CBA’s head of Australian economics, Gareth Aird, asks this question today:

The economic consequences of the COVID-19 pandemic will be long lasting.

Labour market slack will remain elevated for many years which will supress wages growth and see monetary policy remain highly accommodative for an extended period of time.

Private sector credit growth will be very weak and net overseas migration is not expected to return to pre-COVID-19 levels.

Budget deficits will remain large as far as the eye can see and public debt to GDP will continue to climb.

Over time, pressure will intensify to formally re-examine the role and relationship of fiscal and monetary policy as it pertains to monetary financing.

Overview

Economists are having a torrid time trying to forecast the economic outlook as a host of unusual dynamics play out. Many traditional economic models have been of little use over recent months as policymakers globally continue to grapple with the trade-off between limiting the spread of COVID-19 and the negative impact on the economy from restrictions on what people can and can’t do.

We have made material revisions to our forecasts on several occasions in a short space of time as new information on the spread of COVID-19 shifts the economic outlook. We are not alone in doing so. And no doubt more revisions will be forthcoming. But whilst the shorter term picture is highly uncertain and heavily dependent on the ability to control the spread of COVID-19, there are some medium to longer term implications from the pandemic that are less ambiguous.

In this note we take a step back from our quarterly profile for the economy to look at the longer lasting impacts from the pandemic on the economy. We identify five medium term economic implications from the COVID-19 pandemic. And we discuss how the longer lasting economic effects will intensify the debate on the future role and relationship of fiscal and monetary policy as it pertains to monetary financing. Any shift towards monetary financing would significantly change the outlook for inflation and interest rates –it’s a game changer.

(i) Elevated labour market slack and weak wages growth

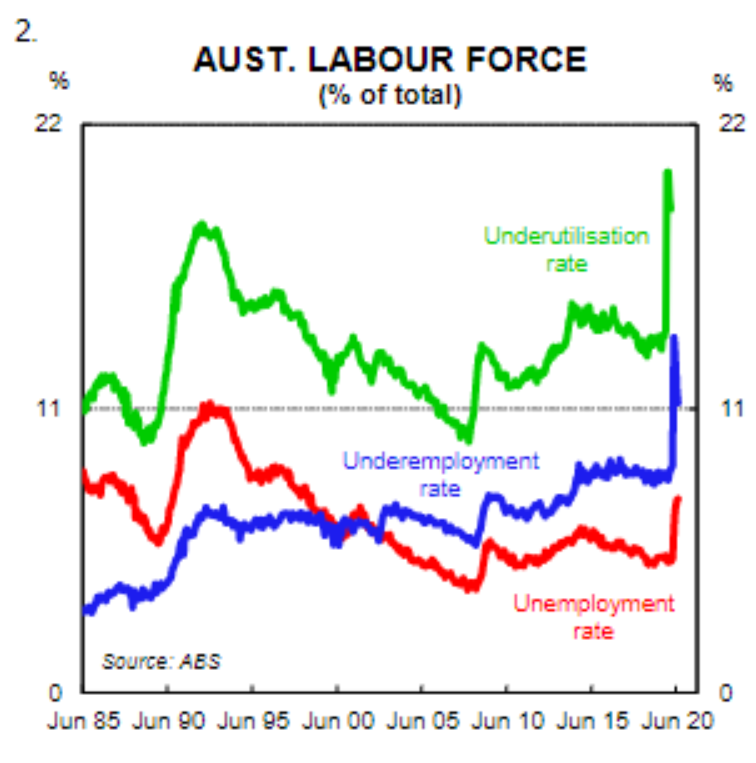

The COVID-19 pandemic has had a very substantial impact on the Australian labour market. Employment has contracted sharply. And many workers have had their hours cut. As a result, labour market slack has risen sharply. The underutilisation rate, which is the broadest measure of labour market slack and is simply the sum of the unemployment and underemployment rates, hit its highest level on record in May and has barely moved lower since (chart 2).

