By Gareth Aird, head of Australian economics at CBA:

Key Points:

The 2020/21 Budget is scheduled for release at 7.30pm (AEST) 6 October.

More stimulus is expected to be announced, including personal income tax cuts, infrastructure spending and a business investment allowance.

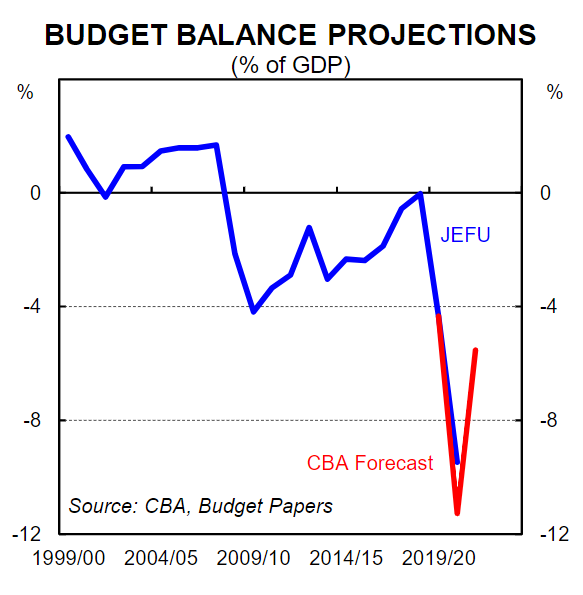

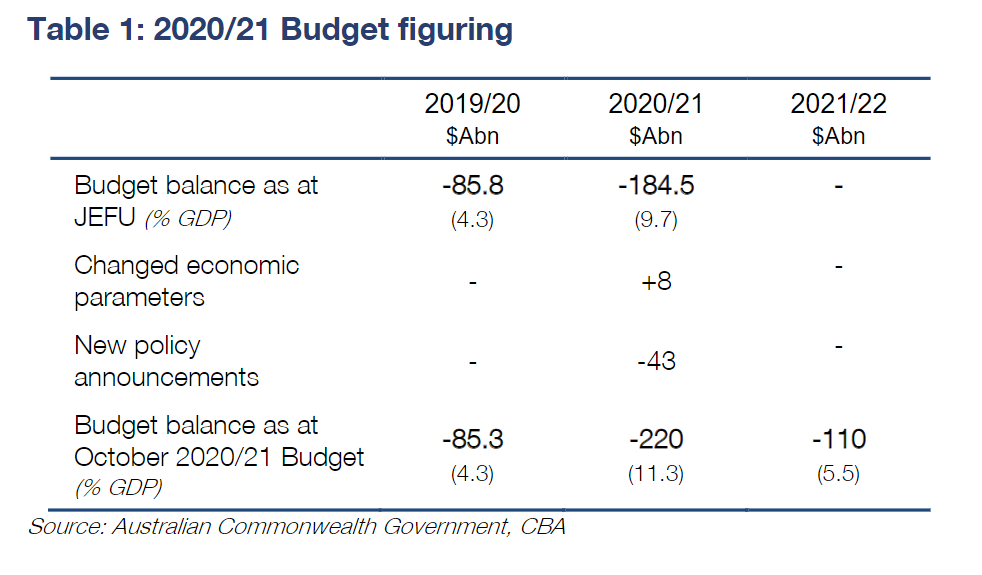

Our point estimate for the underlying cashdeficit in 2020/21 is $A220bn (11.3% of GDP).

Overview

Back in March the Government took the decision to defer the originally scheduled May 2020/21 Budget to October due to the COVID-19 pandemic. Since then the Australian economy has been through an extraordinary period. Output collapsed in Q2 20 but has recovered some ground in the September quarter. And employment has endured a similar roller coaster ride. Economic downturns have big impacts on public finances. And the unique nature of this recession coupled with the Government’s massive fiscal packages mean that the Commonwealth Budget has taken an almighty hit. Australia is not alone and big budget deficits are very much the dominant theme around the world right now.

