As we know, Australian households are among the world’s most indebted people.

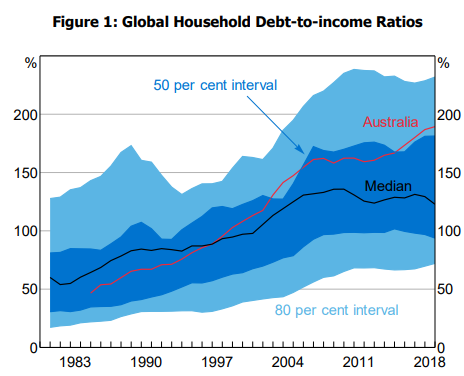

According to the Bank for International settlements, Australians held the second highest household debt loads as a share of GDP at the end of 2019 (120%), behind only Switzerland (132%).

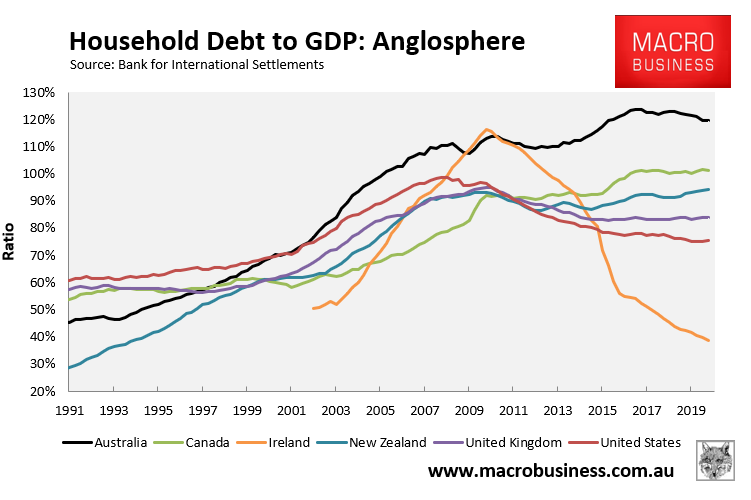

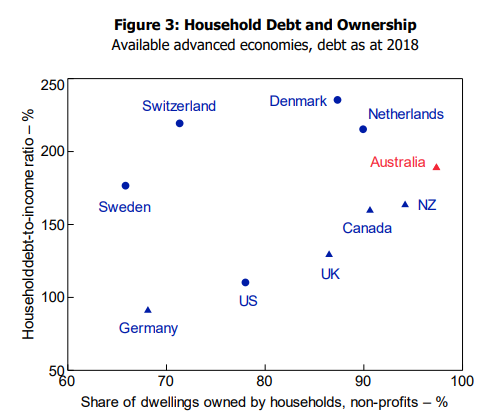

Australia’s household debt loads also dwarf other advanced English-speaking nations, as clearly illustrated in the next chart:

Advertisement

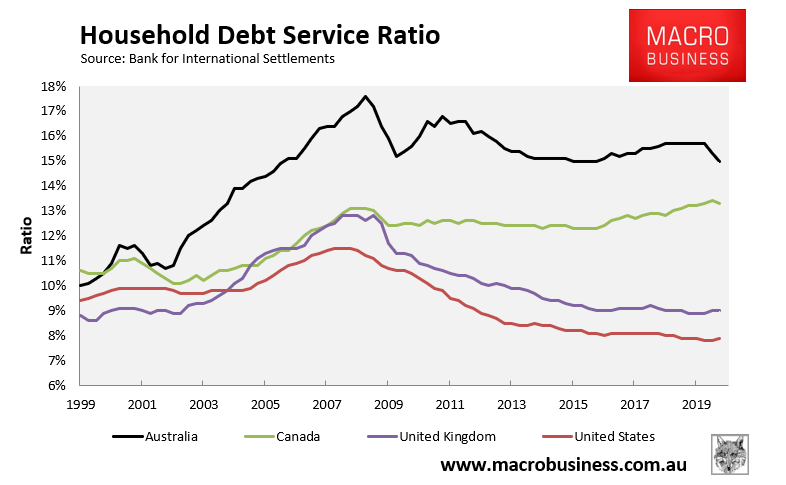

Australian households also have the second highest debt repayment burdens in the world, again dwarfing other advanced English-speaking nations:

Australia’s risky debt metrics raise obvious concerns that households, the banking sector, and the broader economy are at risk of sudden debt-deflation.

