AMP chief economist, Shane Oliver, has updated his forecasts for Australia’s property market, predicting peak-to-trough falls of 10% to 15% nationally, led by Melbourne where prices will crash between 15% and 20%:

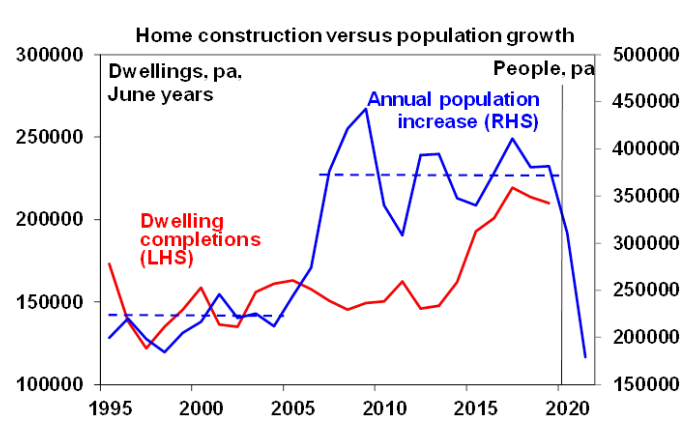

Further falls in home prices are likely. High and still rising unemployment (with “true” unemployment absent government support measures estimated to be just above 11%), the collapse in immigration which has reduced underlying dwelling demand by around 80,000 dwellings a year (see the next chart which shows the collapse in population growth relative to housing completions) and the depressed rental market will likely combine to drive weak housing demand and increased forced sales. JobKeeper, increased JobSeeker, bank payment holidays and other support measures have so far helped head off a sharp collapse in prices but the market has still weakened anyway and we expect an acceleration in falls as support measures start to be tapered from the December quarter. Sydney and Melbourne are the most vulnerable given their higher dependence on immigration, higher debt to income ratios, higher house price to income ratios and greater investor penetration.

The resurgence of coronavirus cases and the renewed negative impact of this on the economic recovery via Melbourne’s stage 4 lockdown, the reversal of some reopening measures in the rest of Australia and reduced confidence has caused us to revise our base case for the decline in national average property prices down to a 10 to 15% top to bottom fall (from a 5 to 10% fall). However, this masks a wide divergence between cities with Melbourne likely to see a 15-20% decline (of which its already fallen 3.5%) partly reflecting the bigger hit to its economy from its ongoing lockdown, Sydney prices likely to see a 10-15% decline (of which its already fallen 2.1%) whereas Adelaide, Brisbane & Hobart are only likely to see falls around 5% and Canberra prices are likely to be flat to up. Perth looks a bit more fragile despite having seen a 22.3% decline from its 2014 high and so prices there are likely to fall 5-10%.

However, if the resurgence in coronavirus cases in Victoria morphs into a broader “second wave” of cases across Australia necessitating a renewed economy wide lockdown and a renewed broad based downturn in the economy then the likelihood of a 20% plus decline in prices will escalate. We are also assuming more government stimulus to be announced in the months ahead – but if it’s not forthcoming it would also add to the risk of a sharper fall in property prices than in our base case.

Good analysis. Let’s recall the gale force headwinds facing the Australian property market, especially Sydney and Melbourne:

Stubbornly high unemployment and falling household disposable incomes once emergency income support and early superannuation access is reduced from October.

Collapsing immigration, particularly into Melbourne and Sydney.

Rising dwelling supply and falling rents.

Ending of mortgage repayment holidays, currently assisting nearly 500,000 borrowers holding $195 billion worth of mortgages (11% of total outstanding).

Tightening credit availability (despite low rates) as lenders become increasingly concerned about borrowers’ ability to repay.

Advertisement

The big risk is that a significant share of Australia’s 1.3 million negatively geared investors, sandwiched between falling property prices and rents, sell en masse.

If this occurs, then Australia’s property market could become caught in a feedback loop of forced sales and falling prices.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.