SoftBank is the “Nasdaq whale” that has bought billions of dollars’ worth of US equity derivatives in a series of trades that stoked the fevered rally in big tech stocks before a sharp pullback on Thursday and Friday, according to people familiar with the matter.

…“These are some of the biggest trades I’ve seen in 20 years of doing this,” said one derivatives-focused US hedge fund manager. “The flow is huge.”

…One person familiar with SoftBank’s trades said it was “gobbling up” options on a scale that was even making some people within the organisation nervous. “People are caught with their pants down, massively short. This can continue. The whale is still hungry.”

The Nasdaq was at one point on Friday down 10 per cent from its peak — the common definition of a correction — yet the options boom means that the US stock market remains vulnerable to further bursts of volatility, according to Charlie McElligott, a strategist at Nomura. “The street is still very much in a dangerous space, and that flow is still out there,” he wrote in a note on Friday.

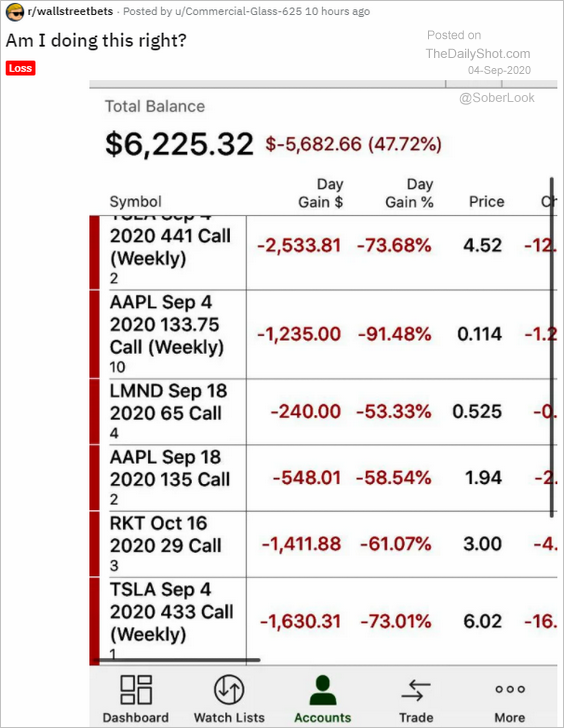

Jason Goepfert, president of Sundial Capital Research, says that while SoftBank may be the biggest player, it can’t be just one firm whipping up markets. Small day traders have spent $40 billion in call premiums in a month, data he compiled from the Options Clearing Corp. show. That’s a hefty amount for retail investors to be wielding and dwarfs what SoftBank is reported to have spent.

“Softbank as a call buyer makes sense, as does the underlying buying it generates. But trades less than 10 contracts swamped the rumored Softbank buys, so clearly others were trying to tag along for the ride,” Goepfert said. “Not sure why now versus other years, other than stay-at-home boredom. Maybe the retail crowd saw this as their last, best change to get rich quick.”

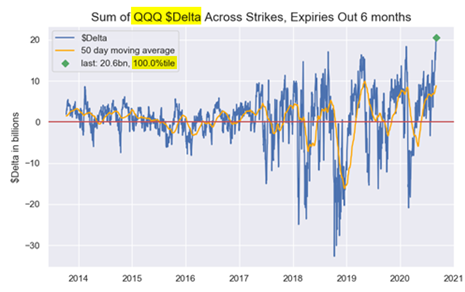

Demand for upside call options in Salesforce.com began to rise at the start of August, before its earnings report sent cash equity shares surging. From the start of the month to the day before the software-marker reported, total call open interest more than doubled from 181,000 to 389,000. Now, the number of outstanding bullish call contracts on the stock stands near 700,000, the highest level on record.

If it stops then it’s game over. The whale is trapped. It’s going to get slaughtered as the gammaquake breaks. More from McElligott:

Advertisement

Yesterday was obviously the “…as it turns the other way to the downside” part, with the coiling convexity that is the reality of hedging “short gamma” as it relates to the sensitivity of the options that dealers are short to the then vacuum-like collapse in price of the underlying securities, i.e. the single-name Tech momentum longs which saw all the buying of calls, call spreads and riskies traded recently as part of the large upside buying flow from the institutional mkt participant as well as the Robinhood short-dated OMT Calls in said “gamma proxies” (i.e. continue to watch TESLA spot as a “leading indicator” today); to single-name delta and the NQ & ES “upside” & futs bot by dealers to hedge “CRASH UP” over the past few weeks).

That much accumulated “short gamma” doesn’t just go away in a ~4% flush – the Street is still very much in a dangerous space, and that flow is still out there in full “Resevoir Dogs” standoff fashion both to UPSIDE AND DOWNSIDE (again, short gamma = sell when mkt going lower, buy when mkt going higher).

Is there any point overlaying this bubble lunacy with a macro narrative? Nope. But I’ll give you a flavour of it.

Growth prospects for the globe are very slowly improving as stimulus persists and the vaccine wave sweeps in. This presents yields with a short term quandary as they’d like to steepen the curve vis-a-vis the better US jobs report.

Advertisement

But equity markets have run so completely crazy that any passing of the baton from fakeflation to fundamentals only presents the outcome that they crash. In short, the equity bubble is now the number one risk to any recovery.

Expect fireworks for equities and, increasingly, forex.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.