Advertisement

No, says the RBA, which has released a new paper claiming that Australia’s high household debt load does not pose major risks to the economy:

It is often observed that the level of household debt (relative to income) is high in Australia compared with other countries and its own history. Many commentators argue that it creates a major vulnerability for the country’s economy.

Concerns about how this will influence the economy’s ability to navigate a major downturn have for many years been central to understanding the resilience of the Australian economy.

In this paper we investigate how important these concerns are. We ask three questions:

1. Why is household debt in Australia relatively high compared with other countries, and what are the main reasons it has increased over time?

2. How big are the risks this debt poses to the banking system?

3. How might this debt shape the response of consumer spending to severe downturns in the economy?

We answer the first question using a panel of data for a wide range of countries over a long period of time.

We apply regression techniques to identify what factors are associated with different levels of debt in these countries at each point in time. The coefficients from this can then be applied to the Australian data to assess why Australian households have their current level of debt.

Our results imply that the rise in household indebtedness has been primarily driven by strong growth in household income and by the fall in real interest rates and inflation. Together these factors have increased the share of income households can spend on housing and the amount of debt that share of income can service.

The easing of restrictions on the financial sector in the late 1980s and early 1990s also appears to have contributed, and our model cannot explain the increase in debt over the past four or five years.

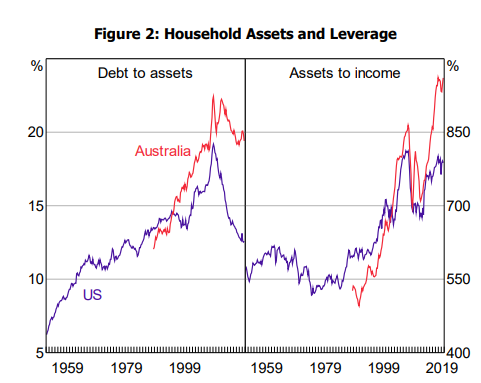

High levels of household income also enable Australians to sustainably hold more debt than in many other countries. The main reason, however, why Australian household debt is relatively high is that the housing rental stock, and hence the debt used to fund it, is owned by the household sector. In most other countries, a significant share of rental properties, and the associated debt, belongs to the government or corporate sectors.

We address the second and third questions with a stress testing framework, using detailed household-level data. We start by simulating how households’ financial positions would change if the economy faced a severe but plausible recession, in which the unemployment rate rose significantly and housing and other asset prices fell sharply (using data prior to the COVID-19 pandemic). We then measure the potential risks to banks by determining how much debt is held by households that would be unable to repay it in this scenario.

Our assessment of how this debt might affect the response of consumer spending involves applying coefficients from the global literature on how consumers react to falls in wealth. We use both the literature that estimates a single coefficient (on average, across all households) and work that explores how increased levels of indebtedness can amplify individual households’ responses.

These stress tests show that banks are well placed to handle a severe downturn in the economy. The main reason for this is that they have maintained strong lending standards: most of the debt is held by households that have significant equity backing their loans and that are less likely to become unemployed than others in a downturn.

Nonetheless, we show that these households could still significantly curtail their consumption in response to a severe recession, especially if they react more strongly to declines in housing prices than

they do to rises.

We find some evidence that the potential fall in consumption has become modestly larger since the early 2000s, as household indebtedness has risen. However, the distribution of debt across households does not appear to have a material influence on the sensitivity of household spending to debt.

Our work leads us to three implications.

First, we argue that it can be misleading to say that households in Australia are more vulnerable than those in other countries to economic shocks because they have higher levels of household debt. Rather, this higher indebtedness is mostly due to measurement issues and a greater capacity to service higher levels of debt.