History shows that labour market slack tends to rise very quickly during a recession but takes a long time to recede. The 2020 pandemic-induced recession will be no different in that regard. It will take time for the economy to heal and the recovery will be drawn out. The sad truth is that the supply of labour will exceed the demand for workers for a long time. That means labour market slack will remain elevated for several years.

There has historically been a close inverse relationship between underutilisation and wages growth. The relationship is simple -as underutilisation rises (falls) wages growth falls (rises). It is all about bargaining power. Elevated labour market slack reduces the capacity of workers to negotiate a pay rise.

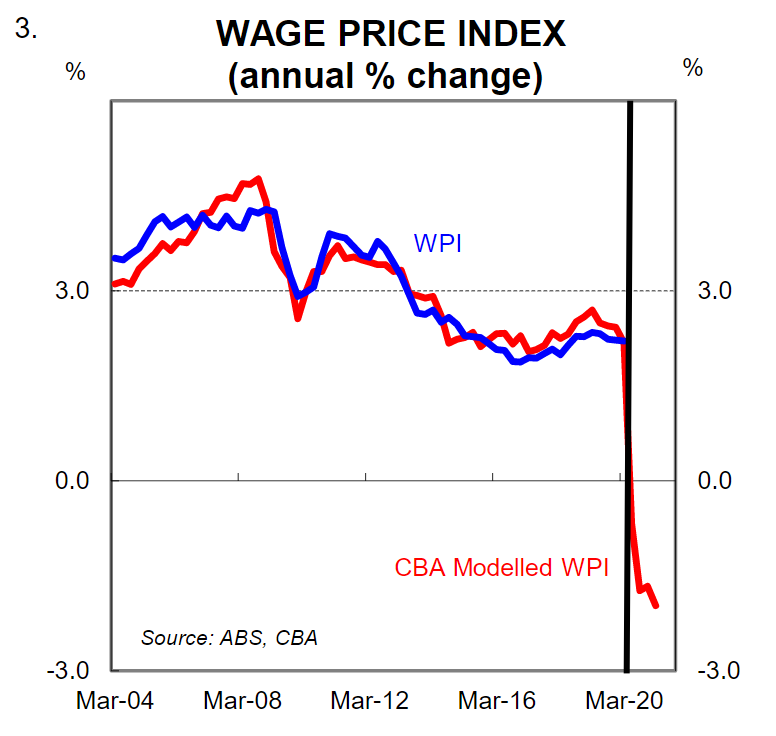

Our wages model, based on underutilisation and inflation expectations, has very accurately predicted the path of wages growth over recent years. But we can now put our model in the closet for a few years as the current level of labour market slack coupled with inflation expectations suggests wages growth stepping down to -2%/yr! (chart3). Clearly that won’t happen as wages are sticky downwards and pay cuts are very rare. But our model illustrates just how big the shock to the labour market has been and how an extended period of very, very low wages growth is the inevitable consequence of such a surge in underutilisation. The Q2 20 Wage Price Index(WPI) was a taste of things to come. The private sector WPI grew by just 0.1% after rising by 0.5% each quarter over the previous five years.

(ii) Very low interest rates

We expect domestic inflation pressures to remain weak primarily because spare capacity in the labour market will keep a lid on wage costs. Our forecast profile has consumer price inflation generally sitting above wages growth, meaning an extended period of(modest) real wage declines. Notwithstanding, both consumer price inflation and wages growth are expected to be low for a long time unless the fiscal and monetary policy framework changes (more on that later).

