DXY is stong again and has formed a head and shoulders bottom. EUR reflects:

The Australian dollar was crushed:

But EMs more:

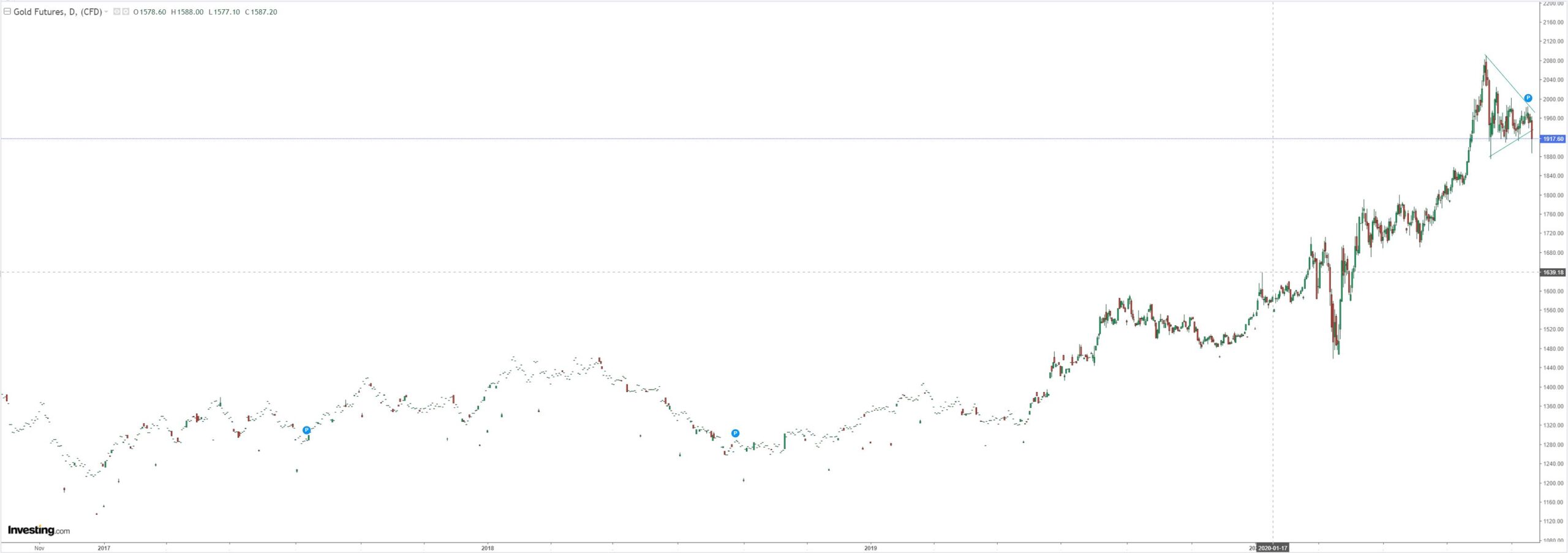

Gold’s bullish pennant broke down:

Oil is in trouble as Libya returns:

Base metals were crunched:

Big miners drove into a pothole:

EM stocks gapped lower:

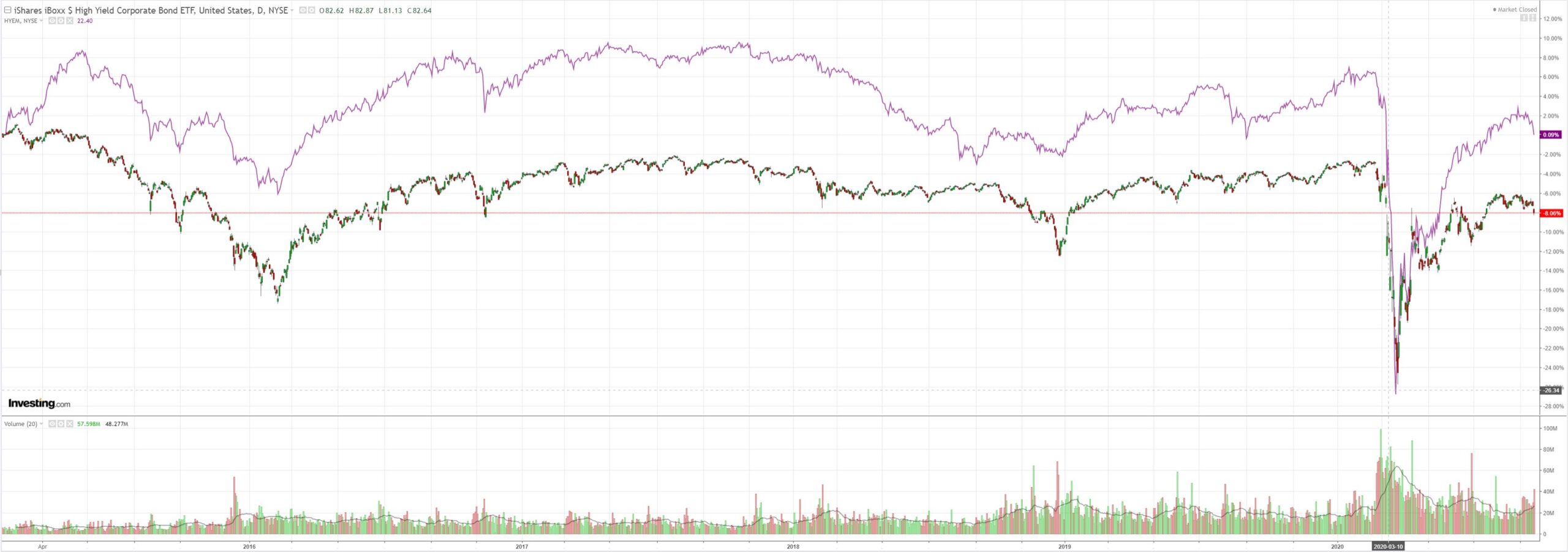

Junk is now screaming a warning for risk:

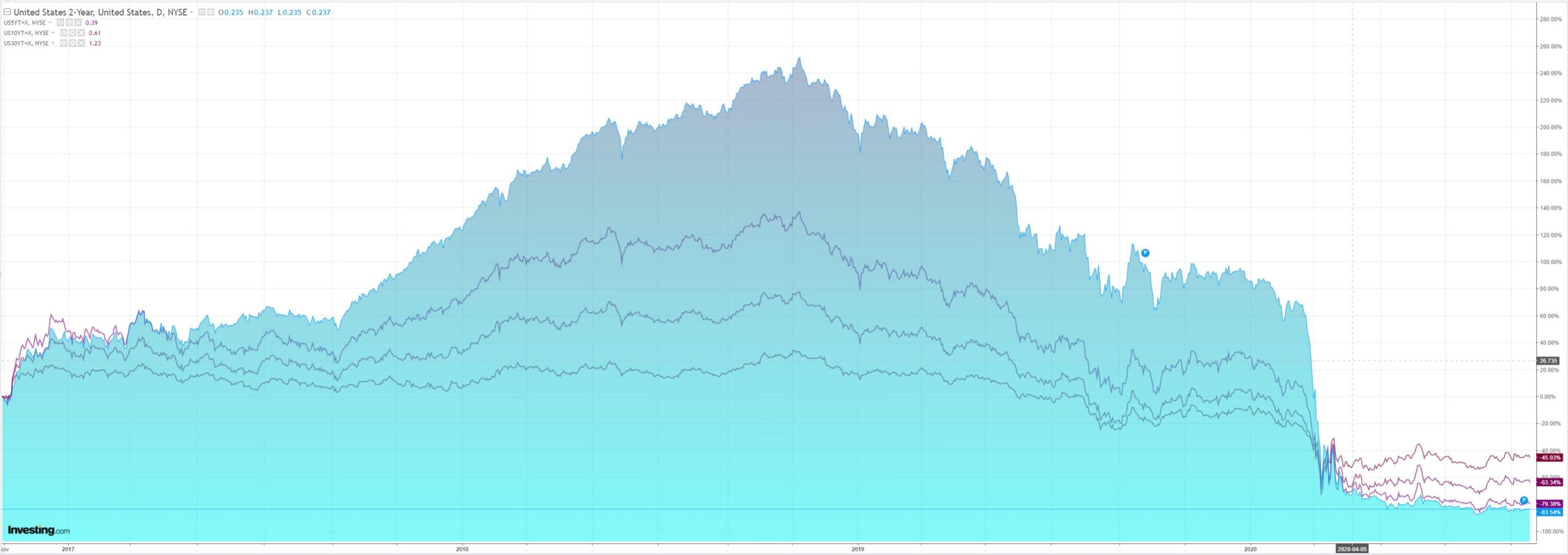

US bonds were bid:

Stocks were hit. Nasdaq clung to the neckline:

Westpac has the wrap:

Event Wrap

The Chicago Fed national activity survey for August continued to gyrate, pulling back to +0.79 from +2.54 (revised from 1.18) in July.