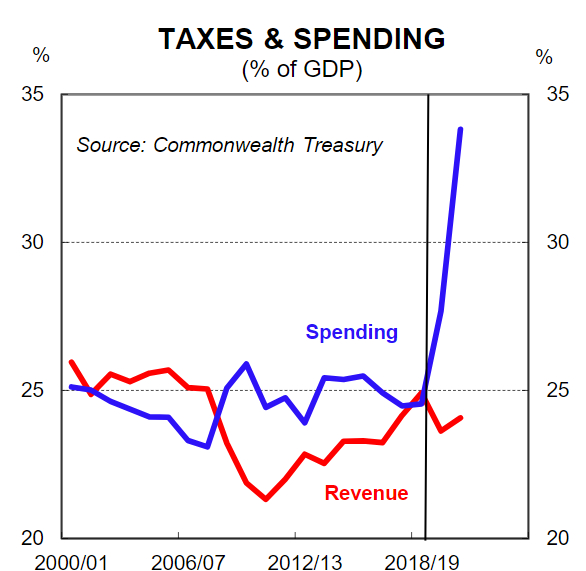

How big are Australia’s deficits?

The 23 July Economic and Fiscal Update (JEFU) contained updated estimates for the fiscal position in 2019/20 and 2020/21. Those estimates are the starting point for which we derive our forecasts for the budget deficit in 2020/21based on parameter changes, announced policy changes and expected policy changes.

Parameter changes primarily relate to changes in economic forecasts, particularly nominal GDP which drives the revenue side of the equation, as well as the level of unemployment which underpins welfare payment forecasts. The news around nominal GDP has improved since the JEFU.

First, the price of iron ore has risen over the past few months whilst Treasury assumed the price of iron ore would fall. The swing is significant and should see tax receipts boosted by around $A5bn in 2020/21. Second, despite the lockdown in Victoria household consumption nationally has stepped up in Q3 20.We suspect the lift in spending will have exceeded the Treasury’s implied quarterly real GDP profile. This will mean higher nominal GDP. Third, growth in hours worked will have been stronger over the September quarter than Treasury’s estimates, pointing to a likely increase in personal tax revenue. Overall our fiscal model is pointing to a revenue upgrade in 2020/21 of ~$A8bn.

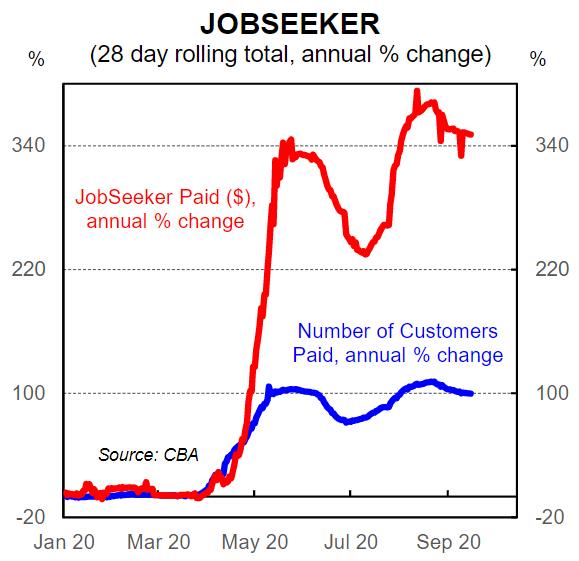

On the expenditure side, parameter revisions are likely to be negligible in 2020/21 compared to the JEFU. Instead the bulk of the expected increase in expenditure this fiscal year will bedriven by: (i)announced policies since JEFU, in particular around the easier eligibility for JobKeeper due to the lockdown in Victoria; (ii) additional policies that will be announced on Budget night and are expected to include more money for infrastructure and a business investment allowance. Personal income taxes look to be a story for the 2021/22 fiscal year.

Our point estimate in 2020/21 is for an underlying cash deficit of $A220bn(11.3% of GDP). That would bean increase of $A35bn from the projected deficit in JEFU.