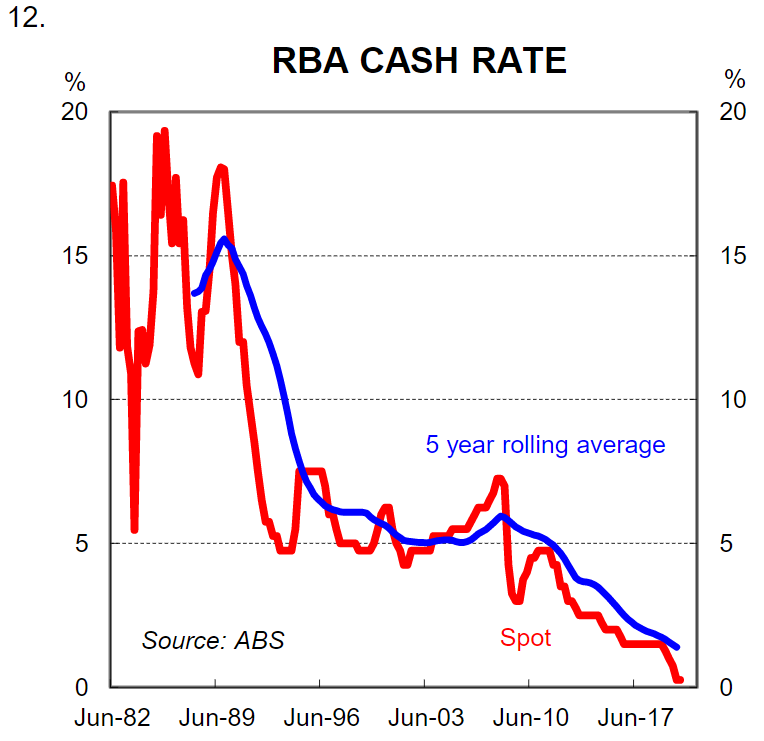

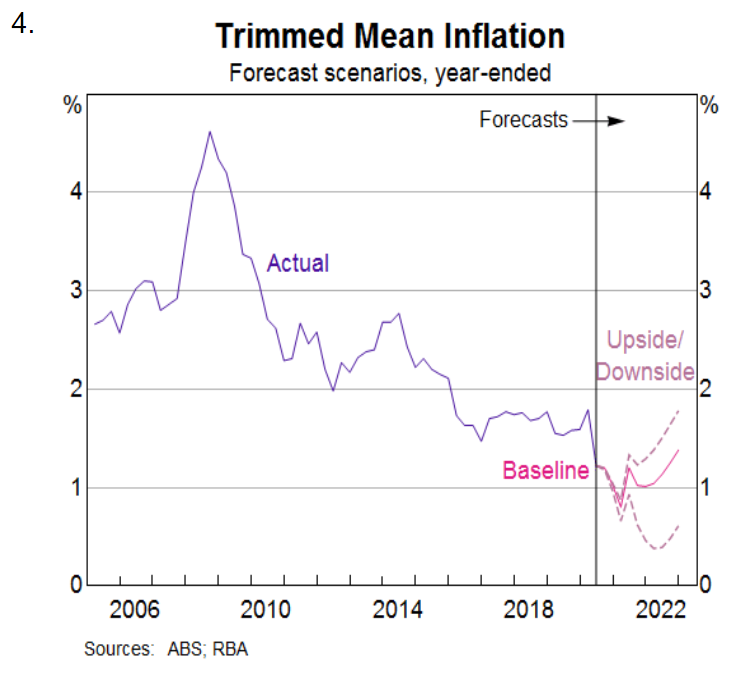

The RBA’s latest forecasts in the August Statement on Monetary Policy put underlying inflation at or below 1½%/yr until end 2022 (end of the forecast period – chart4). Normally such a forecast for inflation would imply that more official interest rate cuts are coming. After all the RBA has an inflation target of 2%-3%pa over the cycle. But the simple reality is that with a cash rate of just 0.25% any further meaningful rate cuts would take the cash rate into negative territory. And that doesn’t look likely to happen. The RBA has repeatedly said that in Australia negative rate cuts are “extraordinary unlikely” because, “they can cause stresses in the financial system that are harmful to the supply of credit, and they can encourage people to save rather than spend”.