The BBC reported that the UK may move from Covid alert level 3 to 4, amid a rise in cases. PM Johnson will give a speech tomorrow after a special Cabinet meeting. London’s Mayor, Khan, said restrictions will be revealed after discussions with Johnson on Tuesday.

Event Outlook

Australia: Weekly payrolls to 5 Sep are likely to exhibit some improvement in momentum after August figures reflected Victoria’s lockdown (prior: -0.4%). RBA Deputy Governor Debelle will speak at 10:30am on “The Australian Economy and Monetary Policy”.

Europe: The resurgence of Covid cases in the region is expected to act as a headwind to consumer confidence’s recovery (prior: -14.7, market f/c: 15.0).

US: Lower mortgage rates have boosted the housing market as the economy reopened. A moderation is anticipated after July’s gains in existing home sales (prior: 24.7%, market f/c: 2.4%). Improving conditions are supporting manufacturing sentiment, according to the Richmond Fed index (prior: 18, market f/c: 12).

This correction is getting moving. S&P broke its 50DMA and is on its way lower, still far above stronger supports like the 200DMA. It’s now clear as well that DXY will rerun its traditional safe haven role once more despite all of the Fed’s efforts which, frankly, are just not enough. In the absence of all fundmanetal drivers, the Fed is either giving or it is taking away and right now it is the latter:

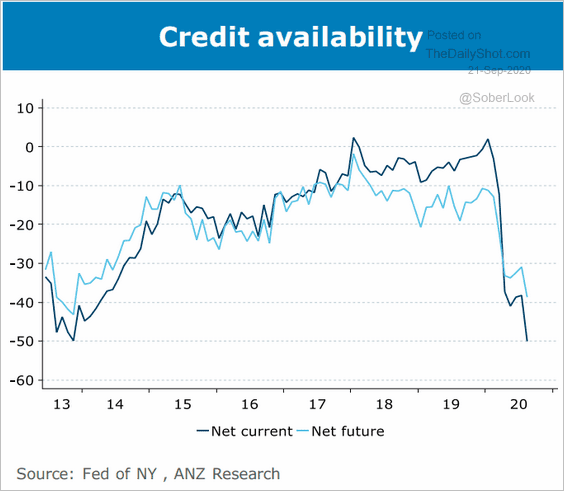

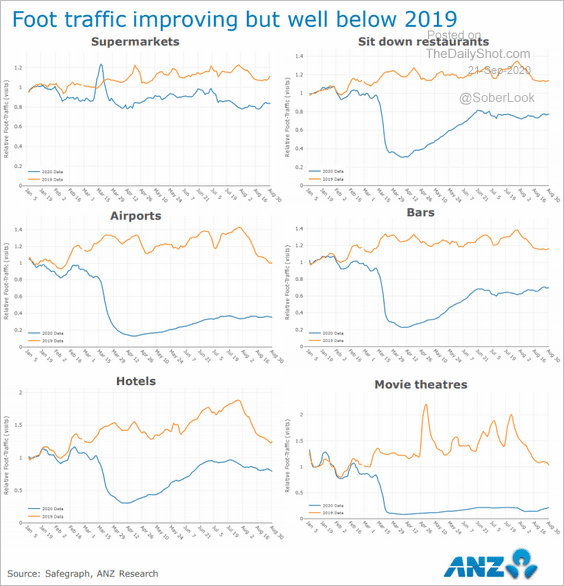

There is no US recovery:

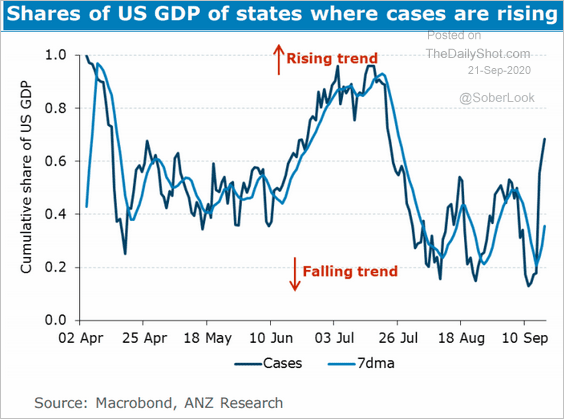

The virus is returning again:

And the hope of the next fiscal package has been dealt another blow by the death of Ruth Bader Ginsberg as Capitol Hill now has another reason to brawl rather than agree to anything pre-election. Not to mention the election itself. And hard Brexit to weigh on EUR.

If DXY is bid once more then Fakeflation is in trouble and the Australian dollar with it.