The budget balance should look a lot better in 2021/22. But it will still be deep in the red and won’t resemble anything remotely like the $A8.4bn surplus projected in the 2019/20 MYEFO (latest available).

A bounce in nominal GDP in 2021/22 will see revenue lift, notwithstanding new policy announcements. Expenditure will fall as a share of GDP in 2021/22 due to the expiry of some of the large stimulus programs. On the policy side we expect the already legislated “stage two” July 2022 income tax cuts to be pulled forward to boost demand in the economy. They are estimated to “cost” around $A15bn per annum which is another way of saying the tax cuts would inject $A15bn into the economy. This would result in more spending, economic activity and therefore tax receipts so the true “cost” to the budget is lower. Pulling forward the tax cuts also makes sense given we will see very little nominal wages growth over the next few years and we expect real wages growth to turn negative. If “stage two” tax cuts are to be pulled forward the most likely start date is 1 July 2021. We are less sure that the “stage three” July 2024 tax cuts will be pulled forward, but there is a small chance that it happens. More infrastructure spending also looks set to be in store in 2021/22. Some further policies to support demand are also likely as is a decision on a permanent lift to JobSeeker.

Clearly we are largely shooting in the dark in forecasting the underlying cash deficit in 2021/22, but we wouldn’t be surprised to see the Government forecast a deficit in the ballpark of $110bn (5.5% of GDP).

The projected deficits in 2022/23 and 2023/24 are of little consequence at the moment given the huge amount of uncertainty about the path of the economy. Table 1 below details the figuring behind what we expect to see in the Budget.

Bigger picture

Overall we expect a stimulatory budget and we do not expect any austerity measures to be introduced over the next few years. The Government has stated that the focus over the near term will be three fold:

(i) allowing the automatic stabilisers to work freely to support the economy;

(ii) providing temporary, proportionate and targeted fiscal support, including through tax measures, to leverage private sector jobs and investment; and

(iii) pushing ahead with structural reforms.

The Government will not shift to restoring the fiscal position until the unemployment rate is comfortably back under 6%. We do not expect the Government to forecast an unemployment rate below 6% until 2022/23.

The unique nature of the economic shock coupled with the policy response means that it’s important to still think about the limits of any stimulus at the moment. Right now it is largely government restrictions on households and businesses to control the spread of COVID-19 that are holding back economic production and jobs growth. Confidence in health outcomes is also playing a role.

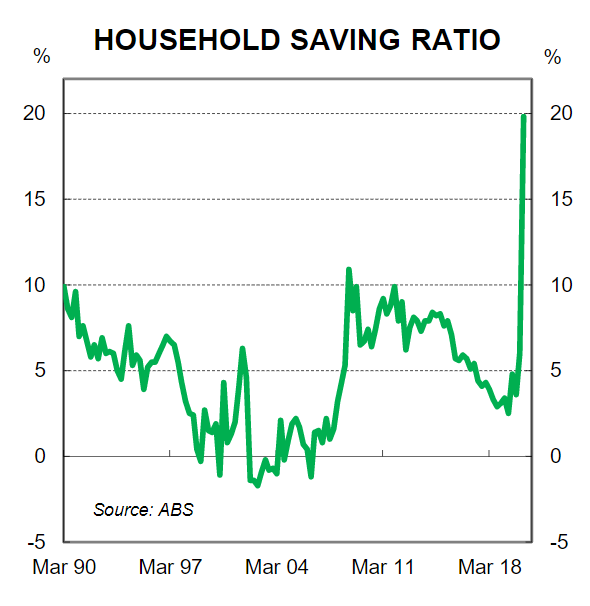

Income support has been massive, but no level of income support can propel GDP and employment back to pre-COVID levels while there are still restrictions on activity, particularly in Victoria. It is akin to tapping the accelerator while the handbrake is still on and largely explains why savings have surged. Households simply cannot spend money on a range of goods and services at the moment.

Finally we remind readers that the RBA October Board meeting is also on 6 October. We expect monetary policy to be left on hold.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.