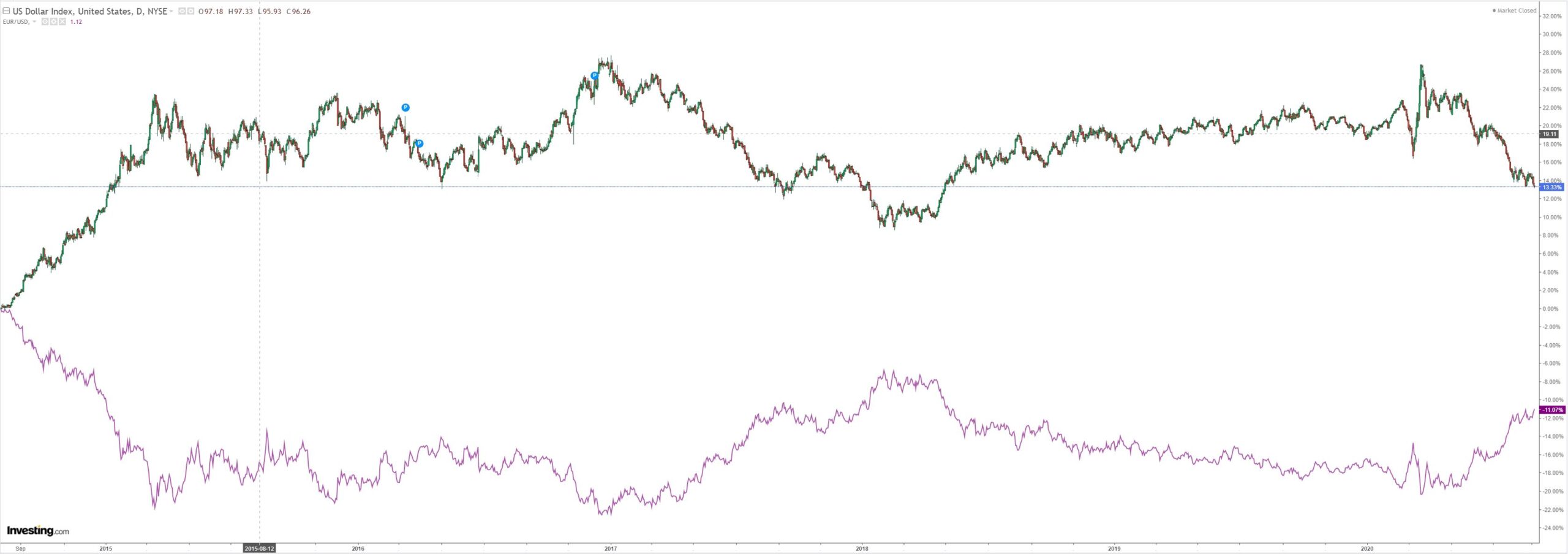

DXY is at new lows and EUR new highs:

We all know what that means for the Australian dollar:

Gold was bid again but couldn’t hold:

WTI is closing on Brent:

Base metals were strong:

Miners firm:

But EM stocks fell:

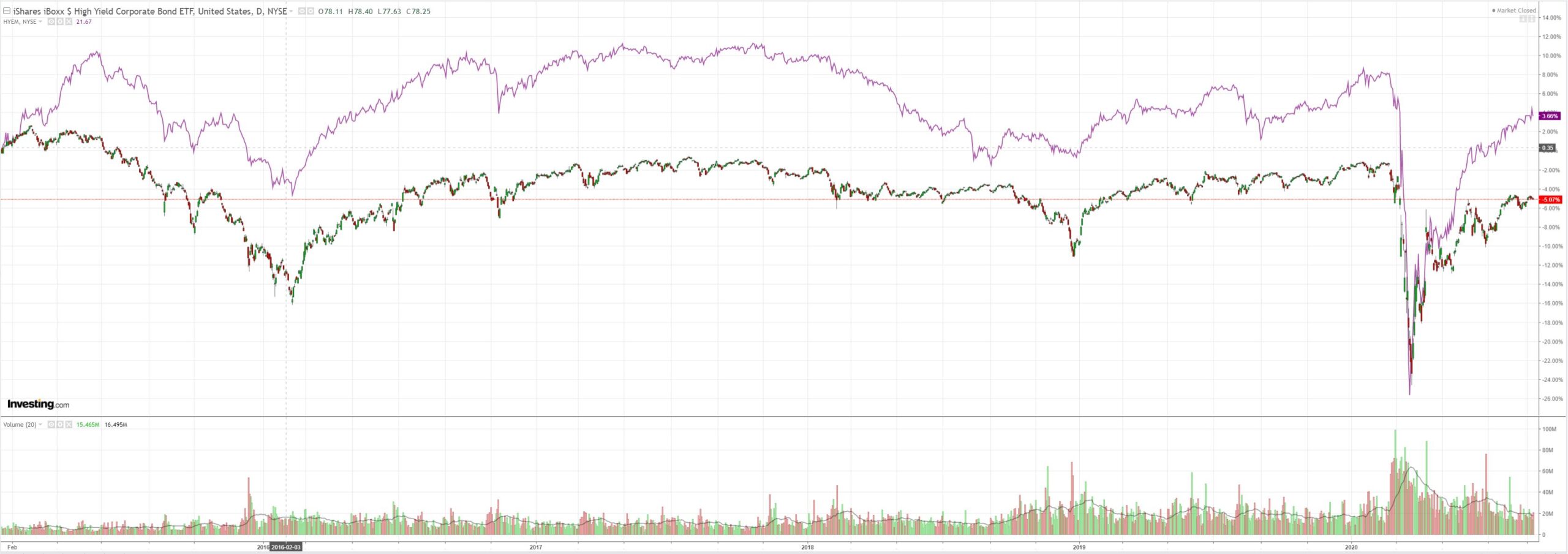

And junk:

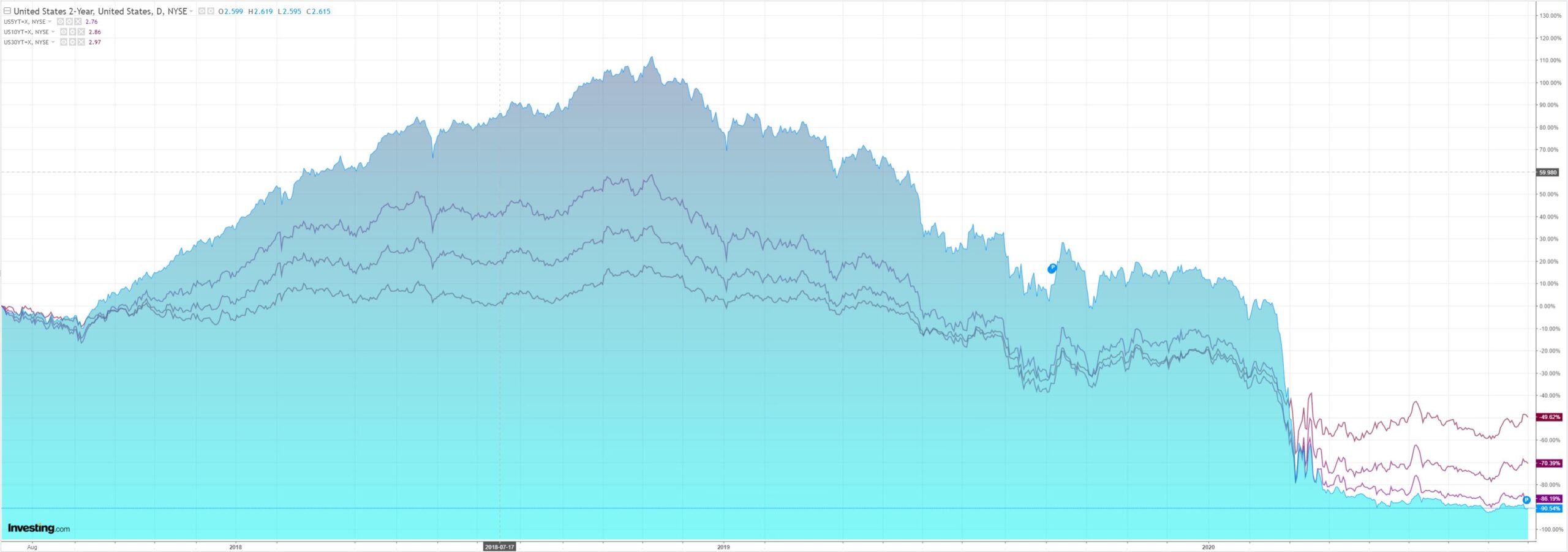

US yields faded the Fed:

Thre Nasdaq blowoff continues:

Westpac has the data wrap:

Event Wrap

The Dallas Fed manufacturing activity survey rose from -3.0 to +8.0 in August (vs 0.0 expected).

Germany’s CPI inflation rate fell 0.1% in August (vs 0.0% expected, -0.5% prior), for an annual pace of 0.0%.

A plan to sell the US operations of TikTok was thrown into jeopardy after China asserted authority over a deal already under scrutiny by the Trump administration. China’s commerce ministry added speech and text recognition and personalised recommendations to a list of products that require approval before they’re sold overseas.

Event Outlook

Australia: It’s a busy day on the event calendar. The Covid shock will continue to filter through slowly to house prices, the August CoreLogic home value index expected to fall 0.6% after a 0.8% decline in July. Dwelling approvals slumped in H1; Westpac and the market expect momentum to improve on a HomeBuilder boost in July (prior: -4.9%, market f/c: -1.0%, Westpac: 3%). Westpac expects net exports to add 1.2ppts in Q2 as imports fall faster than exports. The trade surplus will contribute to a move higher in the current account balance (prior: $8.4bn, market and Westpac f/c: $13.0bn). Westpac expects brisk growth in public demand to continue in Q2, gaining 1.5%. The RBA is expected to remain on hold and highlight uncertainties over the outlook.

NZ: July building permits are expected to see a pullback in multi-unit consents after June’s large increase (prior: 0.5%, Westpac f/c: -10.0%).

China: The Caixin PMI will contribute to the run of positive manufacturing data (prior: 52.8. market f/c: 52.5).

Asia: Markit manufacturing PMIs will also be released for Malaysia, Indonesia, Korea, Taiwan and India.

Eurozone: The August Markit manufacturing PMI will confirm production is improving (final estimate: 51.7). Job loss concerns are however mounting as government support begins to drop off; the unemployment rate is expected to lift from 7.8% to 8.0% in July. Inflation is expected to rise slightly from -0.4% to 0.0% in August.

US: Growth in output and new orders will be reflected in the August Markit manufacturing PMI read (final estimate: 53.6). ISM manufacturing should lift slightly from 54.2 to 54.5 in August. Construction spending is set to jump in July as the sector begins to recover (prior: -0.7%, market f/c: 1.1%). FOMC’s Brainard will speak on the New Monetary Policy Framework (03:00AEST).

There’s not much more to add today. DXY is falling with fakeflation and the hopeless RBA has strapped the Australian dollar to a rocket that gets further and further from its underlying economy. With the meeting today, what expect more stupid can we expect?