DXY is back in a big way. EUR toast:

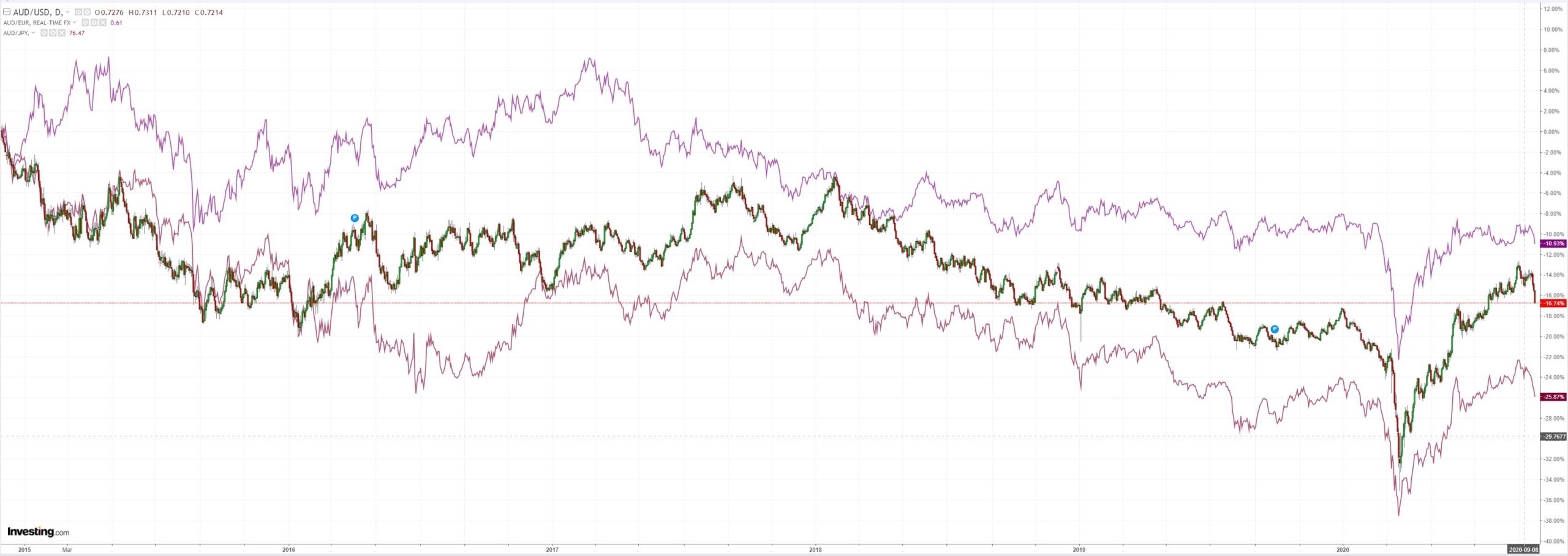

The Australian dollar is in free fall:

Along with EMs:

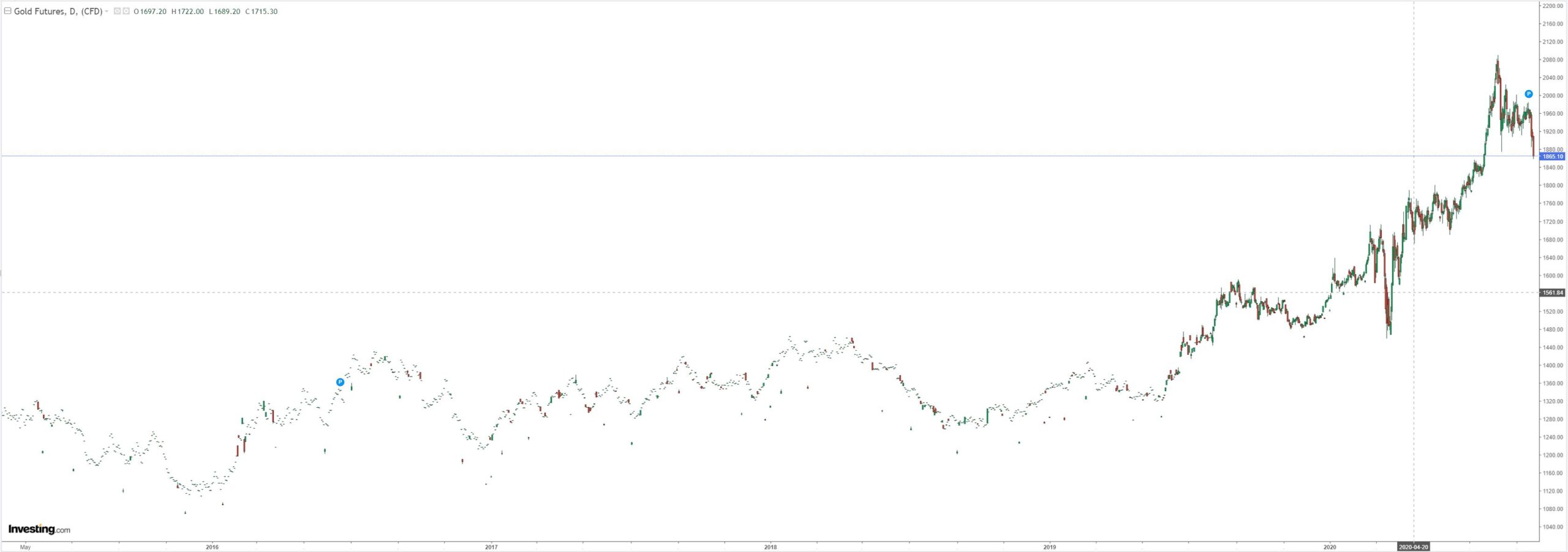

Gold puked:

Oil was OK but it will surely break soon too:

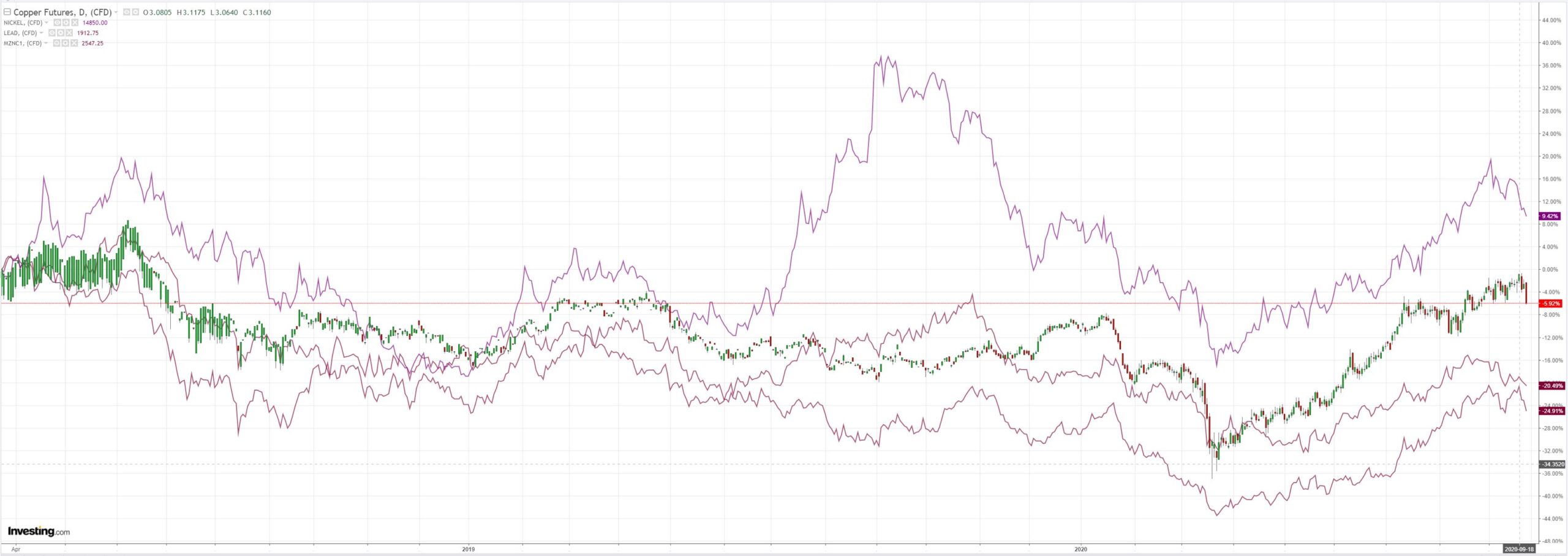

Base metals rolled bigly:

Big miners actually did OK:

EM stocks look ominous:

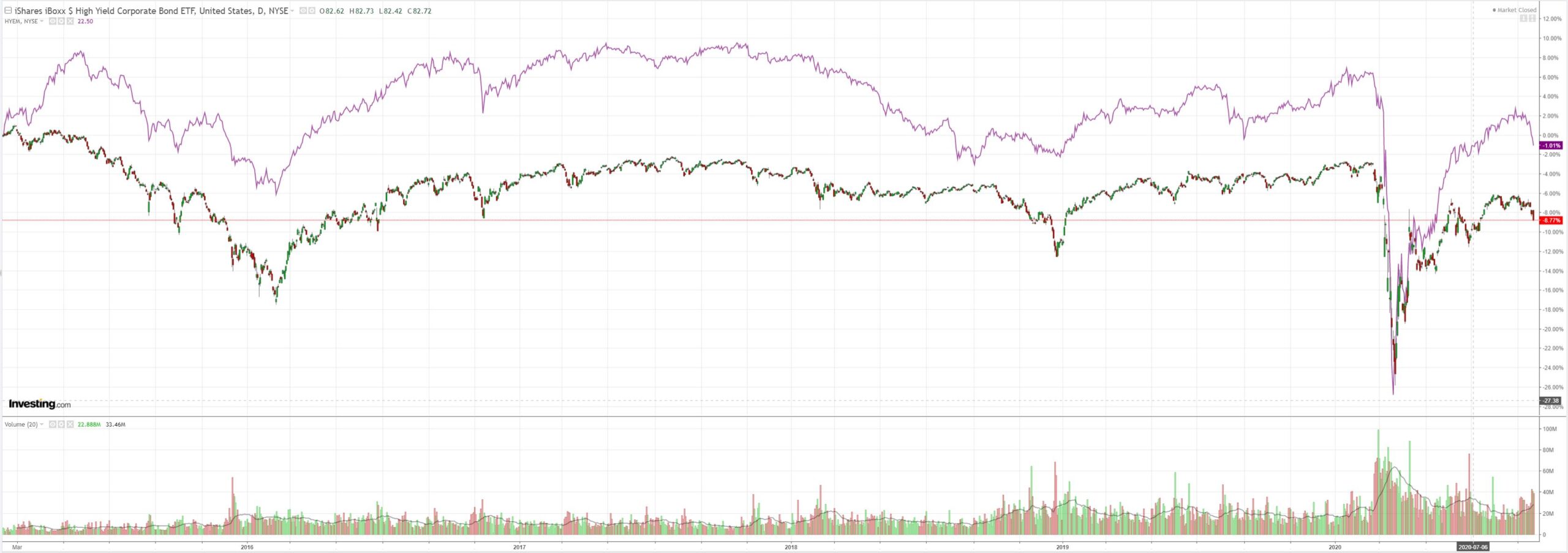

The junk early warning system is screaming at fever pitch:

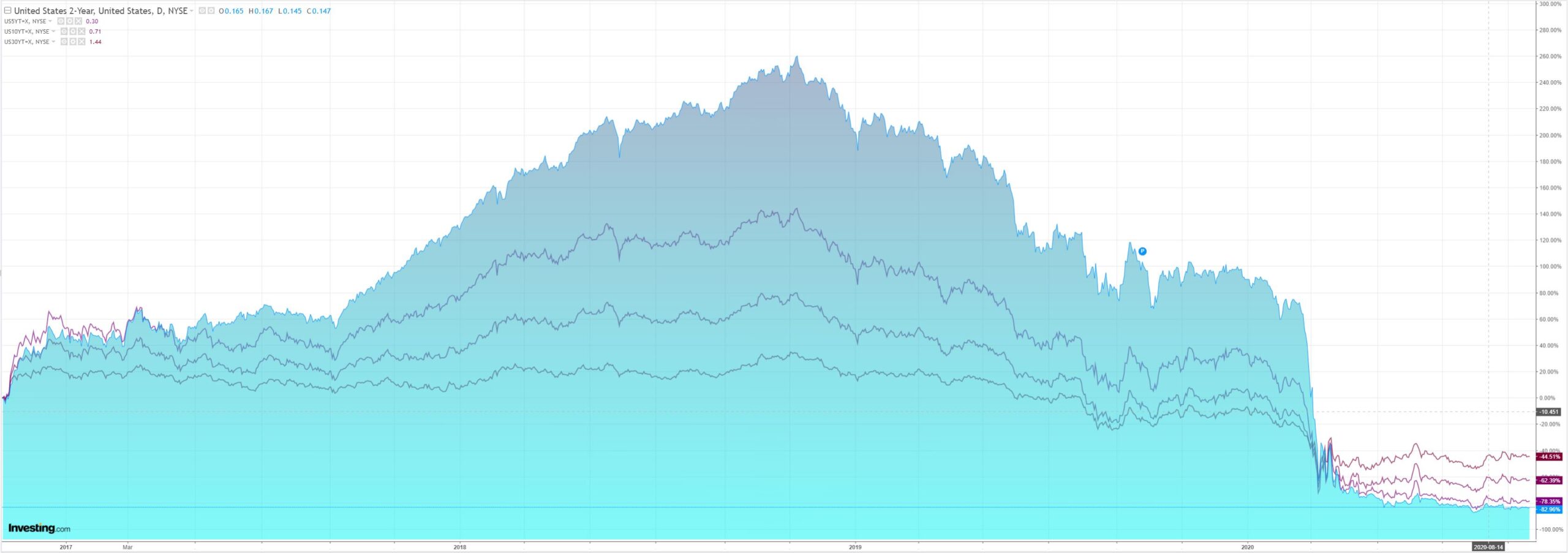

Yields were roughly flat:

As Nasdaq took out the neckline of its head and shoulders top and SPX gathered downside momentum:

Westpac has the data:

Event Wrap

Eurozone September PMIs were dragged down by weakness in service sector activity, notably in France (47.5) and Germany too (49.1). The Eurozone Composite index slipped to 50.1 (vs est. 51.9, prior 51.9), and manufacturing was firmer at 53.7 (est. 51.9, prior 51.7), but services fell to 47.6. However, there was an encouraging lift in activity expectations for 2021 on the basis that COVID would become treatable.

US September PMIs were solid. Manufacturing was as expected at 53.5 (prior 53.1), with services at 54.6 (est. 54.5, prior 55.0).

A plethora of Fedspeak included Chair Powell, who said “there’s still a long way to go”; VC Clarida – the Fed will not raise rates until inflation hits 2%; Rosengren – who is less optimistic on the recovery than other FOMC members; Evans – a 2.5% inflation rate could be seen for some time if the Fed does its job; and Mester – more fiscal stimulus is needed.

Event Outlook

New Zealand: The trade balance is expected to fall into deficit in August, despite import values remaining low on weak demand (prior: 282m, Westpac and market f/c: -350m).

Germany: The IFO business climate survey has improved markedly since April’s lows; September is expected to see a further gain (prior: 92.6, market f/c: 93.8).

US: Initial jobless claims will likely continue to gradually decline; the market expects claims to decrease from 860k to 840k this week. The surge in new home sales appears to be running out of steam as inventory scarcity puts a cap on robust demand (prior: 901k, market f/c 890k). The FOMC’s Bullard (02:00 AEST), Evans (03:00 AEST) and Williams (04:00 AEST) will speak. FOMC Chair Powell will also testify again, this time before the Senate Banking Committee (00:00 AEST).

