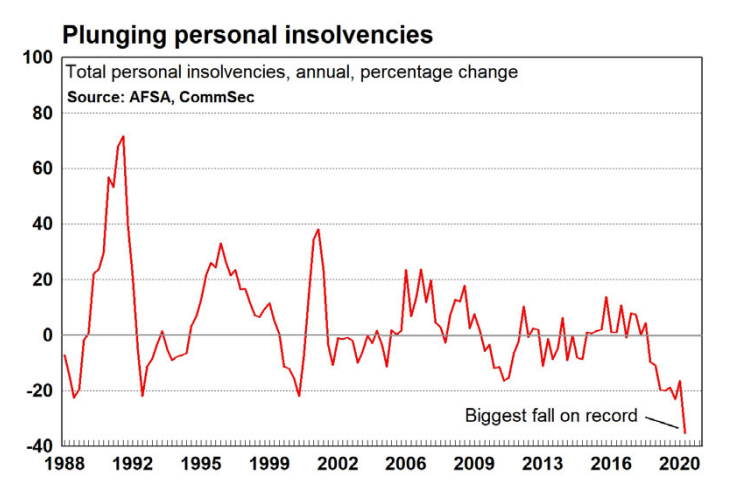

Amendments to the Corporations and Bankruptcy Acts – including the relaxation of insolvent trading laws for six months – have delayed business insolvencies and related personal bankruptcies during the COVID-19 crisis.

These rules, alongside massive emergency income support and debt repayment deferrals, have seen personal insolvencies plunge to record low levels:

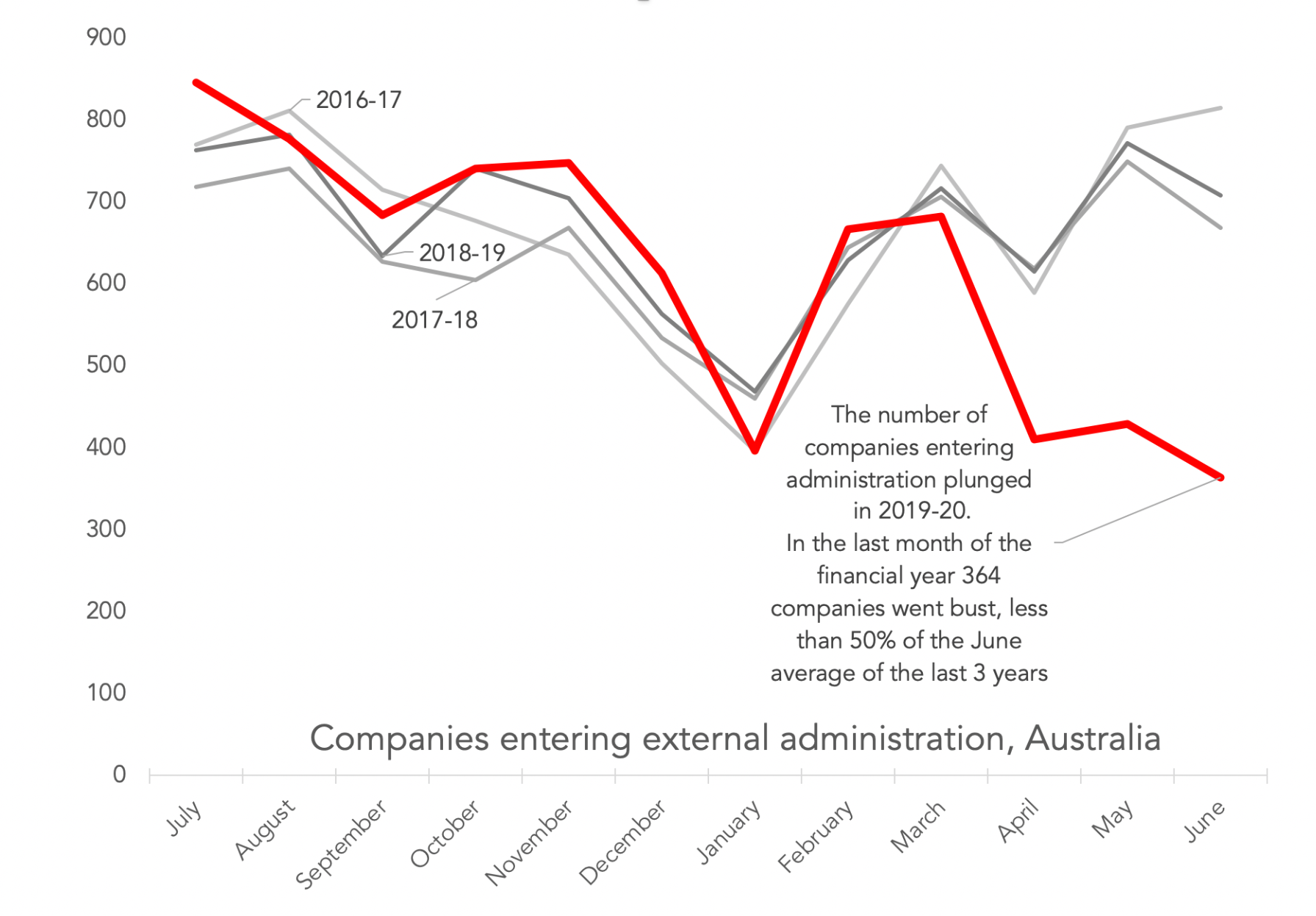

Whereas the number of companies entering administration also plunged to less than 50% of ‘normal’ levels:

Advertisement