While the superannuation industry complains incessantly about the $30-plus billion being stripped out of the system due to the Morrison Government’s early release policy, it is conspicuously silent about the $36 billion in fees stripped from superannuation accounts.

On this front, Harry Chemay – co-founder of Clover.com.au – has penned an excellent article at Michaelwest.com.au dissecting Australia’s wasteful, inefficient and inequitable compulsory superannuation system:

If superannuation didn’t exist, and you went to the Treasurer of the day proposing a retirement system that would require 10 times the operating cost of running the Australian Taxation Office but wouldn’t deliver a net benefit to the Commonwealth budget for at least 50 years, you’d get short shrift.

If you further proposed that same retirement system primarily be a vehicle for the highly paid to supercharge their accumulation of wealth through tax concessions worth some $36 billion each year, you’d probably be expected to be shown the door.

But this is the system we have ended up with today, nearly 30 years on from Paul Keating’s defining speech outlining his vision for Australia’s retirement system.

The annual cost of administering the super system, and investing for the nation’s 16 million account holders, is in the order of $32 billion.

The ATO runs on the smell of an oily rag by comparison – with an annual budget of about $3.4 billion, a tenth of the super industry. On that budget the Tax Office oversees the tax affairs of 12 million individuals, 4.2 million small businesses, 865,000 employers, 36,000 large multinational entities, 35,000 registered tax agents, 201,000 not-for-profits and all self-managed superannuation funds (SMSFs).

Either the ATO is comically underfunded, or the super industry is obesely inefficient. Very possibly both…

The system feeds on $120 billion in annual contributions, 80% via employer payments…

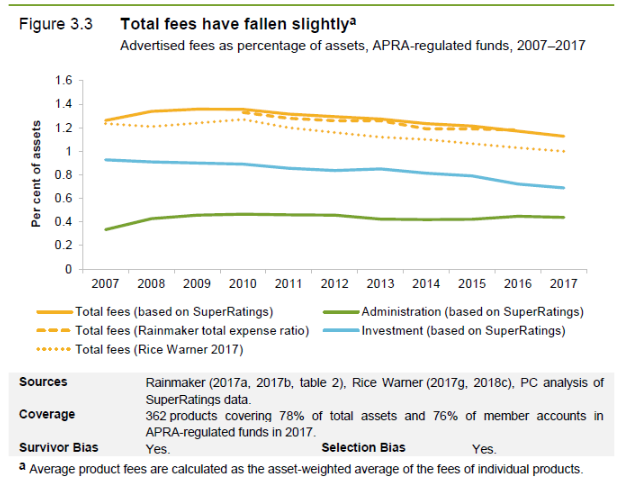

The direct cost to members is estimated at about $32 billion a year – 1.1% of account balances, plus annual insurance premiums of some $9 billion.

These costs appear remarkably resistant to the benefits of scale, as the chart from the 2017/18 Productivity Commission review into super indicates…

Superannuation has been an absolute boon for the highly paid to turbocharge their accumulation of wealth… [They] take advantage of a raft of super tax concessions – the cost of which exceeds $36 billion annually…

As a recent study by the Tax and Transfer Policy Institute reveals, much of the tax benefit of super flows to higher income and older, wealthier Australians…

The largest tax advantage for higher income earners building wealth is achieved through concessional super contributions, as the below chart depicts…

It should, by now, be abundantly clear to policymakers that this current level of taxpayer largesse is simply unsustainable.

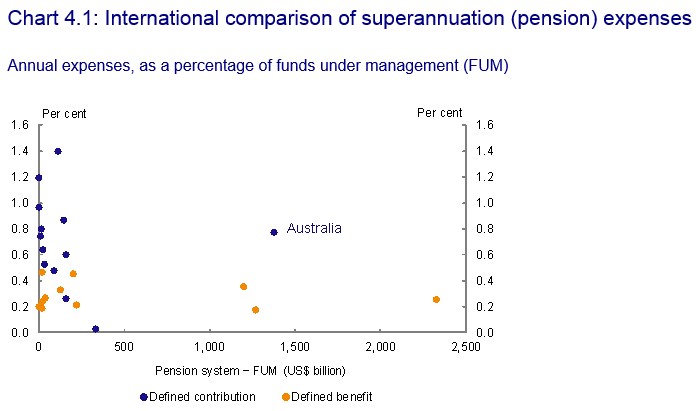

I will add that despite the superannuation industry’s gargantuan size ($2.7 trillion), Australia’s average management fees are well above the OECD average, as illustrated by the Murray Financial System Inquiry:

Advertisement

Thus, what has been created is a giant inefficient suck hole.

From the outset MB has argued against lifting the superannuation guarantee (SG) to 12% for the following primary reasons:

Advertisement

It would lower workers’ take-home pay, hitting lower-income earners especially hard.

It would increase inequality, given the lion’s share of concessions flow to high income earners.

It would worsen the long-term sustainability of the Budget, since the cost of superannuation concessions outweighs the benefits from lower pension outlays.

In reality, Australia’s superannuation system works more as a tax avoidance scheme for the rich than a genuine retirement pillar.

The only real beneficiaries from lifting the SG to 12% are superannuation funds, which would get to earn fatter management fees at the expense of both Australian workers and taxpayers.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.