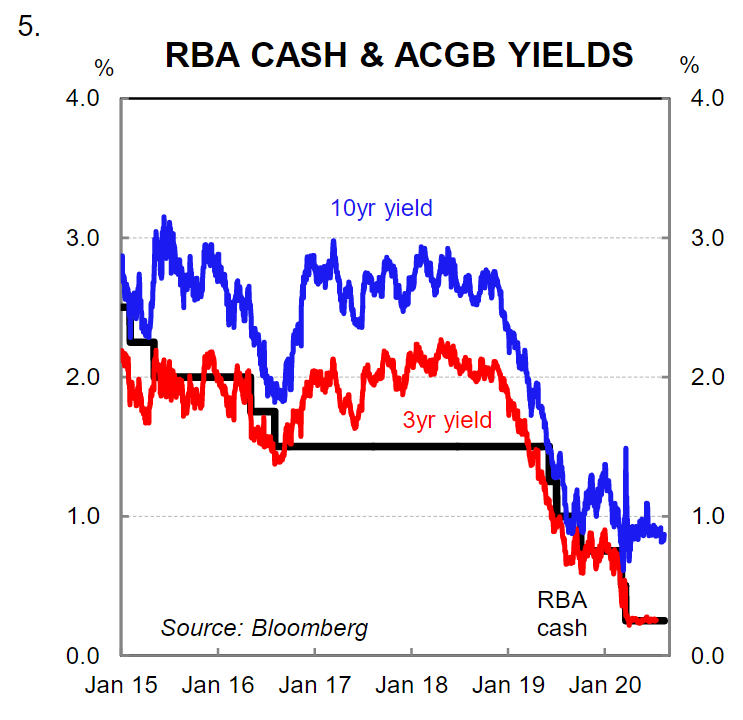

In any event there is virtually no prospect of any lift in the cash rate for many, many years. In the RBA’s own words, “the Board will not increase the cash rate target until progress is being made towards full employment and it is confident that inflation will be sustainably within the 2–3 per cent target band”. That statement is code for ‘a record low cash rate is here to stay for a very long time’.

(iii) Very weak private sector credit growth

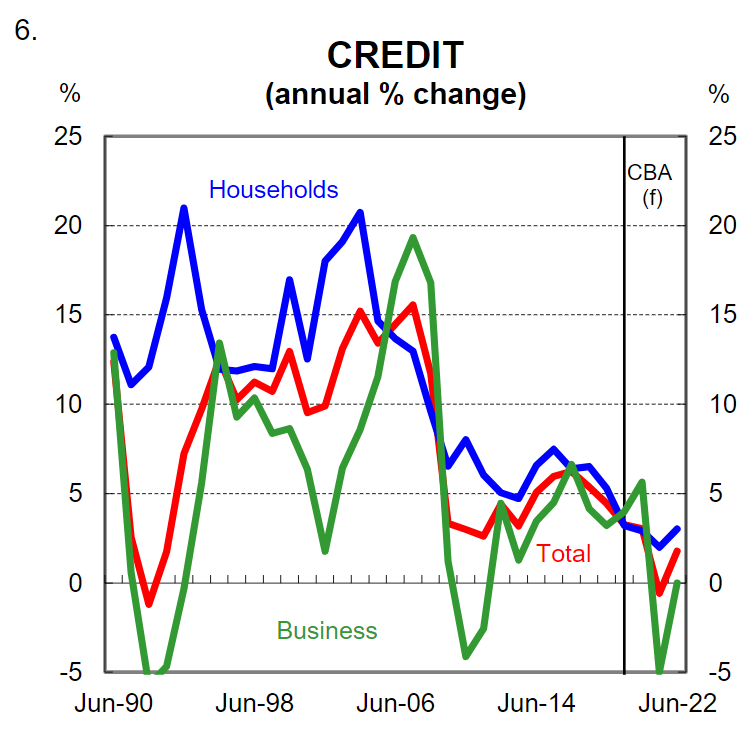

Large economic downturns have a long lasting impact on the demand for credit. History shows that a big contraction in private demand leads to an even bigger decline in business investment and the stock of business credit falls. In the recession of the early 1990s, the stock of business credit contracted by ~10% over a two year period. Personal credit also tends to fall in a downturn as a ‘saving-rather-than-spending’ mindset takes hold of households. RBA credit aggregates indicate these trends are already underway.

The dynamics around housing credit are less certain in a big recession. Housing credit may not necessarily contract. But we are confident it will be very weak. The expression ‘this time is different’ is highly relevant for the outlook for housing credit. The RBA cannot stimulate credit demand by further lowering interest rates as it has done in the past.

