stimulus was more than offsetting the decline in wages and salaries. The household income account will have a complete update on what happened to household income over Q2 20. Combining both income and spending data over the savings rate to spike to a whopping 16% in Q2 20.

The forecasts in the RBA August Statement on Monetary Policy (SMP) imply a contraction in Q2 GDP of -6.7%. So an outcome in line with our forecast would be better than the RBA has anticipated. Notwithstanding, we do not expect any policy implications from the Q2 20 GDP outcome tomorrow.

Overall the Q2 20 national accounts will be a clear reminder that shutting down large parts of the economy has a profound negative impact on economic activity and production. Fiscal transfers to the household sector can cushion household income for a finite period of time. But for the long term health of the economy it is necessary that production rises and that we are on a path towards full employment as soon as possible. It is also important that the journey back to full employment is not a long one.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.