Second, the distribution of debt across households matters a lot for how likely it is to pose material problems to banks, but does not materially affect the risks this debt poses to consumer spending.

And third, any issues that arise from high levels of household indebtedness in Australia are more likely to manifest in a larger-than-otherwise fall in consumer spending than they are to result in bank failures. This reflects that Australian banks (guided by the Australian Prudential Regulation Authority) have mostly done a good job in allocating credit to those that can afford it, and that households have used some (admittedly small) portion of their wealth accumulated over recent years to support spending.

This is obviously the Panglossian view on Australia’s household debt. The alternative view is provided by Martin North, whose mortgage debt surveys paint a far less rosy picture.

Advertisement

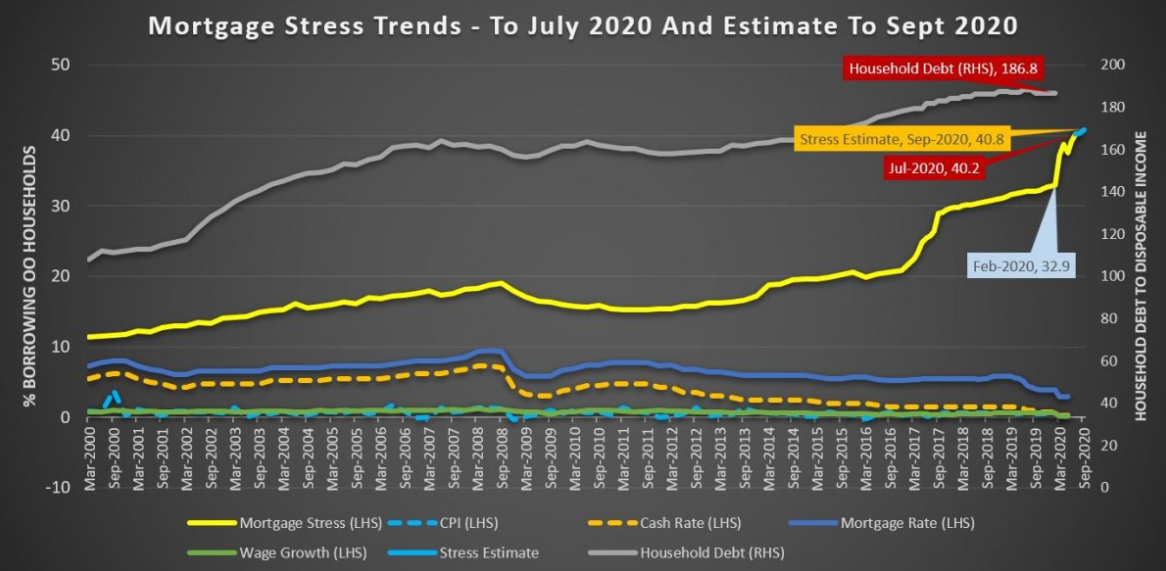

North defines stress in cash flow terms – money in and money out – with those in negative cash flow flagged as stressed.

His latest survey shows that mortgage stress is running at record high levels, with more than 1.5 million households experiencing mortgage stress:

Advertisement

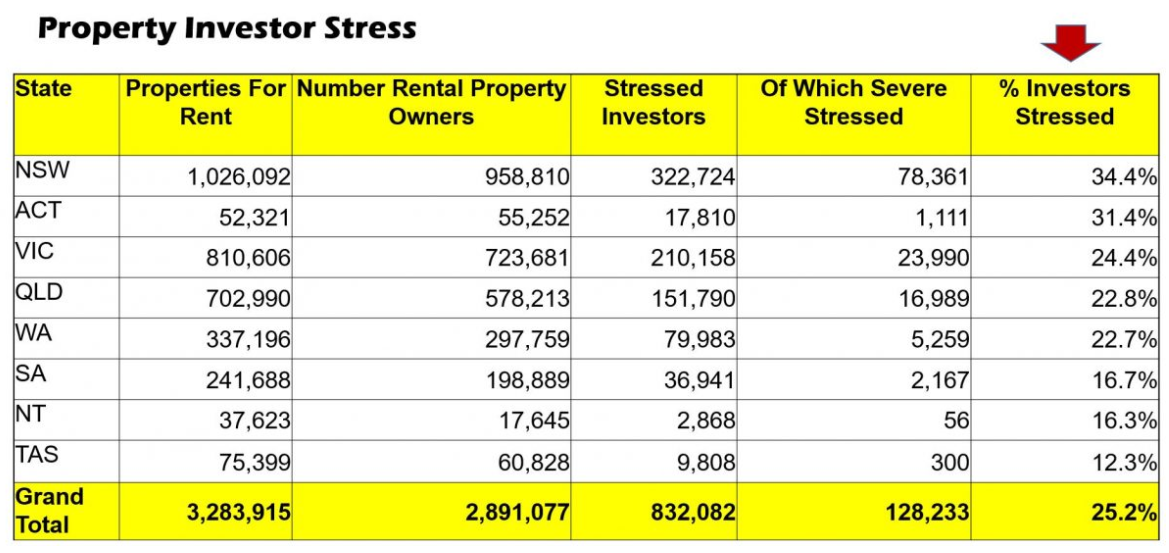

Moreover, around one-quarter of property investors are stressed – i.e. losing money:

This is obviously a major concern given around 500,000 Australian households have deferred repayments on mortgages worth around $195 billion, as well as the pending unwinding of emergency income support, namely:

Advertisement

JobKeeper reduced from $1500 to $1200 from October ($750 part-time); and

JobSeeker reduced from $1100 to $815 from October.

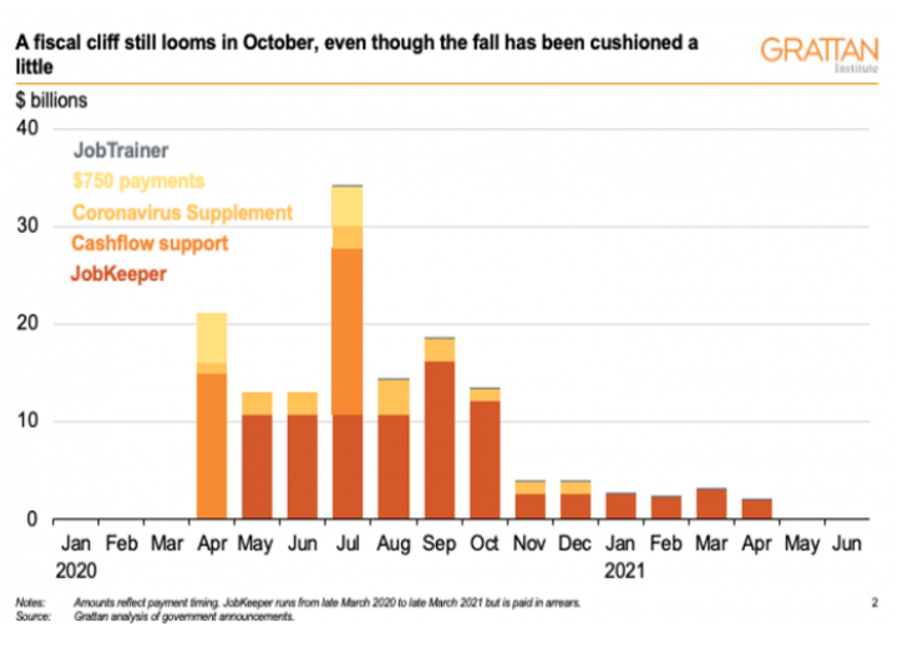

The Grattan institute estimates this tapering will reduce income support from $18 billion a month (10.7% of monthly GDP) to $3 billion a month (1.9% of GDP) for the six months beyond:

Advertisement

The key risk is that a significant proportion of stressed mortgage holders will be forced to sell, leading to a feedback loop that drives property prices lower.

This risk is obviously highest for the 25% of stressed property investors that are now caught in a pincer of falling prices and rents.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.