Paul Keating continues to scaremonger against freezing the superannuation guarantee (SG) at 9.5%, claiming it would leave Australians destitute in retirement:

“You cannot have a decent income in retirement without self provision. Otherwise, you would have people on the pension which is now what $23,000 or $540 a week?,’’ he said…

Mr Keating said if workers failed to save enough super now more will be forced to survive off the aged pension.

“Well. The thing is there’s no economic case for it not to go ahead. None. There’s a prejudicial case from some of these baby-faced Liberals,’’ he said.

“These first term senators, a particular modest form of political life.”

As usual, Paul Keating has failed to mention that superannuation concessions cost the federal budget more than they save in aged pension costs.

The Henry Tax Review was abundantly clear on this point:

“An increase in the superannuation guarantee would … have a net cost to government revenue even over the long term (that is, the loss of income tax revenue would not be replaced fully by an increase in superannuation tax collections or a reduction in Age Pension costs).”

The Grattan Institute has also shown that over “both the short and long term, superannuation tax breaks cost the budget more than they save in pension payments”:

As has actuarial firm Rice Warner:

Actuarial firm Rice Warner said that lifting compulsory super contributions to 12% would not have much impact on the age pension for many years, and would save the budget only about 0.1% in lower age pension spending in the second half of this century.

In contrast, extra super tax breaks from higher compulsory super would cost an average of 0.22% of GDP “through this century”…

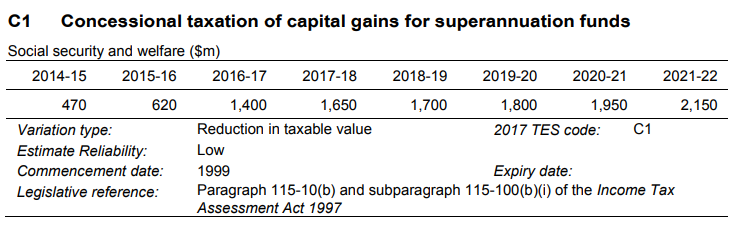

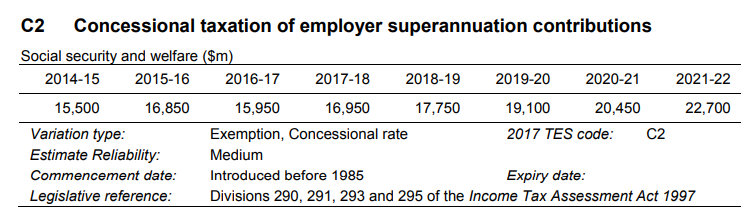

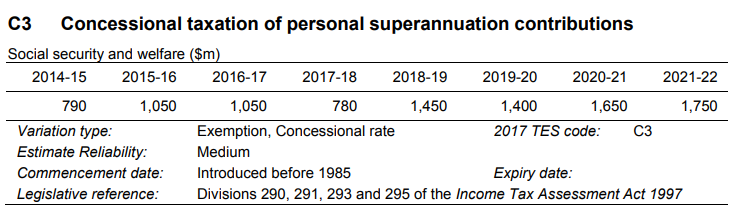

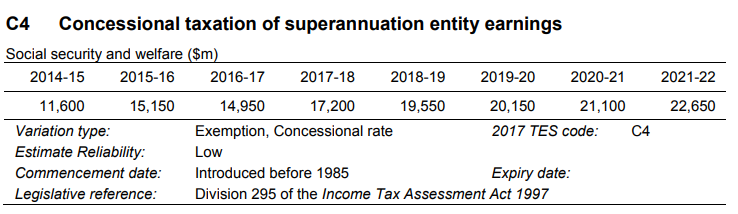

Superannuation concessions were projected to cost the federal budget $45 billion a year this financial year and a whopping $49.3 billion next financial year:

This extraordinary cost necessarily means there are less funds available in the federal budget to lift the aged pension.

In turn, lifting the SG to 12%, as advocated by Paul Keating, would rob the federal budget of more money, making it even harder to raise the pension.

If Paul Keating genuinely cared about the welfare of future retirees he would argue to unwind the compulsory superannuation system altogether and shift the enormous budget savings into lifting the aged pension rate and expanding its eligibility.

Because ultimately, it is the enormous cost of superannuation concessions that prevents the aged pension from being lifted to an adequate level.