DXY continued its bouncing trend lower last night:

Australian dollar was weak:

Gold too:

Indeed, all commodities:

Miners were soft:

And EM stocks:

Junk has plateaued:

Yields were bid:

Stocks are Icarus:

Westpac has the wrap:

Event Wrap

US ADP private sector employment rose +428k in August, lower than the +1000k expected. ADP gains have undershot those in the more widely followed non-farm payrolls during the growth rebound. July factory orders posted a +6.4%m/m headline rise (est. +6.1%m/m), with a minor lift to durable goods from its preliminary release (ex-transport rose +2.6%m/m, vs preliminary +2.4%m/m).

Eurozone July PPI inflation was in line with expectations (-3.3%y/y) and underscored the distinct lack of inflationary pulse evident in yesterday’s weak August CPI release. German July retail sales fell 0.9%m/m (est. +0.5%m/m), although the annual pace was solid at +4.2%y/y (est. +4.1%y/y).

FOMC members Williams and Mester underscored the Fed’s recent dovish change in policy, as well as the uncertainties around growth and disinflationary risks.

BoE Governor Bailey and several MPC members gave a decidedly dovish outlook to growth and inflation risks to UK Parliament’s Treasury Select Committee.

Event Outlook

Australia: The trade surplus is expected to narrow in July as export growth moderates and imports rebound off their lows (prior: $8.2bn, market f/c: $5.35bn, Westpac: 5.4%).

NZ: ANZ commodity prices will be impacted by the Covid impact on dairy prices.

China: The recovery in Caixin’s services PMI is tapering but at a robust level. (prior: 54.1, market/c: 53.9).

Eurozone: Markit’s services PMI is on solid ground but may be impacted by the repositioning of travel restrictions. Consumer spending appetite has returned in Europe, as reflected by another positive retail sales read of 1.0% in July (prior: 5.7%).

UK: The recovery in Markit’s services PMI is well underway, with August’s 60.1 materially above the expansionary threshold of 50.

US: Initial jobless claims are expected to keep trending lower from 1006k last fortnight to 950k last week. The trade deficit is set to widen in July from -$50.7bn to -$58.0bn as imports outpace exports. The August ISM services PMI will contribute positively to the recovery narrative (prior: 58.1, market f/c: 57.0). The FOMC’s Evans will speak (02:30AEST).

The Australian dollar is still torn between Fed fakeflation driving it up and extreme marketing positioning in the short-DXY, long EUR-trade. I still see DXY grinding lower as this works itself ou, at least or until volatility returns in earnest.

On that question we turned to the “K”, via JPM:

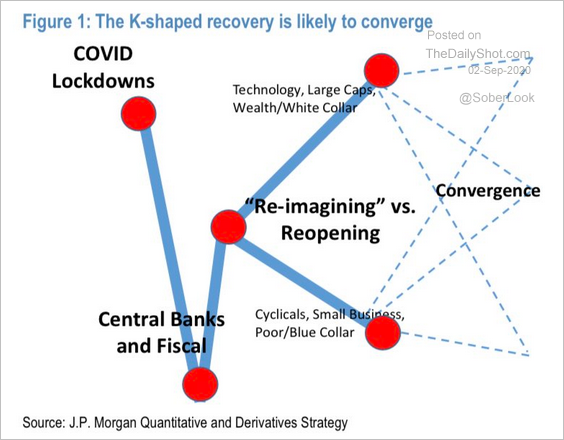

Exactly which convergence will it be? If it is the strong tech and cyclicals catch-up then I see DXY still falling and the Australian dollar rising. If it is tech selling as cyclical catch-up then I see DXY falling and the Australian dollar rising even more. If it is tech bust meeting flattened cyclicals then the safe-haven trade returns and the Australian dollar is crushed.

The probabilities are on a continuum but for ease let’s give each a one-third chance.

Meaning the most likely direction for the AUD is still up in the K-shaped recovery unless or until the RBA works it out and changes the game.