Business credit is generally less sensitive to interest rates than housing credit. But housing credit is highly sensitive to changes in the cost of money. Given the RBA has no real capacity to reignite credit growth via rate cuts we are comfortable with our medium term view that credit growth will remain soft (chart 6).

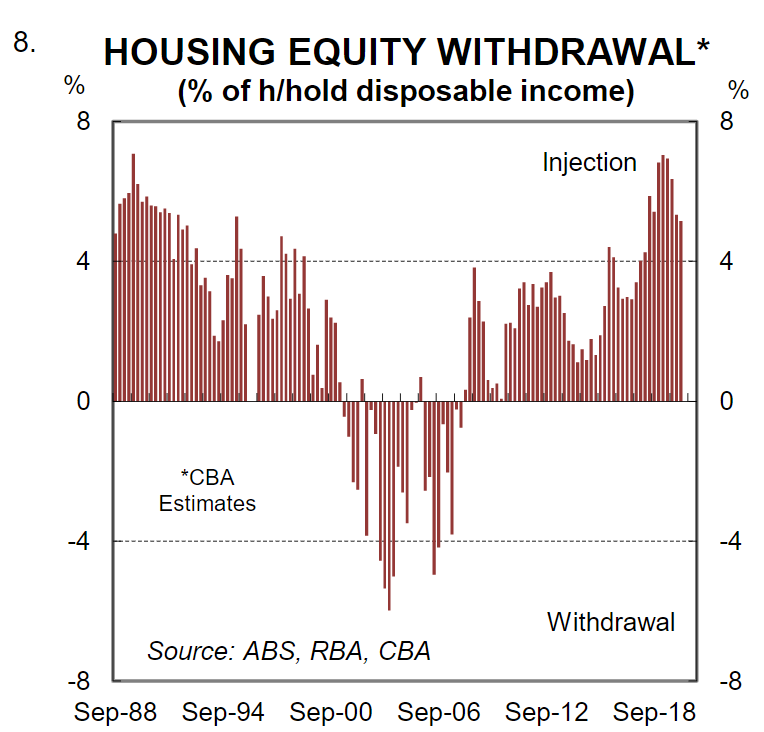

As the economy recovers new lending for housing will lift. But working the other way will be a heavily indebted household sector that is expected to retain a deleveraging mindset. Even before the COVID-19 pandemic households were using lower interest rates to speed up debt repayment (i.e. deleverage). And housing equity injection(as opposed to withdrawal)was elevated as a share of household disposable income (chart 8).