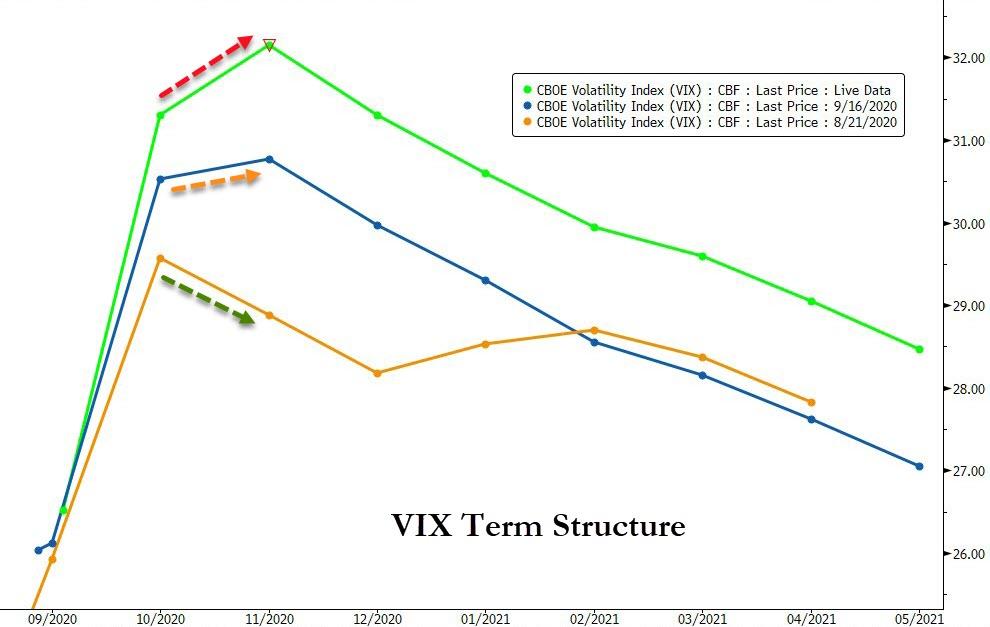

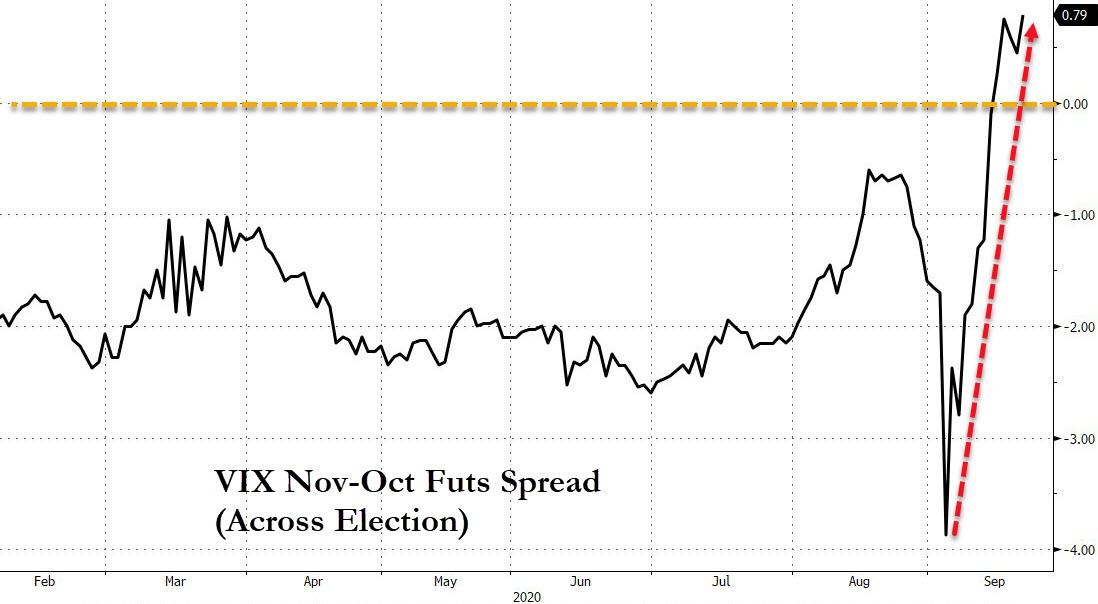

The key drivers remain the US election, stalled fiscal, stalled Fed and rising virus. On the first:

Goldman explains:

One consequence of the pandemic is the fraction of voting occurring via mail is likely to significantly exceed that in prior US elections. Because verification and counting of these mailed ballots does not occur until election dates in some states (including battlegrounds), and given the experience of the primaries, there is a good chance that the result may not be clear on election night.

While markets appear to have internalized this possibility, there are additional potential sources of uncertainty. In particular, there appears to be a significant bifurcation in voting method preferences between Democrats and Republicans, with a significant majority of Democrats expressing an interest in voting by mail and a majority of Republicans preferring to vote in person. This could lead to the appearance of a Trump lead on election day, but a potentially significant portion of the Biden vote still to be counted in the mail-in ballots. In a close election, such an outcome could result in claims/counter-claims of victory and/or litigation, and result in significant market volatility over an extended period.

Nomura’s robot wizard, Charlie McElligot chimes in:

This also likely means that some brave vol traders will try to take advantage as a perceived “generational” opportunity to sell this POST-NOV election “richness” (Dec / Jan) – could be a career “maker or breaker,” with the potential to see monster returns if the event were to pass and all that crash is puked back into the ether… or conversely be turned to dust into a God-forbid realization of chaos, with civil disorder, dual claims to the throne etc.

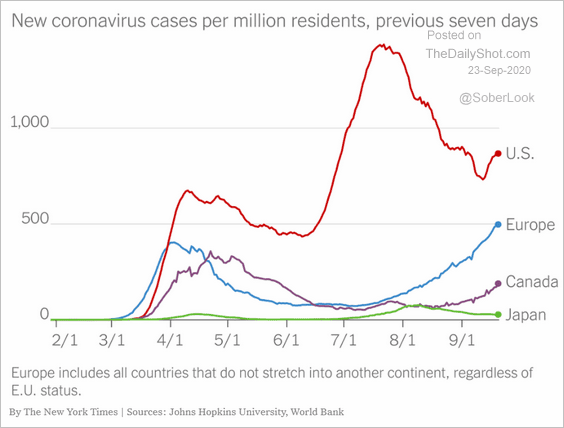

There are more risks than that. The Dems are still front runners and will deliver big corporate tax increases plus lockdowns as the virus rebounds into Winter:

We’re fast lining up for a mighty puke lower in risk here. Including the Australian dollar.