Tell him he’s dreaming: Perrottet’s stamp duty reform fails cost-benefit

By Jesse Hermans, Policy Director at Prosper Australia, an NGO focussed on tax reform.

The Thodey Review’s draft report is right to place land tax at the centre of its vision for state tax reform.

Replacing stamp duty with what the Review called “the states’ best tax lever” has the potential, if enacted sensibly, to support budget recovery without impeding economic growth.

But how this switch is implemented is important.

We commend the NSW Treasurer for taking on the formidable political challenge of tax reform. However, the apparently pain-free transitional approach floated will lose too much revenue and

offer little efficiency advantage over the status quo. Furthermore, it will take 50 years to realise its potential.

The Treasurer suggests letting new buyers ‘opt in’ to land tax, and exempting all current owners by ‘grandfathering’ the changes.

The optional tax, of course, implies a tax cut. Investors, developers and speculators holding property for short periods will opt in to land tax to reduce their overall tax bill. Buyers expecting longer tenure

will opt out and pay no more tax than at present. There will be a net loss of revenue – the principle of adverse selection at work.

Our modelling suggests that for every $1 lost from buyers opting out of land tax, an average $0.67 will be recovered in stamp duty. We estimate that roughly half of buyers will opt out, so this policy will cost one tax dollar in six – more than $1 billion per annum in NSW.

Higher land tax rates cannot recoup this loss without driving more buyers out. And the opt in model leaves the central problems with stamp duty unresolved. High-turnover transactions – evidently little

discouraged at present – get tax cuts, while the inequity and inefficiency of stamp duty in relation to long-held properties remains unaddressed.

The proposal to grandfather tax-free status for existing owners feels intuitively fairer, since it preserves the tax bargain understood upon purchase. Why should those who have ‘pre-paid’ stamp duty also now ‘pay as you go’ with land tax, just like new buyers not subject to duty?

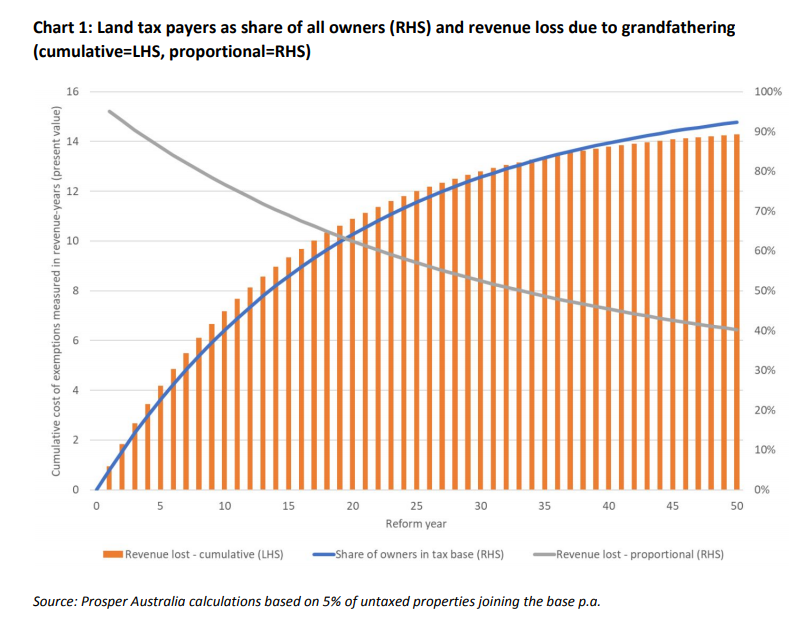

The problem here is that full grandfathering entails a massive and unavoidable loss of tax revenue over a transition period lasting generations. To maintain state spending will therefore require a

permanent increase in state debt.

Stamp duty is paid upfront by buyers, but states have always spent it like a PAYG revenue source. None has been put aside to pay for exemptions as we switch to a recurrent tax; there is no ‘sinking

fund’ to run down. The tax switch might be neutral from the perspective of the average buyer, but from the perspective of the public balance sheet it is not.

Tax revenue securitisation can provide cashflow but not alter the debt impact. Fancy debt is still debt.

In 20 years, with a typical 5% per annum turnover, full grandfathering in NSW will see only two-thirds of properties paying land tax – and perhaps only half that if buyers are allowed to opt out.

This exemption will cost NSW $75 billion (more than 60% of potential land tax revenue) over that period. By contrast, the ACT is transitioning to stamp duty over 20 years, without losing revenue.

A better approach is the Prosper model, which would limit exemptions to the most recent buyers and could be enacted by means such as a partial refund of stamp duty, paid for via a sunsetting

temporary rate.

Perrottet’s no-losers model to tax reform ought to raise eyebrows, as both ‘opt-in’ and ‘grandfathering’ run counter to the aims of the reform. The Review’s final report must call out this wishful thinking, and propose transition options consistent with economic reality.

By the time the entire transition is complete, NSW will have blown 20% of GSP on concessions to landowners who, according to the Thodey Review, have already benefited from “a once-in-a-generation land price windfall”. The equity this buys – a preservation of existing tax privileges above all else – is one we simply cannot afford.

The full Prosper report can be downloaded here.