(iv) Lower net overseas migration

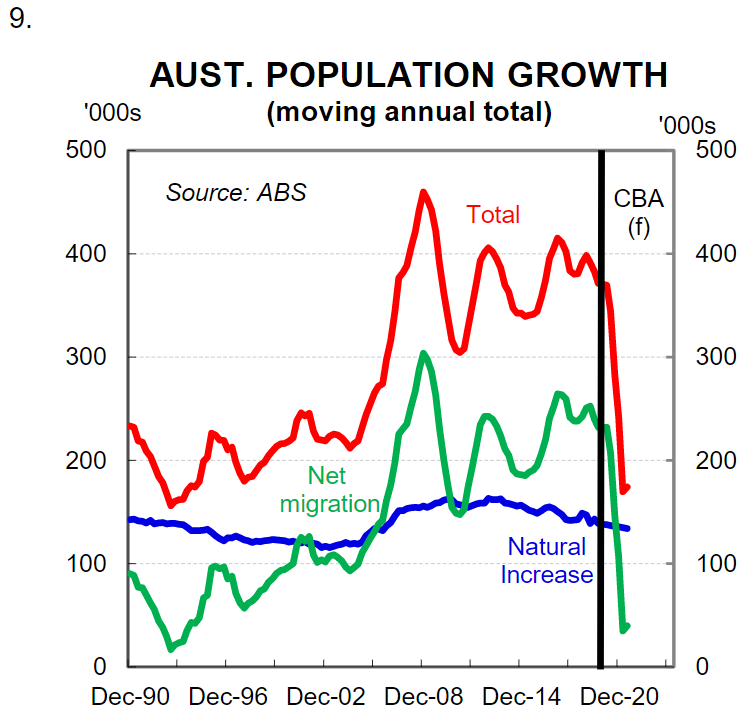

Net overseas migration (NOM) and in turn population growth will decline significantly over the short run due to the COVID-19 pandemic. The Government expects NOM to fall by ~30% in 2019/20 and by ~85% in 2021/22. This means that there is an expected shortfall of around ~310k in NOM over the next 18 months compared to original estimates. Population growth will slow sharply from 1.5% to 0.7%/yr over that period. We published a detailed research note in May on the impact of lower NOM on the economy (see here).

Clearly nobody at this stage knows when the international borders will be reopened and when NOM will start back up. But we don’t think it’s simply a matter of turning the tap back on to the pre-COVID level of NOM. As covered earlier in this note, the Australian labour market will have an elevated level of slack for many years. That means that there will a lot of Australian residents who are either unemployed or underemployed. Basically a much higher than usual proportion of the population will be looking for work in some capacity.

Both politically and economically it is not the time to boost labour market supply when the supply of labour already exceeds the demand for labour. There will be little evidence of wide spread skill shortages if labour market underutilisation is high. Therefore we think that it is more likely than not that when the borders reopen NOM is materially lower for several years than it was before the pandemic.

