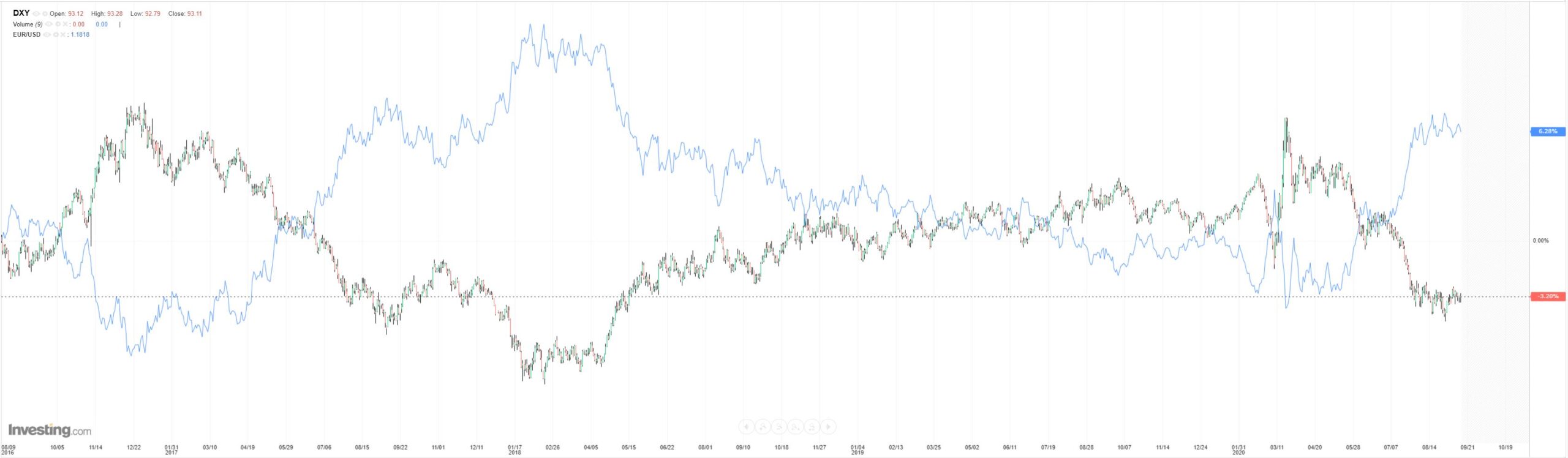

DXY firmed last night and EUR fell:

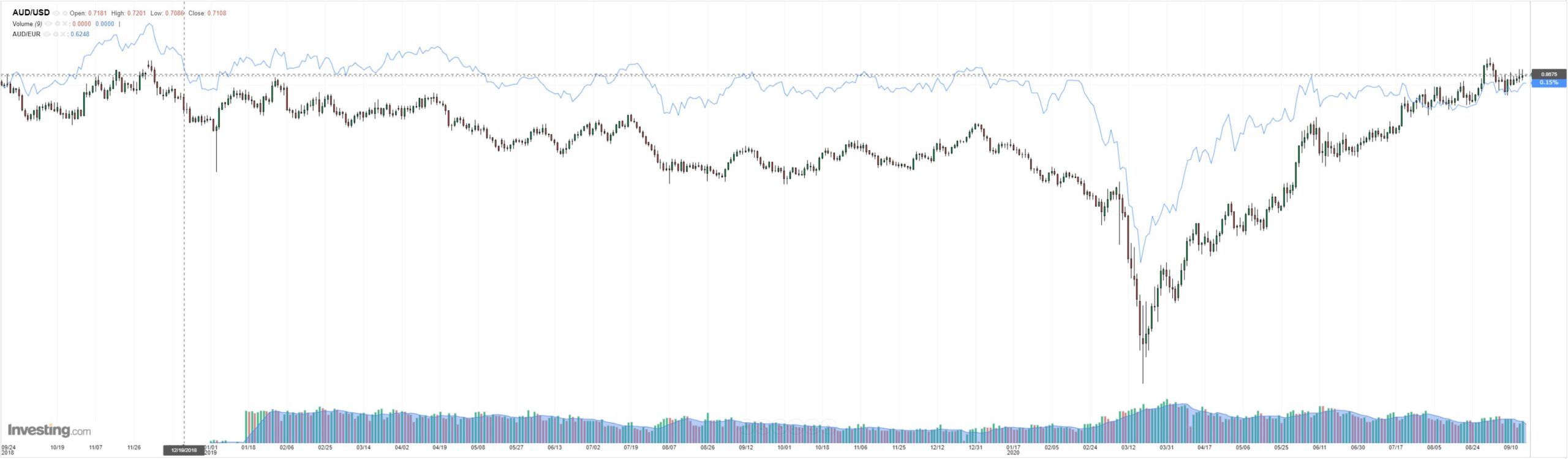

The Australian dollar was roughly flat:

Gold was firm:

Oil jumped:

Junk is still fine:

The US 10 year sold a bit:

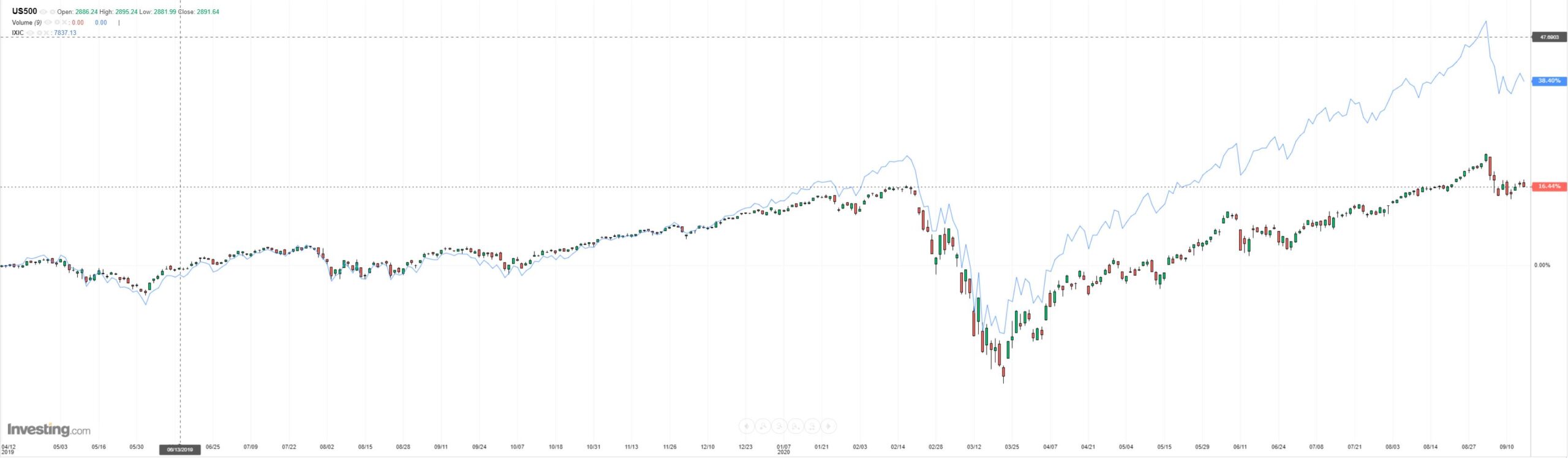

Stocks too a hit:

Westpac has the data wrap:

Event Wrap

The FOMC retained its policy stance, as was widely expected, indicating it will keep rates at the current low level for the next few years. The Committee did further underpin its posture by stating it will aim for an inflation rate moderately above 2% for some time so that inflation averages 2% over time. The dot plot rate projection showed members expected the 0.125% target midpoint to remain unchanged through to 2023 (apart from one expecting a hike in 2022 and four expecting such in 2023). The Fed reiterated that it will in coming months increase its holdings of Treasuries and MBS “to sustain smooth market functioning and help foster accommodative financial conditions.” Economic forecasts reflected an improved outlook on 2020 growth, followed by a more restrained 2021-23 bounce.

