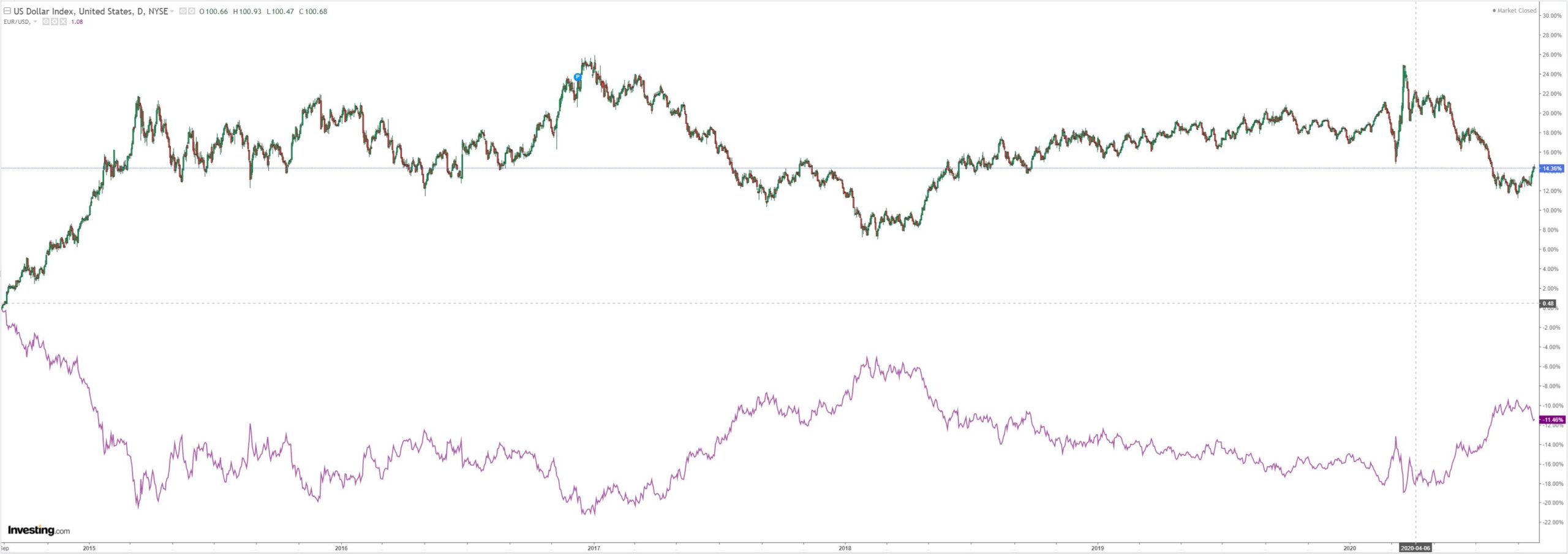

DXY reversed lower last night after its big bounce:

That couldn’t save the Australian dollar which kept on falling:

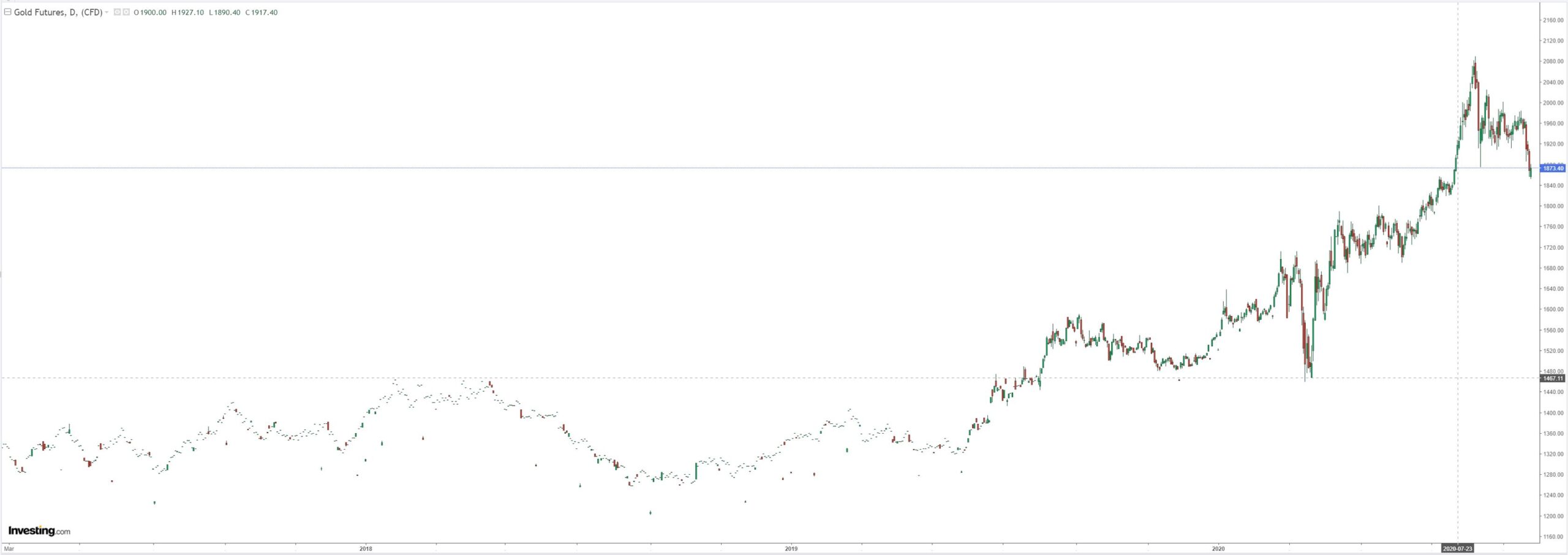

Gold bounced:

Oil hung on:

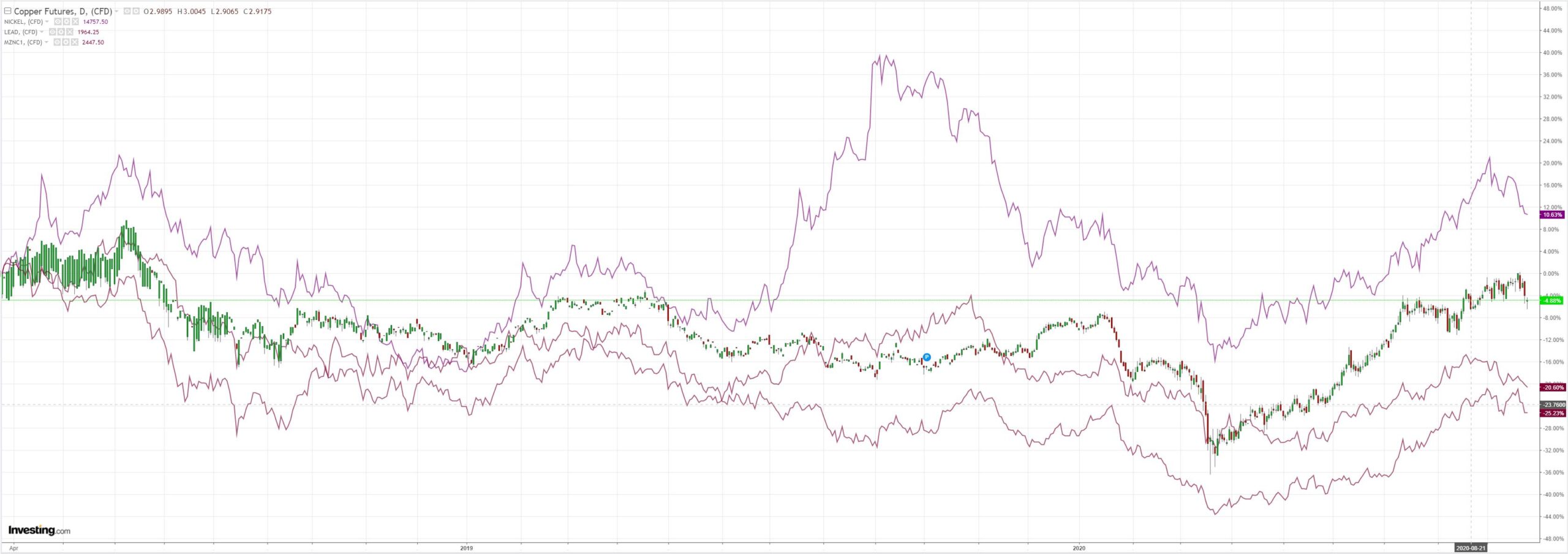

Metals fell some more:

Miners were mixed:

EM stocks are not well:

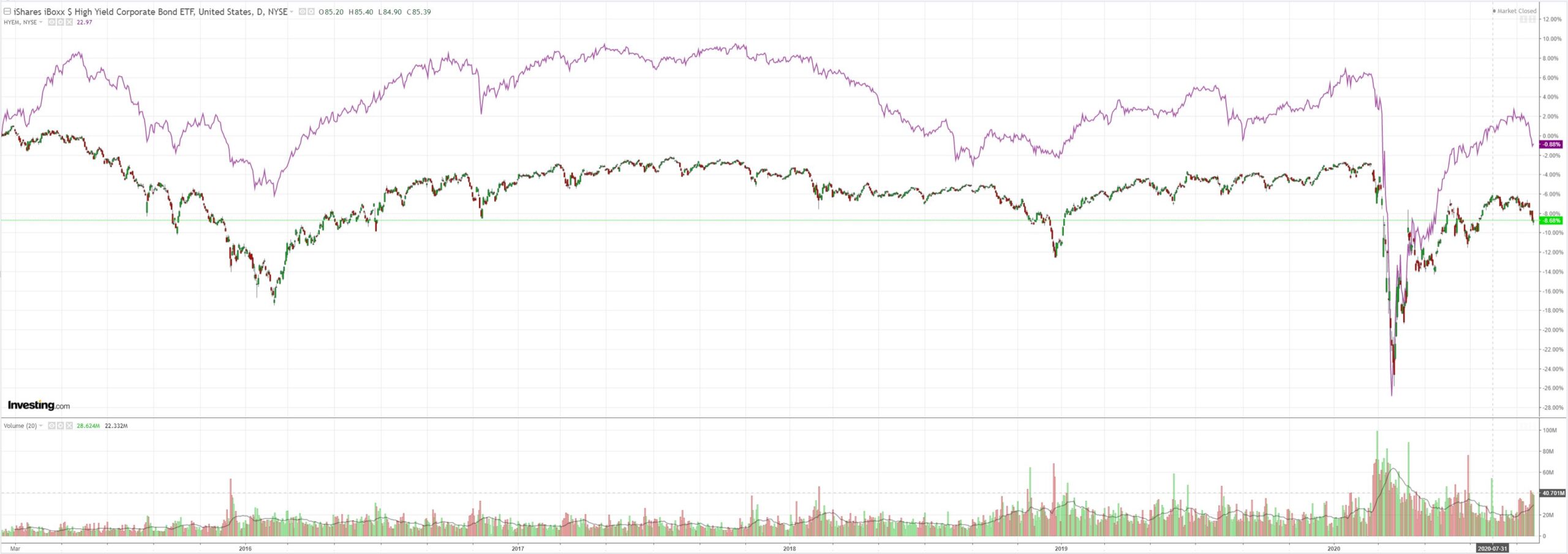

But junk managed to stop falling:

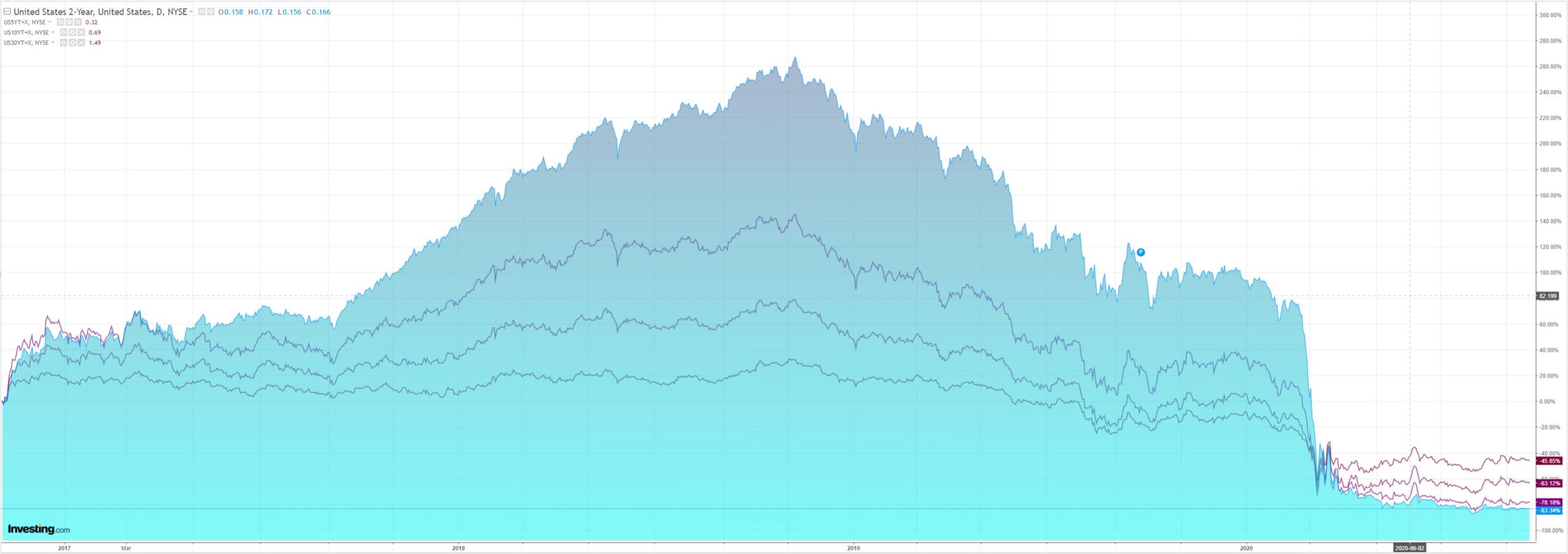

US yields still stalled:

Stocks held on…just:

Westpac has the wrap:

Overnight Market Wrap

Global market sentiment: The recent slide in equity markets stalled as hopes for a US fiscal stimulus package resurfaced. The S&P500 is up 0.3%, and bond yields and the US dollar are little changed. The Swiss and Norwegian central banks remained on hold.

Currencies: The US dollar index is unchanged on the day. EUR initially fell further to 1.1627 (two-month low) but then bounced to 1.1686. USD/JPY ranged between 105.20 and 105.53. AUD initially fell further to 0.7016 (two-month low) before bouncing to 0.7070. NZD similarly found a base at 0.6512 (one-month low) before bouncing to 0.6560. AUD/NZD fell from 1.0800 to 1.0754.

Interest rates: US 2yr treasury yields ranged between 0.13% and 0.14%, while the 10yr yield ranged between 0.66% and 0.67%.

Australian 3yr government bond yields (futures) traded between 0.21% and 0.22%, while the 10yr yield ranged between 0.84% and 0.86%.

Commodities: Brent crude oil futures are unchanged at $41.80, copper fell 0.8%, and gold was unchanged.

Event Wrap

Treasury Secretary Mnuchin said in testimony that he hopes to restart negotiations on another fiscal relief bill with House Speaker Pelosi. “I’m willing to sit down anytime for bipartisan legislation, let’s pass something quickly,” he said.

US new home sales continued to rise in August, the 1011k gain (vs est. 890k) the highest since late-2006. July was revised to 950k from 901k.

Kansas Fed manufacturing survey fell to 11 (from 14, est. 14). Activity was below year ago levels for most firms, and while companies remain relatively optimistic about the coming year, little wage growth is expected.

Weekly initial jobless claims rose to 870k (vs est. 840k, prior 866k), while continuing claims pulled back to 12.580m (vs est. 12.275m, prior 12.747m).

Germany’s IFO business survey rose to 93.4 (vs est. 93.9, prior 92.5), French business confidence up to 92 (vs est. 94, prior 90).

The Swiss National Bank left both its policy rate and its deposit rate unchanged at -0.75% and reiterated its pledge to use foreign exchange interventions if needed.