(v) Big budget deficits and rising public debt

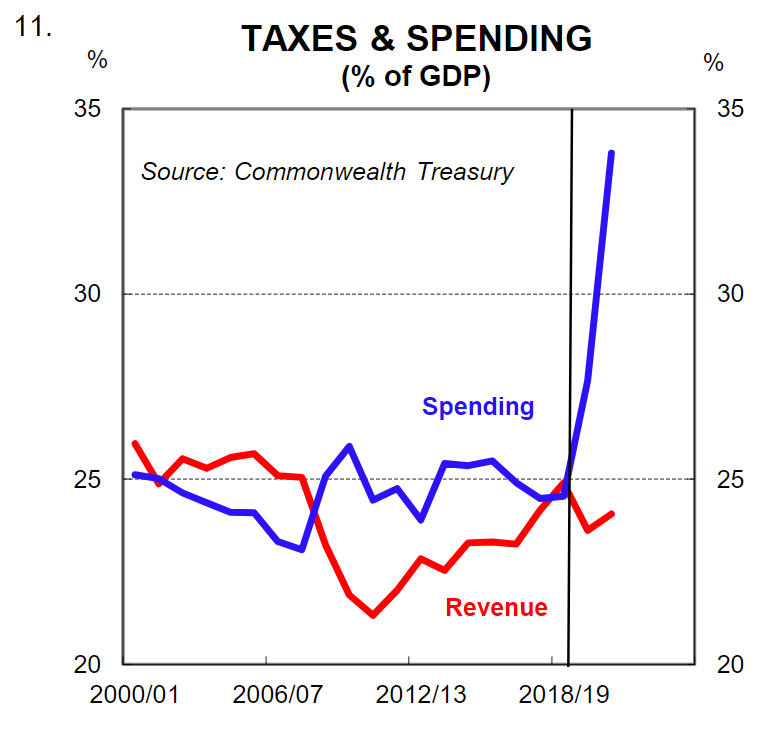

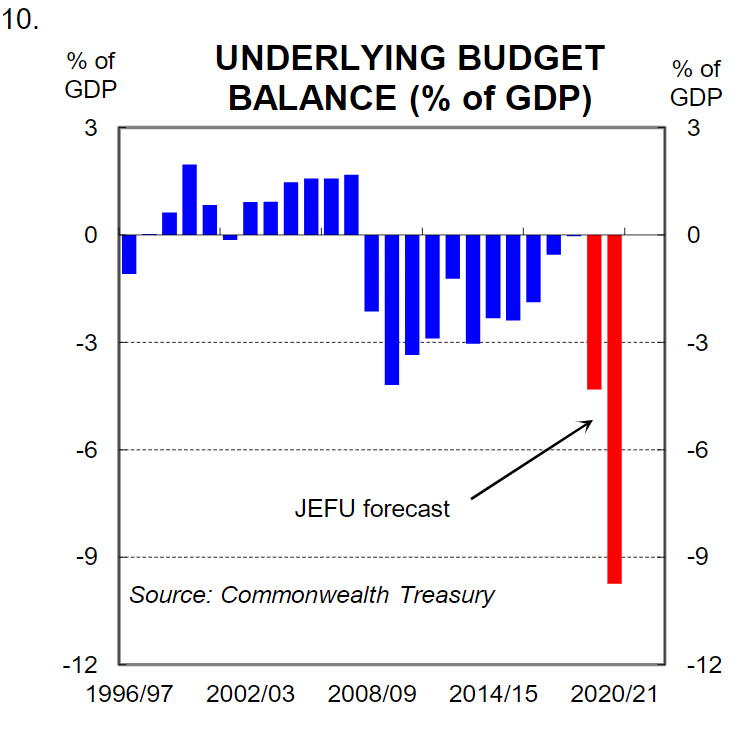

One of the obvious causalities from the COVID-19 pandemic is the Commonwealth’s fiscal position. At the beginning of the year the Government was clinging to hopes of a wafer thin surplus in 2019/20 followed by a string of small surpluses over the forward estimates period. Fast forward to the July Economic and Fiscal Statement (JEFU) and the Government projected a deficit of $A86bn (4.3% of GDP) in 2019/20 and $A185bn (9.7% of GDP) in 2020/21 (chart 10). The deficit this fiscal year will end up being bigger than what was projected in JEFU because of the stage 4 lockdown in Victoria.

The huge negative economic shock caused by the COVID-19 pandemic means a big hit to revenue because of lower nominal GDP (primarily lower tax receipts) and an even bigger lift to expenditure due to higher welfare payments and fiscal stimulus. The upshot is a big lift in government spending as a share of GDP, massive budget deficits and rising public debt (chart 11 & 12).

To be clear we are certainly not suggesting that the policy decision to run big budget deficits is the wrong one. On the contrary. The Government is doing what should be done in the circumstances. A big economic contraction coupled with limited monetary policy firepower and private sector deleveraging means a large fiscal injection is paramount. Indeed more can and should be done. We continue to advocate for bringing forward the already legislated income tax cuts (that are due to start on 1 July 2022) to cushion the impact on households and spending from anaemic nominal wages growth and high underemployment.

Even as the economy recovers there is no case for fiscal repair while labour market slack is elevated and there is a large output gap. We suspect that the Government shares this view and this means that big budget deficits and rising public debt will be with us as far as the eye can see.

The fiscal and monetary framework will need addressing –calls for monetary financing will intensify

