Major fiscal impact from COVID-19 to extend over the next decade and beyond

The future economic and fiscal impact of the COVID-19 pandemic remains highly uncertain and recent forecasts have had particularly short shelf lives due to the rapidly changing nature of the situation. It is clear, however, that the impact will be major and extend over the medium-term. To support an understanding of the likely magnitude of the budget impact based on the latest information, this update of the medium-term fiscal projection scenarios1 incorporates the Reserve Bank of Australia’s (RBA) August economic forecasts2 and policy decisions included in the Commonwealth Government’s July 2020 Economic and Fiscal Update (EFU).

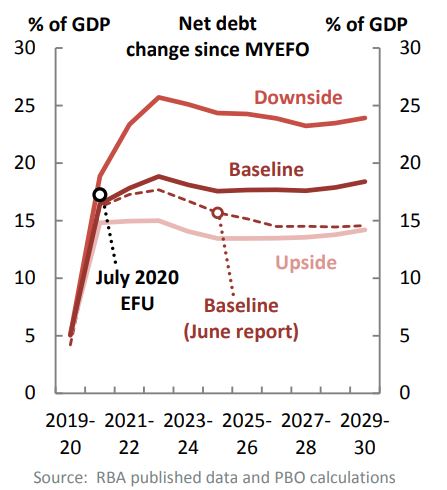

Three fiscal scenarios are presented based on the economic scenarios published by the RBA in the near-term and standard budget assumptions thereafter: a baseline of a gradual economic recovery; an upside scenario of a faster recovery (resulting in less additional debt); and a downside scenario of a slower recovery (resulting in more additional debt). The results are shown as a deviation from December’s Mid-Year Economic and Fiscal Outlook (MYEFO), which was the last full Budget update. While not equivalent to budget forecasts, these scenarios represent a reasonable range for the impact of COVID-19 over the next decade.

The analysis shows that the impact of COVID-19 may result in Commonwealth Government net debt in 2029–30 being between 14 and 24 per cent of GDP (up to $800 billion) higher than it would have been otherwise, as shown in the chart.

The pandemic results in higher net debt due to lower receipts from slower economic growth and the significant policy response in 2019–20 and 2020–21. The resultant impact of increased borrowing endures through to 2029–30.

The ‘baseline’ result is around 4 per cent of GDP higher by 2029–30 than presented in our June fiscal scenarios report (also shown on the chart). This is largely because our June report did not include the impact of lower migration on Australia’s future population. Our updated scenarios incorporate the estimated permanent impact on population from lower migration due to border closures in 2019–20 and 2020–21, as published in the EFU.

Presumably, that is a flow chart not stock. So, in the worst-case scenario offered by the RBA (which is the PBO’s first mistake), Aussie public debt will be in the order of 50% of GDP by 2030.

That would leave it at roughly half the levels of all other developed economies. The additional interest bill per annum at current interest rates will be $7.2bn per annum. A virtual rouding error in tax remittance and cost terms. Double it if you like.

Advertisement

And all of that before we even begin to talk about QE or MMT in which we pay the bill to the RBA and it comes back as a dividend anyway.

There is no affordability issue here at all.

That said, we will not always be so lucky with commodity prices, and the worst case is much worse than the RBA is willing to contemplate, so there’s no need to be wasteful when the right time comes to cut back.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.