Norges Bank decided to keep its key policy rate at 0%, saying it will most likely stay at that level for some time. It did increase its policy rate forecast for Q4 2022 from 0.16% to 0.21%.

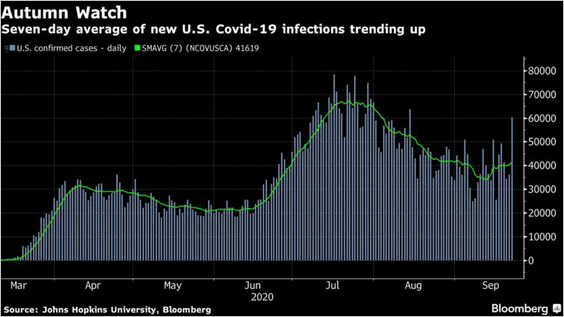

None of that matters. All that does is the election and its interplay with the virus. The latter is rising into Autumn:

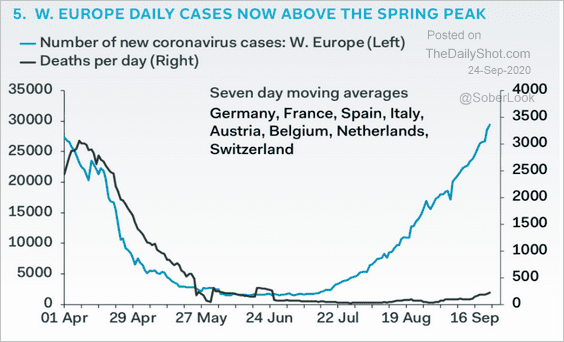

Uh oh. More shutdowns coming. Especially if Biden wins. And the EUR is in trouble as Europe sickens:

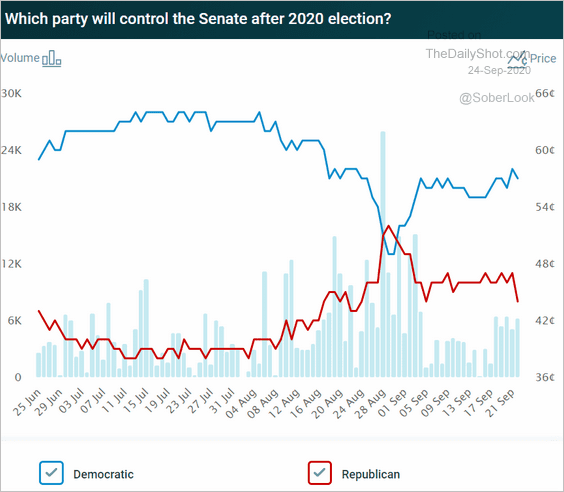

Enter a Democrat clean sweep:

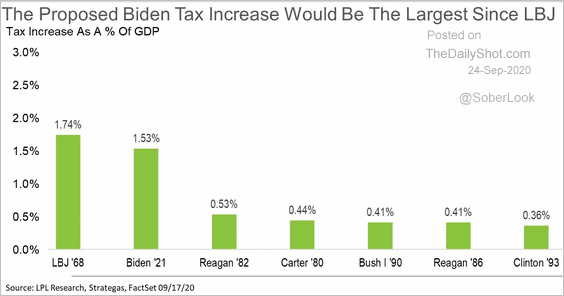

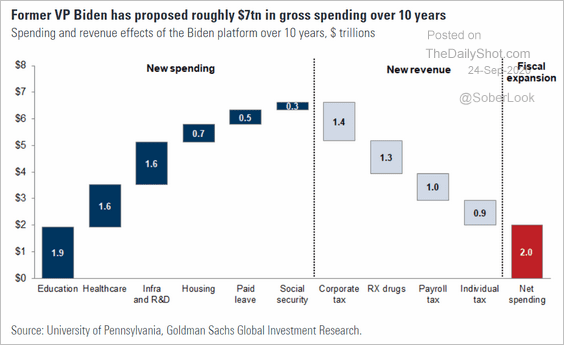

Which gives the stock market bubble a double shock to earnings and to capital gains for punters as taxes are lifted:

Where’s the upside here for risk? And, by extension, the Australian dollar?

Gone.