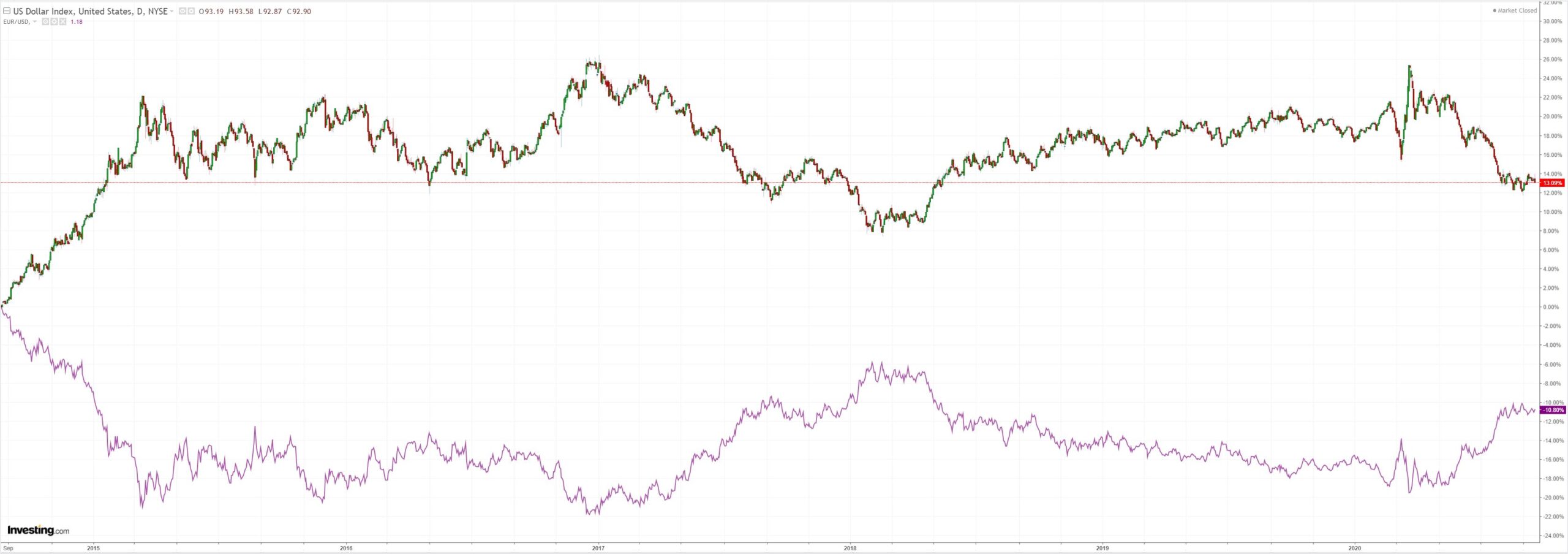

DXY was soft last night, EUR firm:

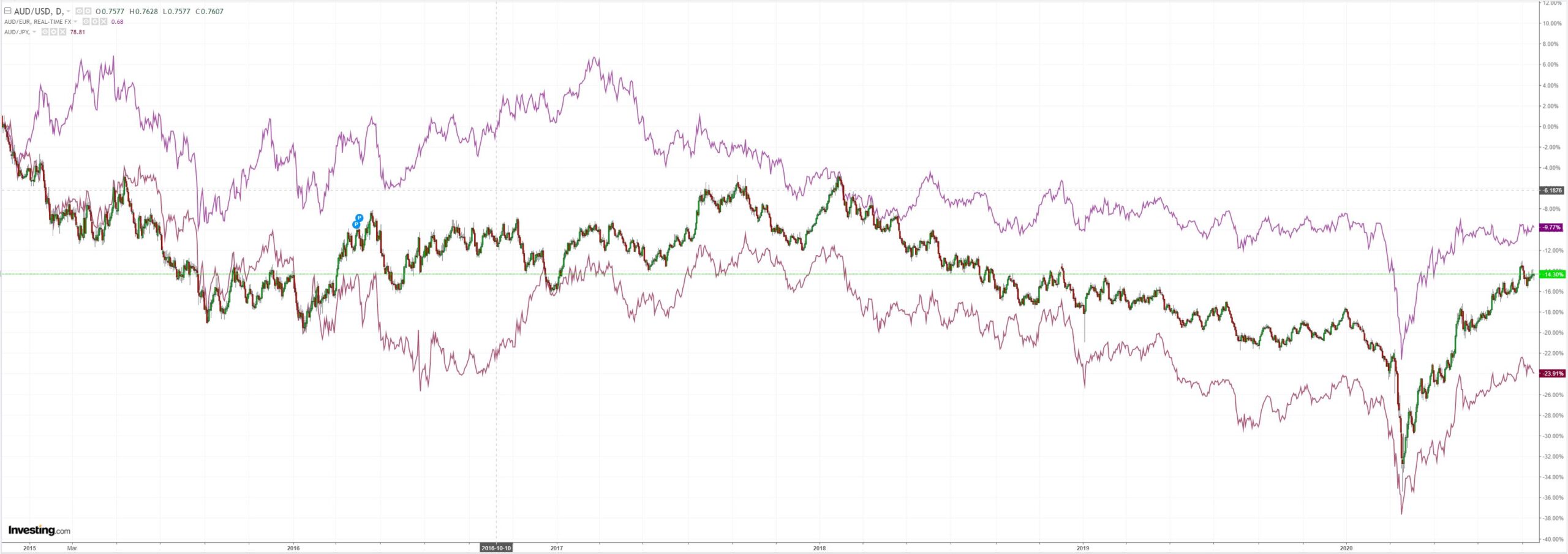

The Australian dollar still looks strong across the DM board:

Weirdly, EMs are rallying as risk diminishes:

Gold couldn’t capitalise:

Not sure what happened to WTI:

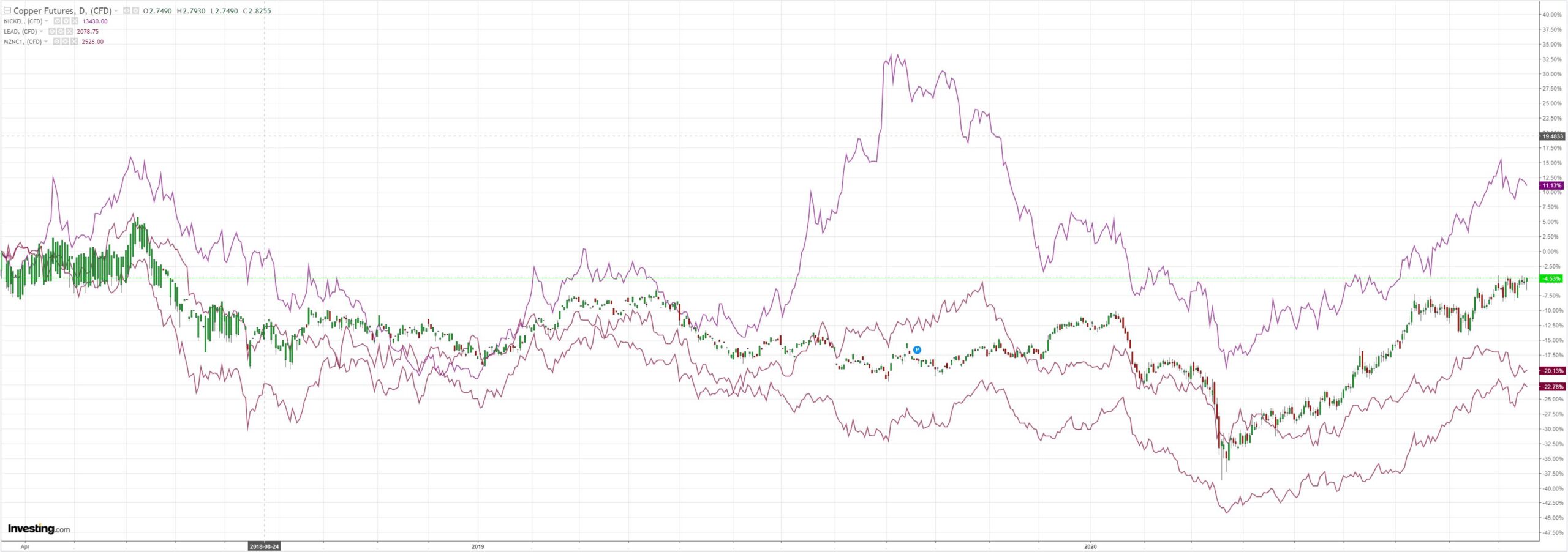

Base metals are bifurcating:

Miners are still solid:

EM stocks too:

Junk looks toppy:

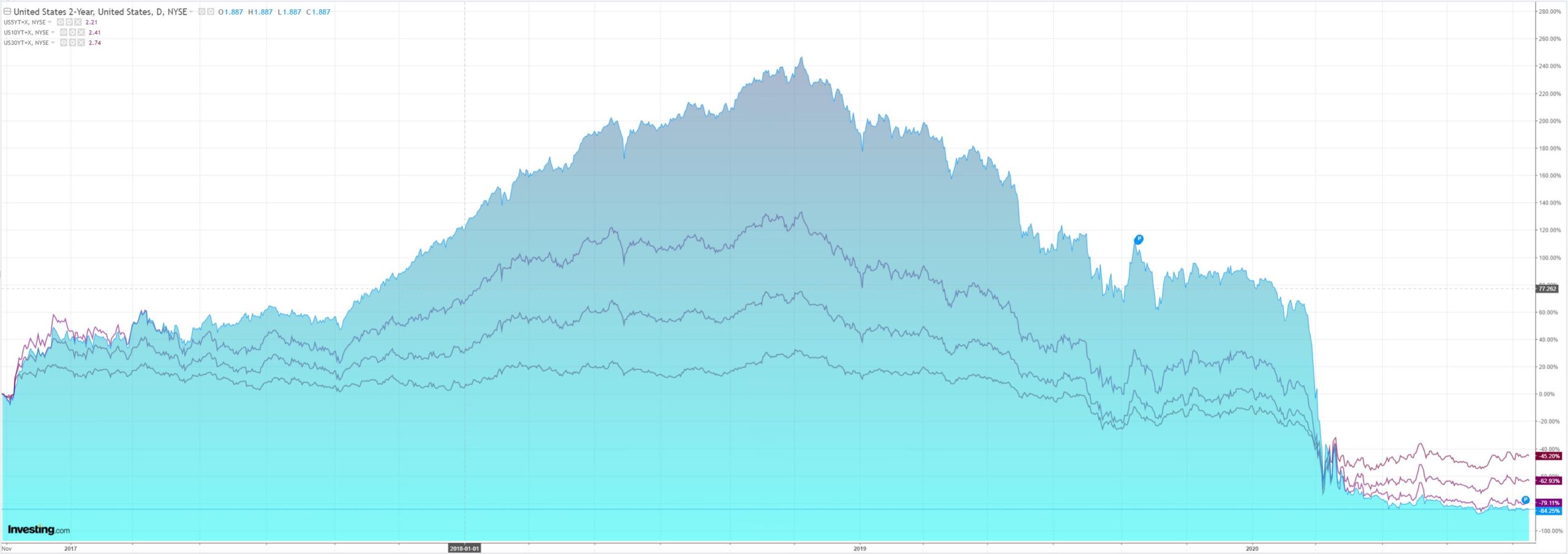

US yields are pancaked:

US stocks have formed a very attractive head and shoulders top. The neckline is intact but lookout if it breaks:

Westpac has the data wrap:

Event Wrap

Robert Redfield, director of the Centers for Disease Control and Prevention, told a Senate committee that even if a vaccine were approved this year, it wouldn’t be ready to be widely distributed to Americans until next summer or fall.

US housing starts undershot estimates with a -5.1% fall in August to a still-elevated 1.416m pace. Building permits fell -0.9% to 1.470m pace, following three consecutive gains from a five-year low in April. The Philly Fed business activity index fell -2.2 points to a still-solid 15.0 reading, and well above the 40-year low of -56.6 in April. The components were stronger than the headline. Initial jobless claims of 860k in the latest week were close to estimates (850k), while continuing claims fell to 12,628k (vs 13,000k expected) in the first week of September. The report was fairly neutral overall.

The BoE’s MPC left the repo rate and QE settings unchanged, at 0.10% and GBP 745bn, as had been widely expected. The summary and minutes noted that the outlook is unusually uncertain, despite recent data being better than expected. Despite economic growth forecast to continue recovering, unemployment was expected to rise, consistent with spare capacity. The summary stated that “the Committee does not intend to tighten monetary policy until there is clear evidence that significant progress is being made in eliminating the spare capacity and achieving the 2% inflation target.” The last paragraph in the minutes discussing negative rates was a surprise for markets: “The Committee had discussed its policy toolkit, and the effectiveness of negative policy rates in particular, in the August Monetary Policy Report, in light of the decline in global equilibrium interest rates over a number of years. Subsequently, the MPC had been briefed on the Bank of England’s plans to explore how a negative Bank Rate could be implemented effectively, should the outlook for inflation and output warrant it at some point during this period of low equilibrium rates. The Bank of England and the Prudential Regulation Authority will begin structured engagement on the operational considerations in 2020 Q4.”

Event Outlook

Japan: Annual CPI inflation is slowing, partly due to the travel promotion subsidy’s impact on accommodation prices (prior: 0.3%, market f/c: 0.2%).

UK: The recovery in retail sales is expected to moderate in August after a 3.6% gain to pre-pandemic levels in July (market f/c: 0.8%).

US: A slight improvement in September’s Uni. of Michigan consumer sentiment is anticipated following an uptick in August (prior: 74.1, market f/c: 75.0). The August leading index is expected to be little changed (prior: 1.4%, market f/c: 74.9). The FOMC’s Bullard will speak on the Covid Recovery Challenge (0:00 AEST).

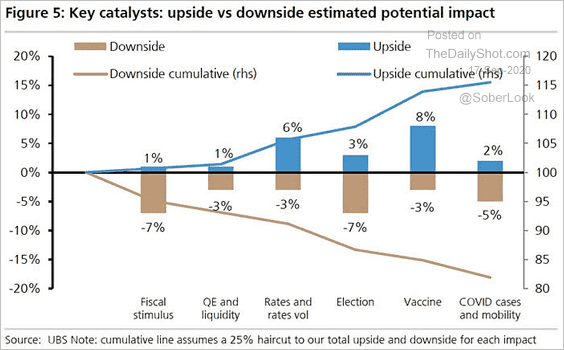

Interesting price action. The bid into EMs is largely being sustained by a falling DXY even as risk comes off in stocks thanks to the first wave of stimulus tightening. That holds up the Australian dollar as well. A neat chart from UBS tells the tale:

At least until the election, I expect equity volatility (biased towards weakness) to persist. So, I don’t think it likely that the soft DXY can be sustained short term, especially so given how lopsided is positioning in the short trade.

It is more likely than not that we see a deeper correction short term for everything except DXY, including the Australian dollar.