US retail sales faltered in August, headline sales up 0.6%m/m (vs est. +1.0%, and prior revised to +0.9%m/m from +1.2%m/m), and the control group down 0.1%m/m (est. +0.3%m/m, prior revised to +0.9%m/m from +1.4%m/m). The NAHB homebuilder sentiment survey rose to a record high of 83 (survey began in 1985), well above the estimates of (unchanged at) 78. Single family homes (88, prior 84) helped drive the index higher, along with general buyer “traffic”, with NAHB citing lower mortgage rates and demand for suburban homes. The increase in activity was said to be driving up lumber prices and thus building costs.

The ECB’s de Cos added to the recent comments from other ECB members, notably Chief Economist Lane, that fx markets would be monitored closely, saying EUR strength was dampening inflation. Although key member Schnabel said that ECB does not target fx, she did say that the market would be monitored.

UK inflation data for August was not as soft as expected, headline CPI down 0.4%m/m and +0.2%y/y (vs est. -0.6%m/m and 0.0%y/y), and core +0.9%y/y (est. +0.5%y/y, prior +1.8%y/y).

Event Outlook

Australia: Following July’s rebound in employment of 114.7k, the Victoria shutdown and a levelling out of employment growth in NSW is expected to see employment decline overall. Westpac and the market expect falls of 50k and 35k respectively. The unemployment rate should edge up from 7.5% in July (Westpac and market f/c: 7.7%).

New Zealand: The April Level 4 lockdown severely restricted activity in Q2. Westpac expects a GDP contraction of 11.5% – slightly less severe than the market at -12.5% (prior: -1.6%).

Eurozone: Final CPI inflation for August is expected to confirm inflation remained negative for another month after reaching record lows in July (prior and market f/c: -0.4%).

UK: No policy change is expected from the BoE, although downside risks will be highlighted.

US: Momentum in housing starts (prior: 22.6%, market f/c: -3.1%) and building permits (prior: 18.8%, market f/c: 3.2%) is expected to moderate in August after a rapid recovery from their COVID lows. September’s Philly Fed index is anticipated to remain in expansionary territory (prior: 17.2, market f/c: 15.0). Initial jobless claims have continued to edge lower as more unemployed Americans exhaust jobless benefits (prior: 884k, market f/c: 850k).

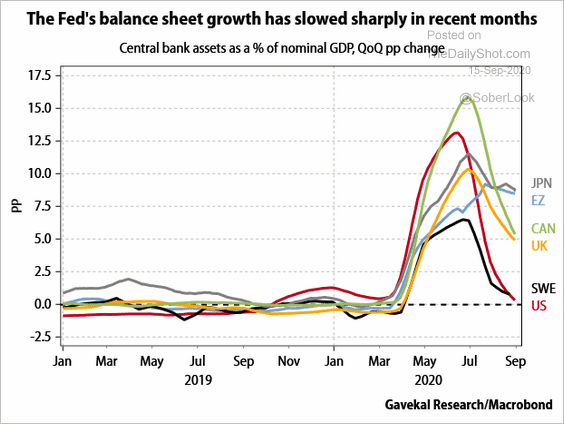

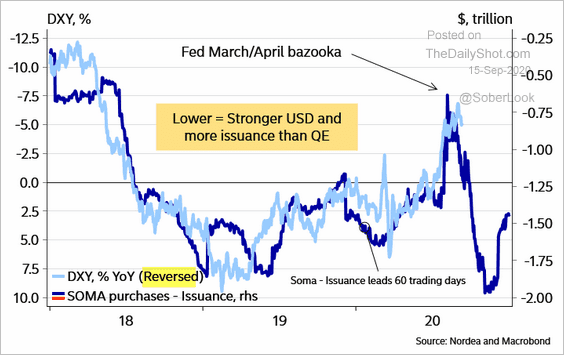

The FOMC is showing no sign of advancing to further easing. Indeed, its balance sheet expansion is all but over:

Which usually means one thing, a rising DXY:

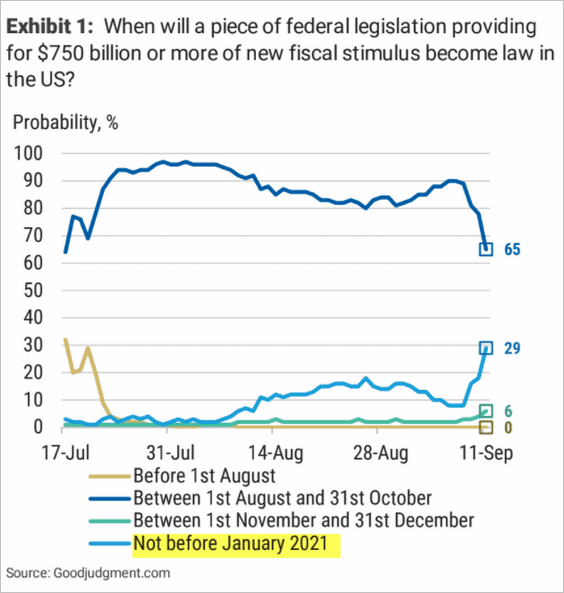

Don’t get me wrong. I don’t see a trend change for the declining DXY. But there are reasons to be short term cautious about a corrective rally. The Fed is one. Stalled fiscal is another:

Which will matter soon enough:

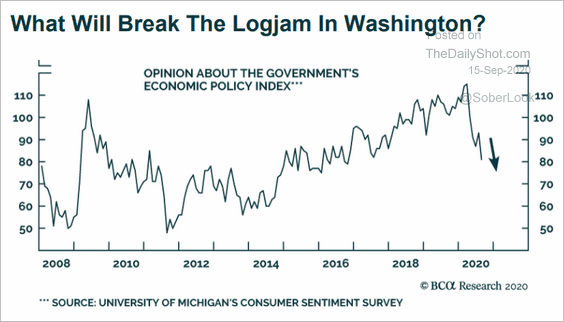

Then there is the US election which will certainly test risk appetite. And there is this:

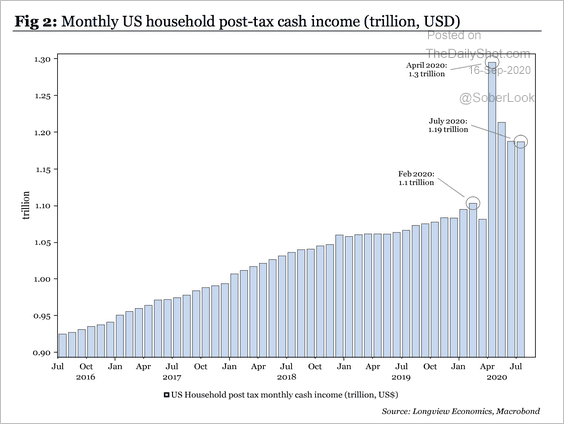

Plus this:

What happens if there’s no trade deal by 31 December?

When transition ends, the UK will automatically drop out of the EU’s main trading arrangements (the single market and the customs union).

The single market means that countries share the same rules on product standards and access to services, whereas the customs union is an agreement between EU countries not to charge taxes (tariffs) on each other’s goods.

If a new trade deal is not ready then tariffs and border checks would be applied to UK goods travelling to the EU. The UK could also do this to EU goods, if it chose to.

Tariffs would make UK goods more expensive and harder to sell in the EU, while full border checks could cause long delays at ports.

Failure to reach a deal would also result in the UK service industry losing its guaranteed access to the EU. This would affect everyone from bankers and lawyers, to musicians and chefs.

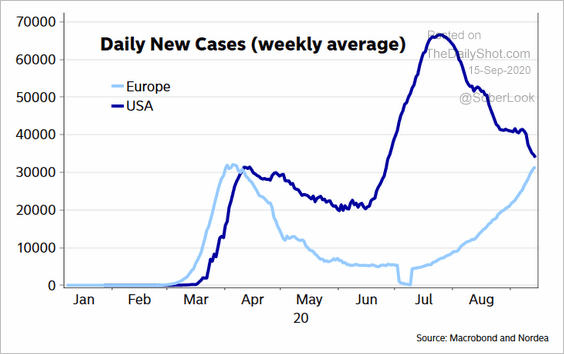

The flip side of DXY is the EUR and more virus plus political instability equals less economic activity and a sizable dent in the EUR rising trade.

Lots of reasons to see short term strength in DXY and weakness in the AUD.