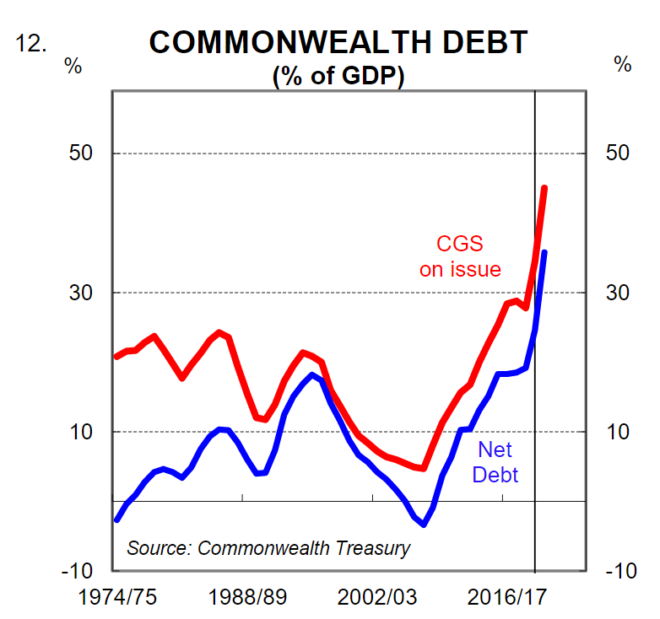

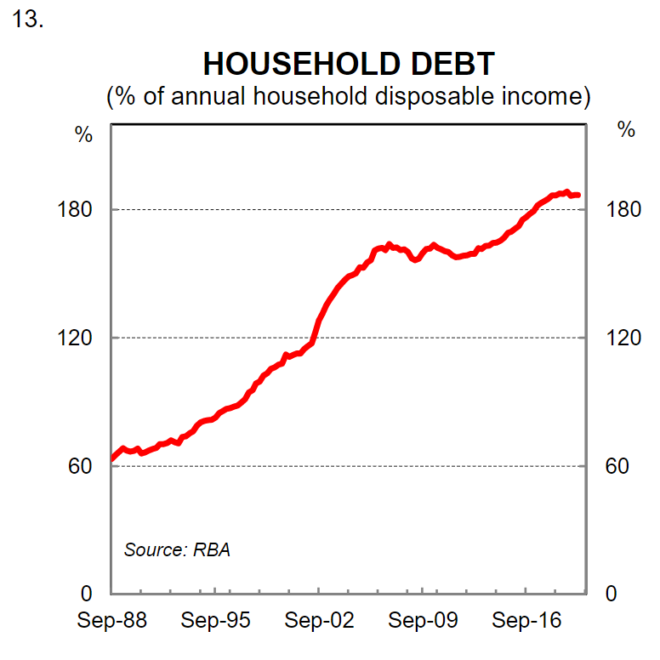

The timing of the pandemic-induced economic downturn is important to note. It arrived when interest rates were already close to zero and had been on a structural decline for decades(chart 12). And it arrived when household debt to income was at its record high (chart 13). In essence it arrived at the end of the long term debt cycle.

So we now find ourselves in a situation of elevated labour market slack, very weak wages growth, very little private sector credit growth, record high household debt, big budget deficits, ballooning public debt and perhaps most importantly, negligible capacity to stimulate growth by lowering interest rates.

So against that backdrop, what next? How do we get back to a steady state of trend growth, full employment, inflation within the RBA’s target and the budget on a sustainable path? What levers can be pulled from here and when will they be pulled? How long can the RBA forecast below target inflation while leaving monetary policy unchanged and credibly claim to have an inflation target?

The short answer is that we do not know what policymakers will decide to do. Plenty of fiscal stimulus has been injected into the economy. And the RBA has committed to anchoring the 3 year Australian Commonwealth Government Bond (AGB)yield at 0.25% by buying government bonds in the secondary market. But that doesn’t address the medium to longer term issues around public and private debt, interest rates, inflation and fiscal and monetary policy.

We no longer have the interest rate lever available to give households debt relief when a negative shock comes along. And we can’t stimulate the interest rate sensitive parts of the economy with more rate cuts. In addition, the previous narrative around debt and deficits no longer looks fit for purpose.

In short, we are inching towards a new paradigm that will involve some form of monetary financing at some point in the future (i.e. a direct transfer of money from the central bank for government to spend). The bottom line is that the system as we know it will need to be reset and the printing press will be part of that reset.

The RBA Governor in a speech on 7 July hosed down the idea of monetary financing and said that there is no ‘free lunch’. Specifically he stated that, “suppose that the additional government spending is successful in stimulating the economy and this starts to push inflation up. At some point, interest rates would need to be increased to avoid inflation rising too far. If this lift in interest rates did not occur, inflation would rise, perhaps to a very high level. In this case, it would be through the inflation tax that the community pays for the extra government spending.” It seems ironic to us that the Governor would consider higher inflation and higher interest rates as “costs” when higher inflation and a normalisation in interest rates is what the RBA has been pursuing for years!

We are not proposing or advocating that monetary financing be taken up imminently, particularly when the current arrangement of the Government issuing bonds in the primary market and the RBA a willing buyer in the second market is working well. But we are raising these issues because at some point down the line the conversation will inevitably shift towards some form of monetary financing to put fiscal and monetary policy on a sustainable longer term footing. And when that happens the outlook for inflation, income, debt and many asset markets will shift considerably.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.